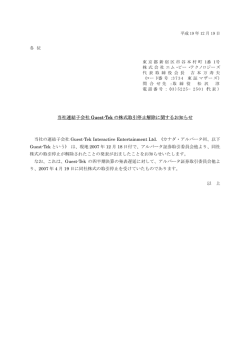

Empirical Testing of Parsimonious Equity Valuation Models1 Carl Fredrik Danielson2, Martin Grund3 and John Gyllenhammar4 18 December 2007 Master’s Thesis in Finance/Accounting and Financial Management Stockholm School of Economics Tutor: Professor Kenth Skogsvik Abstract This paper empirically evaluates the ability among different parsimonious equity valuation models to withstand factors causing valuation errors and to estimate the fair market value. The asset-based book value of owners’ equity and the discounted cash flow based capitalised earnings model are empirically evaluated along with the terminal value constrained versions of Residual Income Valuation and Abnormal Earnings Growth valuation models. Extended and altered versions of these models are also evaluated. The empirical testing is performed by estimating and comparing the valuation errors for a sample of publicly traded Swedish companies over the time period 1998-2007. The constrained versions of Residual Income Valuation and Abnormal Earnings Growth valuation models generally provide smaller absolute valuation errors than the book value and capitalised earnings respectively. Adjusting the Residual Income Valuation model for the valuation bias at the horizon point of time is found to be a feasible extension of the model under the provision that an accurate estimation of the valuation bias is available. Evaluating the Abnormal Earnings Growth valuation model against the Residual Income Valuation model shows that the abnormal earnings-based approach generally seems to capture valuation biases to a larger extent and on average provides a smaller average absolute valuation error. 1 The authors gratefully acknowledge Professor Kenth Skogsvik for helpful comments and guidance. [email protected] 3 [email protected] 4 [email protected] 2 1 Table of Contents 1. Introduction and Purpose .......................................................................................................................4 2. Summary ....................................................................................................................................................6 3. Valuation Models and Hypotheses ........................................................................................................8 3.1. Assumptions and Notations.............................................................................................................8 3.2. Introduction to Models...................................................................................................................10 3.3. Book Value of Owners’ Equity .....................................................................................................10 3.4. The Residual Income Valuation Model and Its Terminal Value Constrained Version........11 3.5. The Terminal Value Constrained Residual Income Valuation Model Extended with Permanent Measurement Bias Adjustment.........................................................................................12 3.6. The Capitalised Earnings Model in Two Versions.....................................................................13 3.7. The Abnormal Earnings Growth Valuation Model and Its Terminal Value Constrained Version......................................................................................................................................................14 3.8. Hypotheses........................................................................................................................................15 4. Data...........................................................................................................................................................19 4.1. Data Set, Descriptive Statistics and Consistency Checks ..........................................................19 5. Empirical Analysis ..................................................................................................................................22 5.1. Modelling Assumptions ..................................................................................................................22 5.2. Book Value of Owners’ Equity .....................................................................................................26 5.3. The Terminal Value Constrained Residual Income Valuation Model ....................................27 5.4. The Permanent Measurement Bias Extended Version of RIV(TVC).....................................28 5.5. The Capitalised Earnings Model (Required Rate of Return on Equity) .................................32 5.6. The Capitalised Earnings Model (The Risk-free Interest Rate) ...............................................33 5.7. The Terminal Value Constrained Abnormal Earnings Growth Valuation Model................35 5.8. Testing of Hypothesis 1..................................................................................................................37 5.9. Testing of Hypothesis 2 and Sub-Hypothesis.............................................................................38 5.10. Testing of Hypothesis 3................................................................................................................41 5.11. Testing of Hypothesis 4................................................................................................................42 5.12. Testing of Hypothesis 5................................................................................................................44 5.13. Summary of Empirical Results and Statistical Testing ............................................................46 6. Discussion of Empirical Results and Concluding Comments ........................................................50 6.1. Discussion of Empirical Results....................................................................................................50 6.2. The Validity and Robustness of the Empirical Results .............................................................56 7. References................................................................................................................................................59 8. Appendix..................................................................................................................................................60 8.1. Appendix 1: Derivation of AEG(TVC) from PVED................................................................60 2 8.2. Appendix 2: GICS Industry Sectors and GICS Level 1 Sector Group Indexes....................61 8.3. Appendix 3: Data Sample...............................................................................................................62 8.4. Appendix 4: Valuation error in RIV(TVC)..................................................................................65 8.5. Appendix 5: Valuation error in RIV(PMB) .................................................................................66 8.6. Appendix 6: Valuation error in AEG(TVC)................................................................................67 8.7. Appendix 7: Comparison Between the Valuation Error in AEG(TVC) and RIV(TVC) ....68 8.8. Appendix 8: Beta Calculations.......................................................................................................69 8.9. Appendix 9: Average Absolute Valuation errors per Sector and Year......................................70 8.10. Appendix 10: Empirical Results 1998-2002 ..............................................................................72 8.11. Appendix 11: Empirical Results 2003-2007 ..............................................................................75 8.12. Appendix 12: Empirical Results Five or More Consensus Estimates (1998-2007) ............78 8.13. Appendix 13: Empirical Results 5% Equity Risk Premium (1998-2007) .............................81 8.14. Appendix 14: Statistical Testing 1998-2002...............................................................................84 8.15. Appendix 15: Statistical Testing 2003-2007...............................................................................86 8.16. Appendix 16: Statistical Testing Five or More Consensus Estimates (1998-2007).............88 8.17. Appendix 17: Statistical Testing 5% Equity Risk Premium (1998-2007) .............................90 8.18. Appendix 18: Summary of Empirical Results and Statistical Testing: 1998-2002...............92 8.19. Appendix 19: Summary of Empirical Results and Statistical Testing: 2003-2007...............96 8.20. Appendix 20: Summary of Empirical Results and Statistical Testing: 5 or More Consensus Estimates (1998-2007) ......................................................................................................................... 100 8.21. Appendix 21: Summary of Empirical Results and Statistical Testing: 5% Equity Risk Premium (1998-2007) .......................................................................................................................... 104 3 1. Introduction and Purpose In the practice of equity valuation, straightforward valuation models with few assumptions and an ability to withstand factors that have strong impact on the valuation are attractive. A review of the most frequently applied equity valuation models would show that the Discounted Cash Flow (DCF) valuation models are commonly used. In DCF modelling, explicit forecasts of the company’s future performance and growth are used to calculate the present value of future cash flows. A DCF model relies on strong assumptions and the mechanical valuation technique is sensitive for alterations in these assumptions. More straightforward valuation models less dependent on crucial assumptions and with an ability to withstand factors that have strong impact on the valuation are therefore desirable. The Residual Income Valuation (RIV) model has made a great impact on accounting-based valuation practice. RIV modelling anchors residual earnings to book value of owners’ equity as a possible measure of a firm’s value creation. Current value of owners’ equity is defined as the sum of book value of owners’ equity and the present value of future residual earnings. Similar to the RIV model, but anchoring value to the capitalised earnings, the Abnormal Earnings Growth (AEG) model has recently been introduced by Ohlson and Juettner-Nauroth (2005). AEG focuses on future earnings and earnings growth, and the AEG model defines current value of owners’ equity as the sum of capitalised earnings and the present value of future abnormal earnings growth. Parsimonious versions of both the RIV and AEG models, where the terminal value is set to zero at some horizon point of time, are considered as practical benchmark models for equity valuation based on financial statement information and forecasts of the future. The terminal value constrained versions of RIV (RIV(TVC)) and AEG (AEG(TVC)) modelling are, however, more or less affected by conservative accounting and the company’s distance to steady state at the valuation point of time. Under the assumption of steady state, the valuation bias from conservative accounting of the RIV(TVC) model is proposed by Skogsvik and Juettner-Nauroth (2007) to be non-positive and dependent on the conservative bias of owners’ equity at the terminal point of time, whereas the valuation bias of the AEG(TVC) model depends on the capitalised growth of the conservative bias in the terminal period. If the growth of the conservative bias coincides with the general growth in a company that has entered the steady state, the measurement error in the terminal value constrained AEG model is typically smaller than in the corresponding RIV model. (Skogsvik and Juettner-Nauroth, 2007) The purpose of this paper is to empirically evaluate the ability among different types of parsimonious equity valuation models to withstand factors causing valuation error. The reasoning will be based on the theoretical framework presented in the working paper by Skogsvik and 4 Juettner-Nauroth (2007). The valuation error in the empirical analysis is, however, not solely attributable to conservative accounting; other factors, e.g. the distance to steady state, will also provide a valuation bias. The evaluation will cover the asset-based book value of equity (Bv), the discounted cash flow based capitalised earnings (PVEE) along with the accounting-based parsimonious valuation models RIV(TVC) and AEG(TVC). Extended versions of the RIV(TVC) model will also be evaluated. The evaluation will be performed by estimating and comparing the valuation errors to make inferences about the models’ ability to reflect the fair value of owners’ equity. This paper is organized as follows. In section 2 the main results of this paper are summarised. In section 3, assumptions and valuation models are specified together with the hypotheses that will underpin the empirical testing and discussion. In section 4, the data is discussed together with descriptive statistics and consistency checks. Section 5 presents the empirical analysis of the models’ measurement error and testing of hypotheses. Section 6 discusses the results and its validity, and finally summarises the results with concluding comments. The Appendixes provide detailed and explaining tables, charts and information. 5 2. Summary The major results of this paper are: Result 1: The RIV(TVC) model [on average] provides a smaller absolute valuation error than book value of owners’ equity for 9 out of 9 industry sectors. Result 2: The RIV(PMB) model [on average] provides a smaller absolute valuation error than RIV(TVC) for 5 out of 9 industry sectors. RIV(TVC) [on average] provides a smaller absolute valuation error than RIV(PMB) for 2 out of 9 industry sectors. Result 3: The PVEE(rf) model [on average] provides a smaller absolute valuation error than PVEE(rE) for 1 out of 9 industry sectors. PVEE(rE) [on average] provides a smaller absolute valuation error than PVEE(rf) for 8 out of 9 industry sectors. Result 4: The AEG(TVC) model [on average] provides a smaller absolute valuation error than PVEE(rE) for 5 out of 9 industry sectors. PVEE(rE) [on average] provides a smaller absolute valuation error than AEG(TVC) for 3 out of 9 industry sectors. Result 5: The AEG(TVC) model [on average] provides a smaller absolute valuation error than RIV(TVC) for 7 out of 9 industry sectors. RIV(TVC) [on average] provides a smaller absolute valuation error than AEG(TVC) for 2 out of 9 industry sectors. The main results imply that the models show varying levels of abilities to capture biases in the valuation of equity. RIV(TVC) and AEG(TVC) generally provide smaller absolute valuation errors than the book value and PVEE respectively. Adjusting the RIV(TVC) valuation for the conservative bias at the horizon point of time is found to be a feasible extension of the model provided that an accurate estimation of the permanent measurement bias is available. Estimating Q to adjust for conservative bias as well as the firm-specific goodwill/badwill at T<T* does not provide a smaller valuation error than the PMB extension. Evaluating the AEG(TVC) model against RIV(TVC) shows that the abnormal earnings-based approach generally seems to provide a smaller average absolute valuation error. 6 In general, the empirical results and statistical testing can be seen as robust over time and for critical modelling assumptions. These are attractive features that would separate the parsimonious valuation models from more complex valuation models. The volatile and relatively large average valuation errors in the empirical evaluation, however, shed light on the difficulties in finding appropriate rules of thumb to apply on industry sectors and over a long period of time. 7 3. Valuation Models and Hypotheses 3.1. Assumptions and Notations The notations used in this paper (in alphabetical order): Bvt = Book value of owners’ equity at time t, after capital transactions between the company and the owners at time t. Cbt = Conservative valuation bias in owners’ equity at time t. Divt = Expected dividend paid to the shareholders less any new issue of equity capital at time t. Et(…) = Expectation operator, conditioned on available information at time t. g = kt = Company growth rate in earnings. Net payout ratio as a percentage of earnings, i.e. the net of dividends and new issue of equity capital divided by earnings. Nt = New issue of equity capital at time t. Pt = Market value of owners’ equity at time t after capital transactions (dividend and/or new issue of equity capital) between the company and the owners at time t. q= The relation between the market value and the book value of owners’ equity. rE = Required rate of return on owners’ equity, i.e. the cost of equity capital. RE = (1+ rE). rm –rf = The market risk premium, i.e. the incremental return that investors require from holding risky equities rather than risk-free securities. rf = The risk-free interest rate, i.e. the interest rate at which an investor could invest with no default risk. T* = The firm specific point in time where only zero net present value (NPV) project are executed, i.e. steady state. …(UB) = Unbiased accounting. Vt = Value of owners’ equity according to the applied valuation model at time t, after transactions between the company and the owners at time t. Xt = Accounting net earnings accumulated over the period. 8 The following assumptions are assumed to hold: 1. The valuation point of time coincide with t=0 (t0) throughout the whole paper. 2. Dividends and new issues of equity capital are marked to market and settled at the end of future periods. 3. The investment risk associated with the (net) dividends payments is incorporated in the required rate of return on owners’ equity. 4. The required rate of return on owners’ equity is non-stochastic and has a flat term structure. 5. The deviations from the clean surplus relation (CSR) in future financial statements are expected to be zero, i.e. net income, dividends, and new issues of equity capital account for all changes in the book value of owners’ equity: E 0 [Bv t +1 − ( Bv t + X t +1 − Div t +1 )] = 0 ⇔ E 0 ( Bv t +1 ) = E 0 ( Bv t ) + E 0 ( X t +1 ) − E 0 ( DIVt +1 ) 6. (CSR) This relationship of conservative accounting (Cbt) could be denoted: Bv (0UB ) − Bv 0 = Cb 0 ≥ 0 E 0 ( Bv (t UB ) ) − Bv t = E 0 ( Cb t ) ≥ 0 (Cbt) E 0 ( X t ) = E 0 [ X (t UB ) − ( Cb t − Cb t −1 )] = E 0 ( X (t UB ) ) − E 0 [ ∆( Cb t )] (Skogsvik and Juettner-Nauroth, 2007) The reasoning above implies that when steady state is reached, the book value of owners’ equity equals market value if accounting is unbiased. Conservative accounting implies that the book value will be lower than the market value when steady state is not yet reached. However, it should be noted that the impact on earnings is ambiguous. 9 3.2. Introduction to Models The evaluated models [with some reservation for book value of owners’ equity] can be derived from the present value of expected dividend (PVED) valuation. In PVED, the value of owners’ equity equals the present value of all future dividends paid by the firm to its equity holders: ∞ V0 = ∑ E 0 ( Div t ) R ET t =1 (PVED) By inserting a horizon point in time t=T, an unconstrained version of the PVED can be obtained: V0 = ∑ T E 0 ( Div t ) E 0 ( PT ) + R tE R ET t =1 (PVED) PVED requires explicit forecasts of dividends for T periods and a forecast of the terminal price PT at the end of period T. 3.3. Book Value of Owners’ Equity Book value is determined by the current book value of equity on the balance sheet and represents the shareholders’ investments in the firm: V0 = Bv 0 (Bv) The book value of owners’ equity does not, however, capture the future expected earnings associated with the shareholders’ investments and thus the measure does not fully reflect the intrinsic value of owners’ equity. In a company with future earnings, the intrinsic value of equity must therefore equal the sum of book value of owner’s equity and a premium. This fits with the idea that investors pay for future earnings today5. (Penman, 2007) 5 The relationship between the market valuation of owners’ equity and book value of owners’ equity is often referred to as the Market-to-Book ratio. 10 3.4. The Residual Income Valuation Model and Its Terminal Value Constrained Version The RIV model clarifies the linkage between accounting-based measures of owners’ equity, earnings and the intrinsic value of owners’ equity (Ohlson, 2005). With book value of owners’ equity as an anchor, the RIV model uses residual earnings as a measure of a firm’s value creation. The intrinsic value of owners’ equity is defined in RIV modelling as the sum of book value of equity and the present value of future residual income. Under the assumption that CSR holds, E0(Divt) can be rewritten in accounting terms and incorporated in the PVED to develop the RIV model: V0 = ∑ T E 0 ( Div t ) E 0 ( PT ) + R tE R ET t =1 (PVED) E 0 ( Bv t +1 ) = E 0 ( Bv 0 ) + E 0 ( X t +1 ) − E 0 ( Div t +1 ) T V0RIV = Bv 0 + ∑ t =1 E 0 ( X t − rE ⋅ Bv t −1 ) E 0 ( PT − Bv T ) + R tE R ET (RIV) The formula above shows that the value of owners’ equity is driven by three factors: 1. Opening book value of owners’ equity, excluding dividend and including any new issue of share capital: Bv 0 2. Present value of the expected residual income until the horizon point in time. The residual income is calculated as the difference between earnings and the return on equity: T ∑ t =1 3. E 0 ( X t − rE ⋅ Bv t −1 ) R tE The present value of the goodwill/badwill of owners’ equity at the horizon point in time, which can be explained by the present value of all future residual incomes: E 0 ( PT − Bv T ) R TE 11 The unconstrained RIV valuation model is conditioned on the assumption of CSR, which implies that the function is unaffected by the choice of accounting principles. Provided that the accounting is done in compliance with CSR, the model will yield the same result as PVED. If the accounts are prepared with conservative accounting principles, higher excess profits will be created and a constantly higher residual income will be produced at the horizon point of time. Given unbiased accounting and if T≥T* (i.e. the company is in steady state and there is no business goodwill/badwill at the horizon point of time) the terminal value in the unconstrained version of RIV drops out and could be set to zero in a parsimonious terminal value constrained version of the model: T ( TVC ) V0RIV = Bv 0 + ∑ ,CB t =1 E 0 ( X t − r ⋅ Bv t −1 ) R tE (RIV(TVC)) If accounting is conservatively biased and/or if T<T*, the RIV(TVC) model is affected by the valuation bias of the terminal value, and will consequently provide a valuation error in the valuation of owners’ equity. (Skogsvik and Juettner-Nauroth, 2007) 3.5. The Terminal Value Constrained Residual Income Valuation Model Extended with Permanent Measurement Bias Adjustment If accounting is biased and/or if T* is not reached at the terminal point of time (T), RIV(TVC) will provide a valuation error. An adjustment aimed to decrease this error could be made by extending the parsimonious terminal value constrained version of RIV with an estimation of the business goodwill/badwill at T: T V0RIV ( PMB ) = Bv 0 + ∑ t =1 E 0 ( X t − rE ⋅ Bv t −1 ) q ⋅ Bv T + R tE R ET (RIV(PMB)) where: q ⋅ Bv T E 0 ( PT − Bv T ) = R TE R TE An estimate for the q-measure that defines the valuation bias as a fraction of book value at t=T could be obtained from financial literature for a swift extension of the RIV(TVC) model. 12 The estimation of q if T=T* (i.e. the estimation of conservative accounting) is often referred to as the permanent measurement bias (PMB)6. (Runsten, 1998) 3.6. The Capitalised Earnings Model in Two Versions The discounted cash flow approach and earnings-based capitalised earnings model (PVEE) can be derived from PVED using, the dividend payout ratio (k): V0 = k 1 X 1 (1 + g ) k 1 X 1 = rE − g rE − g (PVEE) Assuming that all earnings are paid out as dividends (kt=1), a firm will not make any investments and hence the growth could be assumed to equal zero (g=0): V0 = X1 rE (PVEE(rE)) As an attractive model feature, PVEE does not depend on any choice of particular parameters relating to dividend policies. Rather, it focuses on the more easily forecasted next year earnings. The major drawback of PVEE, however, is the focus on next year earnings solely to value owners’ equity. This approach could potentially lead to valuation errors if next year earnings are not representative for future earnings and earnings growth, e.g. as a result of conservative bias. PVEE(rE) by its definition does not capture the value of growth in future earnings, and thus the model could be expected to underestimate the value of owners’ equity for companies with growth in earnings. By removing the risk adjustment from the cost of equity capital in the denominator and under the assumption that the growth and risk parameters are of equal size (or that the growth factor is greater than the risk parameter), capitalising the earnings with the riskfree interest rate would potentially imply a more accurate estimation of owners’ equity7: V0 = 6 X1 rf (PVEE(rf)) The observant reader notes that the estimated PMB value must not necessarily equal q, and thus, the extension of the model will not always neutralise the valuation bias. The implications of this will be discussed in connection with the evaluation of RIV(PMB). 7 This valuation approach is often used on aggregate market capitalisation over the world and is popularly referred to as the Fed Model. 13 3.7. The Abnormal Earnings Growth Valuation Model and Its Terminal Value Constrained Version With PVEE(rE) as an anchor, the AEG model focuses on future earnings and earnings growth in the short- and the long-run. The intrinsic value of equity depends on forward earnings and the subsequent growth8. Analogously with the PVEE, the unconstrained AEG model is immune to dividend policy: V0AEG = E 0 ( X 1 ) T −1 E 0 ( X t +1 + rE ⋅ Div t − X t ⋅ R E ) r E +∑ + rE R tE t =1 E ( P + Div T − X T ⋅ R E r E ) + 0 T R TE (AEG) The unconstrained AEG model is a restatement of PVED9 and similar to the RIV model, the valuation of owners’ equity is driven by three factors: 1. Capitalised expected value of earnings in the first period t=1 (PVEE): E0 ( X1 ) rE 2. The present value of capitalised expected abnormal earnings growth over the periods t = 2,3,…,T: T −1 ∑ t =1 3. E 0 ( X t +1 + rE ⋅ Div t − X t ⋅ R E ) r E R tE The present value of the expected difference between the market value of owners’ equity and capitalised value of earnings at the horizon point in time t=T: E 0 ( PT + Div T − X T ⋅ R E r E ) R TE The abnormal earnings growth model embodies the idea that the value of equity is based on what the firm can earn. Given that the assumption of CSR holds, the measures of abnormal 8 Cf. Penman (2007) for further discussion of AEG modelling. 9 Cf. Appendix 1 for the axiomatic rewriting of PVED to AEG valuation model. 14 earnings growth in the AEG model will be clearly linked to the measure of residual income in the RIV model10. Given unbiased accounting and that T≥T*+1, the terminal value in AEG is equal to zero. Hence, the model can be rewritten to obtain a terminal value constrained version: V0AEG( TVC ) = E 0 ( X 1 ) T −1 E 0 ( X t +1 + rE ⋅ Div t − X t ⋅ R E ) r E +∑ rE R tE t =1 (AEG(TVC)) As in the corresponding RIV(TVC) model, the AEG(TVC) will provide a valuation error in the valuation of owners’ equity if accounting is conservatively biased and/or if T<T*+1. (Skogsvik and Juettner-Nauroth, 2007) 3.8. Hypotheses Under the assumption of steady state, Skogsvik and Juettner-Nauroth (2007) suggest that the unconstrained versions of RIV and AEG modelling are immune to accounting conservatism. This does not, however, hold for book value of owners’ equity and PVEE, or for the parsimonious versions of RIV and AEG modelling. Conservative accounting in book value provides a valuation error (-Cb0) of owners’ equity that is equal to the difference between the book value at t=0 (Bv0) and unbiased book value (Bv0(UB)) at t=0 : V0 − P0 = Bv 0 − Bv (0UB ) = −Cb 0 The valuation error in the RIV(TVC) is a function of the expected conservative bias of owners’ equity at horizon point of time11: V0 − P0 = − 10 E 0 ( Cb T* ) R ET* The following expression shows on the equality between the abnormal earnings growth for period t + 1 and the difference between residual income in period t + 1 and period t: E 0 ( X t +1 + rE ⋅ Div t − X t ⋅ R E = E 0 [( X t +1 − rE ⋅ Bv t ) − ( X t − rE ⋅ Bv t −1 )] (Skogsvik and Juettner-Nauroth, 2007) 11 Cf. Appendix 4 for derivation of the measurement error in RIV(TVC). 15 This implies an expected non-positive bias if E0(CbT*) ≥ 0 and that RIV(TVC) accommodates conservative accounting with no valuation error if E0(CbT*) = 0. If t0 < T* it could be expected that E 0 ( Cb T * ) is smaller than Cb 0 . R TE* The RIV(TVC) model [on average] provides a smaller absolute Hypothesis 1: valuation error than the book value of owners’ equity. The valuation error in RIV(PMB) is a function of the error in the estimation of q (PMB) and the book value of owners’ equity at T*12: V0 − P0 = − ( PMB − q ) ⋅ Bv T* R TE* RIV(PMB) will consequently provide a smaller valuation error than RIV(TVC) if: ( PMB − q ) ⋅ Bv T * E ( Cb ) < 0 T* T* T* RE RE Hypothesis 2: The RIV(PMB) model [on average] provides a smaller absolute valuation error than the RIV(TVC) model. The PVEE(rE) valuation model provides a valuation error of owners’ equity equal to difference between capitalised earnings at t=1 and capitalised unbiased earnings at t=1: V0 − P0 = X 1 X 1UB − rET* rET* According to the reasoning in section 2, the PVEE model could be used together with the risk-free interest rate. By capitalising next year estimated earnings with the risk-free interest rate (rf), the denominator is adjusted downwards to adjust for the absence of growth in the numerator. This could potentially capture the value of growth in future earnings that is omitted in PVEE(rE) when capitalising with rE. The adjustment would produce a smaller valuation error if the growth rate of the company is larger than the difference between rE and rf: 12 Cf. Appendix 5 for derivation of the measurement error in RIV(PMB). 16 V0 − P0 = X 1 X 1UB − T rfT rf Under the assumptions above, the following must hold: rf > rE − g PVEE(rf) underestimates fair value (always smaller ⇔ g > β ⋅ ( rm − rf ) valuation error than PVEE(rE)). rf < rE − g PVEE(rf) overestimates fair value (valuation error ⇔ g < β ⋅ ( rm − rf ) size unclear relative to PVEE(rE)). rf = rE − g PVEE(rf) captures growth in earnings. ⇔ g = β ⋅ ( rm − rf ) Hypothesis 3: The Capitalised Earnings Model where earnings are capitalised with the risk-free interest rate [on average] provides a smaller valuation error than earnings capitalised with the required rate of return on equity. The valuation error in AEG(TVC) is equal to the negative present value of the capitalised growth of the conservative bias in period (T*+1) and thus, if the expected change in the conservative bias in (T*+1) equals zero, the AEG(TVC) model could accommodate conservative accounting principles with no valuation error in the valuation of owners’ equity13: V0 − P0 = − Cb T* +1 − Cb T* / rE T* RE If t0 < T* it could be expected that: 13 Cf. Appendix 6 for derivation of the measurement error in AEG(TVC). 17 Cb T* +1 − Cb T* / rE X 1UB X 1 < − . R TE* rET* rET* Hypothesis 4: The AEG(TVC) model [on average] provides a smaller absolute valuation error than PVEE(rE). Skogsvik and Juettner-Nauroth (2007) suggest that the valuation error in the terminal value constrained AEG model is typically smaller than in the corresponding RIV model if the growth of the conservative bias lies within a certain interval of “normal” values. The RIV(TVC) model, on the other hand, provides a smaller valuation error than the AEG(TVC) only when the growth of the conservative bias exhibits more “extreme” values14: Given CSR and steady state, the valuation bias of AEG(TVC) is smaller than in RIV(TVC) only if: -E0(CbT*) · rE < E0[(CbT*+1-CbT*)] < E0(CbT*) · rE Reversely, the RIV(TVC) model is superior to AEG(TVC) only if: E0[(CbT*+1-CbT*)] < -E0(CbT*) · rE or E0[(CbT*+1-CbT*)] >E0(CbT*) (Skogsvik and Juettner-Nauroth, 2007) Under an assumption of steady state, this supports the reasoning in Hypothesis 5: Hypothesis 5: The AEG(TVC) model [on average] provides a smaller absolute valuation error than RIV(TVC). In the next section, the models’ ability to reflect market value and to withstand conservative accounting biases will be empirically evaluated. The results will be discussed on basis of the theoretical reasoning and by testing hypotheses 1-5. 14 Cf. Appendix 7 for a comparison between the measurement errors in RIV(TVC) and AEG(TVC). 18 4. Data 4.1. Data Set, Descriptive Statistics and Consistency Checks Monthly observations of yearly data for 190 currently traded companies on the Stockholm Stock Exchange have been collected from DATASTREAM for the period July 1998 to October 2007. The companies have been categorised into nine industry sectors15 according to the Global Industry Classification Standard (GICS)16: GICS Sector 1998 1999 2000 2001 2002 2003 Consumer Discretionary 5 8 9 11 7 15 Consumer Staples 0 3 3 3 2 3 Energy 1 1 2 2 1 2 Financials 4 10 15 12 6 14 Health Care 2 3 4 3 2 7 Industrials 18 26 33 31 12 33 Information Technology 5 11 15 15 2 19 Materials 5 5 6 6 2 6 Telecommunication Services 1 1 1 2 2 2 Total 41 68 88 85 36 101 Table 1: Sample size measured as number of companies per industry sector and year. 2004 18 3 2 16 7 36 24 9 2 117 2005 19 4 2 15 8 39 21 8 3 119 2006 23 6 3 19 7 44 26 10 4 142 2007 25 7 4 24 8 49 32 9 3 161 Evidently, the number of firms in any year does not total 190. This is explained by the fact that companies enter the sample at different points of time over the studied period. Limitations in analyst coverage further reduce the sample size, and the possible implications from this will be discussed later. Together with Institutional Brokers Estimate System (IBES) consensus estimates17, reported accounting data has served as a starting point in the empirical valuation modelling18. The analyst estimates have been used as a proxy for the market’s expectations on company future book value, earnings and dividends. The average number of estimates available per company and parameter varies with sector and time, e.g. estimates for fiscal period (FY) 4 are rarely observed: 15 The categorisation of companies into industry sector is made to allow for a deeper understanding and discussion of the empirical results. Cf. Appendix 2-3 for more detailed information on the studied sample and the different industry sector characteristics. 16 GICS is an industry classification that consists of 10 sectors, 24 industry groups, 62 industries, and 132 sub-industries. GICS assigns an industry sector name to each company according to its principal business activity, and the standard is widely accepted as a framework for investment research, portfolio management and asset allocation. 17 18 The consensus estimates are the arithmetic average of estimates for the fiscal period indicated. IBES is a system which monitors and gathers the different estimates made by stock analysts on companies of interest to institutional investors. The IBES database covers over 18 000 companies in 60 countries. 19 Fiscal Year 1 Fiscal Year 2 GICS Sector BPS EPS DPS BPS EPS DPS Consumer Discretionary 6.9 8.1 8.9 6.5 8.0 8.5 Consumer Staples 5.8 7.6 7.9 5.2 7.5 7.6 Energy 2.2 3.3 2.8 2.0 2.9 2.6 Financials 7.1 9.9 10.5 6.5 9.7 9.8 Health Care 4.5 5.4 5.8 4.2 5.3 5.5 Industrials 6.7 8.7 9.2 6.2 8.6 8.6 Information Technology 4.8 6.2 5.8 4.4 6.0 5.4 Materials 8.0 10.6 11.2 7.4 10.5 10.6 Telecommunication Services 11.8 14.8 16.7 10.9 15.0 16.0 Table 2: Average number of estimates per company, estimated parameter and fiscal year. BPS 4.6 3.9 1.5 4.4 3.2 4.5 3.1 5.1 8.1 Fiscal Year 3 EPS DPS 5.4 5.8 5.4 5.7 2.0 1.8 6.3 6.5 3.9 4.0 5.9 6.0 3.9 3.6 7.0 7.2 11.1 11.6 BPS 1.2 1.0 0.9 1.0 1.1 1.1 1.1 1.1 1.7 Fiscal Year 4 EPS DPS 1.0 1.0 1.0 1.0 0.1 0.1 0.8 0.7 0.6 0.6 0.8 0.8 0.6 0.6 0.9 1.0 2.4 2.5 Reported accounting information and consensus estimates used in the empirical analysis: Book Value Per Share (BPSt) = BPSt is the net asset value of a company’s securities, expressed in per share terms. BPSt is used as an estimation of Bvt. Earnings Per Share (EPSt) = EPSt is the amount of a company’s profit allocated to each outstanding share of common stock, thus this serves as an indicator of a company’s profitability. EPSt is used as an estimation of Xt. Dividends Per Share (DPSt) = DPSt consists of a company’s common stock dividends on an annualized basis, divided by the weighted average number of common shares outstanding for the year. DPSt is used as an estimation of Divt. Price Per Share (PPSt) = The last price per share represents the market value of owners’ equity per common share outstanding. PPSt is used as an estimation of P t. To ensure comparability and to improve the validity of the empirical results, extensive consistency checks have been carried out to find error in the data. The consistency checks and adjustments include: Currency translations have been made from exchange rate time series where reported information or consensus estimates are reported in other currencies than SEK. 20 Observations with negative earnings or book value forecasts have been excluded19 along with missing observations. BPSt has been estimated where the value is missing. Estimation of BPSt is performed in accordance with CSR and based on information from the previous fiscal period. Consequently, the estimation can only be performed for FY1-FY4 where both EPS and DPS estimates are observed in the previous period: BPS FYt = BPS FYt −1 + EPS FYt − DPS FYt −1 To empirically evaluate the models and to allow for a paired sample t-test of the hypotheses, the data has been limited to observations with complete accounting information and consensus estimates for three fiscal periods. The terminal point of time is set to t=T=3 because of the limited number of analyst estimates for FY4. The total number of complete observations in the data sample is 8 504: GICS Sector 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Total Consumer Discretionary 28 88 99 63 76 153 174 197 234 231 1343 Consumer Staples 0 28 36 25 4 32 36 46 64 55 326 Energy 5 2 4 5 5 16 10 4 24 34 109 Financials 23 93 127 79 65 133 139 137 192 202 1190 Health Care 12 25 31 14 18 63 79 80 82 67 471 Industrials 98 234 315 194 112 296 365 395 485 453 2947 Information Technology 23 81 139 68 7 127 218 171 225 230 1289 Materials 25 52 71 33 24 63 94 76 100 87 625 Telecommunication Services 5 12 12 15 20 24 24 29 37 26 204 Total 219 615 834 496 331 907 1139 1135 1443 1385 8504 Table 3: Total number of complete observations per industry sector and year (e.g. 7 companies were observed in Consumer Discretionary sector in 2002. If full accounting information and estimates would have been available for all companies and months this year, the number of complete observations would have been 84. With missing information, however, the number of complete observations is only 76). The number of observations per sector and year increases from 1998 to 2007, and any biases that this may induce on the results will be discussed and empirically tested. 19 The reasoning behind the exclusion of negative observations is self-evident, e.g. valuing owners’ equity with negative earnings forecasts would imply a negative value in the capitalised earnings model. Naturally, this can not hold. 21 5. Empirical Analysis In this section, the models’ accuracy in determining the market value of owners’ equity and the impact of conservative accounting will be evaluated. Hypotheses 1-5 will be tested. 5.1. Modelling Assumptions The market value (Pt) is assumed to reflect the fair value of owners’ equity at the valuation point of time (t=0) given all available information. In order to isolate the valuation error, it is assumed that the valuation of owners’ equity would be correct if the accounting was unbiased and the company had reached steady state at t0. Consequently, any deviations from Pt are explained by conservative bias and/or the business goodwill/badwill (i.e. T<T*). The valuation error (V.E.) will be calculated as the difference between the market value of owners’ equity at time t=0 (estimated by PPSt) (P0) and the estimated value (V0): V.E. = V0 − P0 (V.E.) To allow for comparison between models and over industry sectors, the absolute valuation error (Abs(V.E.)) will be computed: Abs( V.E.) = V0 − P0 (Abs(V.E.)) All valuation errors will be normalised using the market value at t=0, and the normalised valuation errors will henceforth be referred to as the valuation errors in the models: V.E. V0 − P0 = P0 P0 Abs( V.E.) V0 − P0 = P0 P0 The differences in average absolute valuation errors between models will be tested with paired t-tests on the equality of means20, and at the 5 percent (**) level. Significance is also reported for the 1 (***) and 10 percent (*) levels. All results will be presented with 3 different alternative 20 The t-test rests on an assumption of normal distribution in data. 22 hypotheses, the computed t-statistics and the associated p-values as well as a computed 95 percent confidence interval for the mean values. To calculate the cost of equity capital for companies, an estimate of the equity risk premium is central. The required return on equity will be the risk-free interest rate plus a risk premium. The risk premium will be the equity risk premium for the market, adjusted for the risk of the company. This requires an estimate of the prospective equity risk premium, whereas by definition the only premium which can be measured is the historical risk premium. In practice therefore, the historical risk premium is used as a starting point for assumptions about the future. Generally, in inferring the future risk premium from historical data, the implicit assumption is made that the historical risk premium, measured over many years, is an unbiased estimate of the future premium21. Over a 105-year period between 1900 and 2004, the annualized geometric equity risk premium, relative to bills, was 5.5 percent in Sweden. Averaged across the world index, the risk premium relative to bills was 4.7 percent. Across the world index, the risk premium relative to bonds averaged 4.0 percent, while for Sweden it was 5.0 percent22. (Dimson et. al., 2005) The historical estimates should be considered to be too high as forecasts of the future. Increased diversification, for example, has decreased the required risk premium for investors and the past returns have therefore been advantaged by the decline in the risk faced by investors. This means that when developing forecasts for the future, the historical risk premium should be adjusted downward for the impact of these factors. (Dimson et. al., 2005) An estimate of a plausible, forward-looking risk premium for the Swedish market would consequently be on the order of 4.0 percent (rm - rf = 4.0%). This assumption will later be robustness tested to infer its impact on the empirical results. The nominal risk-free interest rate at the time for valuation (t=0) is given by the midpoint between the bid and offered rates for the 10-year Swedish Government zero coupon. The risk adjustment of the equity market risk premium is measured by the systematic risk of a company (beta). Beta is used as a measure of the extent to which a share’s performance fluctuates with the market, relative to average. A raw beta is estimated at each time for valuation (t=0) by regressing 400 points of daily returns of the relevant GICS Level 1 Sector Group index23 21 An unbiased estimate of the risk premium required by investors would tell what future returns can be expected from the equity market, relative to risk-free investments. A low (high) risk premium would automatically imply low (high) future returns from equities. If this were not the case, then the stock market would ensure that share prices rapidly rose (fell) until promised returns were aligned with required returns. 22 This historical risk premium is summarised by the geometric mean of historic returns. The forward- looking risk premium, however, should more appropriately be measured by the arithmetic mean, since it represents the mean of all returns that may possibly occur. 23 Cf. Appendix 2 for detailed information on the GICS Level 1 Sector Group indexes. 23 against the market proxy return Affarsvarlden General Index (AFGX)24. The industry sector estimated beta is applied to all companies in the specific industry sector at the time for valuation25: GICS Sector 1998 1999 Consumer Discretionary 0.9272 0.9313 Consumer Staples 0.3979 Energy 0.8651 0.8464 Financials 0.8789 0.9144 Health Care 0.8365 0.7170 Industrials 0.8687 0.8064 Information Technology 1.5740 1.6932 Materials 0.8042 0.7479 Telecommunication Services 1.0981 1.1438 Table 4: Average beta values per sector and year. 2000 0.7403 0.2182 0.3718 0.6868 0.3538 0.4254 1.8373 0.4068 1.2231 2001 0.6383 0.1134 0.3845 0.6221 0.1109 0.3752 1.9835 0.3038 1.1501 2002 0.8589 0.0996 0.7542 0.8779 0.4046 0.6816 1.9807 0.5130 1.2016 2003 0.8786 0.2045 0.8645 1.0167 0.6593 0.8705 2.0107 0.6295 1.2447 2004 0.7507 0.2786 0.9503 0.9267 0.7169 0.9573 2.0587 0.6749 1.0413 2005 0.7104 0.3777 0.9954 0.8103 0.5603 0.9764 2.0658 0.6275 1.0100 2006 0.8150 0.5132 1.1527 0.9969 0.6733 1.1285 1.2986 0.9587 0.9124 2007 0.8852 0.5723 1.1704 1.0552 0.6488 1.1684 1.0151 1.1475 0.8280 Under the assumption that the Capital Asset Pricing Model (CAPM) holds, the index model is used to derive the equity cost of capital by risk adjustment of the equity market risk premium: E( rE ) = rf + β ⋅ [E(rm ) − rf ] (CAPM) The PMB values used in the testing of RIV(PMB) has been obtained from Runsten (1998). Runsten (1998) discusses the sources and factors that primarily influence the level of expected business goodwill/badwill at t=T*, and provides a calculation of PMB values for different industry sectors. Runsten’s (1998) industry sector categorisation differs from GICS, and thus, assumptions about applicable sectors have been required. The assumptions are based on expectations about e.g. balance sheet composition and business models, which are factors that influence the expected level of PMB: GICS Sector Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Table 5: PMB values used in ranked in ascending order. 24 Runsten (1998) Classification PMB Rank Consumer Goods 0.72 7 Consumer Goods 0.72 7 Shipping 0.65 6 Real Estate 0.56 3 Pharmaceuticals 1.74 9 Engineering 0.33 1 Consultants and Computer 0.59 4 Chemicals 0.44 2 Consultants and Computer 0.59 4 the empirical modelling per GICS industry sector and AFGX measures the Stockholm Stock Exchange and was started in 1937. Base: 28 December 1979 = 100. AFGX is a capital-weighted index and it is calculated by multiplying the number of shares in each company with the bid price of the most numerous type of share in the company. 25 Cf. Appendix 8 for the historical beta values estimated at (t=0) and for each industry sector. 24 Runsten (1998) does not provide estimates of PMB for companies in the Financials sector, and thus the closest match in terms of balance sheet composition and business model has been assumed to be Real Estate companies (n.b. Real Estate companies are included in the GICS Financials industry sector). It should also be noted that Runsten’s (1998) research did not have any possibility to cover the evolvement of the Information Technology sector from 1998 and forward. The applied PMB value from Runsten (1998) for this sector is therefore potentially misleading. Parallel to using Runsten’s (1998) PMB values, an estimation of q values including the valuation bias from companies not being in steady state (Q) is performed in the empirical modelling. The estimation is obtained through reverse-engineering the q-value for each observation that would imply zero valuation error in RIV(TVC) if the extension was added to the valuation: ( P0 − V0RIV ( TVC ) ) ⋅ R TE Qi = Bv T (Q) Q is subsequently calculated as the average of all reverse-engineered values per industry sector. The discounting of present values in the modelling is performed by adjusting the yearly interest rate at t=0 to fit with the monthly data and the assumptions about when in time transactions occur. 25 5.2. Book Value of Owners’ Equity The book value of owners’ equity is given in the modelling by the company reported information at t=0 (V0 = Bv0 = BPS0). As stipulated in section 2, the valuation error provided in book value of owners’ equity with conservative accounting is equal to the difference between the book value at t=0 and unbiased book value at t=0 (-Cb0). A negative (positive) valuation error would consequently imply that book value on average underestimates (overestimates) the correct value of owners’ equity: 1.00 1.40 0.80 1.20 0.60 1.00 0.40 V.E. 0.80 0.00 0.60 -0.20 -0.40 0.40 -0.60 0.20 -0.80 Abs(V.E.(BV)) Chart 1: Average valuation error and absolute valuation error in book value measured per sector. 2007 Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Chart 2: Average absolute valuation error in book value, measured per sector and historically. Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary -0.5640 0.0109 -0.5854 -0.5426 0.6350 0.0074 0.6205 0.6496 6 Consumer Staples -0.7367 0.0077 -0.7518 -0.7215 0.7367 0.0077 0.7215 0.7518 8 Energy -0.1504 0.0448 -0.2393 -0.0616 0.4412 0.0204 0.4007 0.4817 2 Financials -0.4181 0.0091 -0.4361 -0.4002 0.4745 0.0064 0.4619 0.4871 4 Health Care -0.7305 0.0174 -0.7647 -0.6964 0.8050 0.0077 0.7900 0.8200 9 Industrials -0.5293 0.0062 -0.5415 -0.5172 0.5857 0.0041 0.5776 0.5938 5 Information Technology -0.5603 0.0135 -0.5868 -0.5338 0.6639 0.0092 0.6459 0.6819 7 Materials -0.3073 0.0117 -0.3304 -0.2843 0.3620 0.0089 0.3446 0.3795 1 Telecommunication Services -0.4065 0.0251 -0.4560 -0.3569 0.4524 0.0209 0.4112 0.4936 3 Table 6: Average valuation error and absolute valuation error in book value with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. The average valuation error shows that the book value underestimates the fair value of owners’ equity across all industry sectors. The average valuation error is the smallest for Energy and Materials companies. The industry sectors with the largest valuation error are Consumer Staples and Health Care. Evaluating the absolute valuation error shows that Materials and Energy together with Telecommunication Services have the smallest valuation error. Health Care, Consumer Staples, and Information Technology have the largest average absolute valuation error. Putting a 95 percent confidence interval on all mean absolute values would imply an absolute deviation from the fair value between 34.46 percent and 82.00 percent. 26 2006 2005 2004 2003 2002 2001 2000 1999 1998 Materials Information Technology Industrials Health Care Financials Energy Consumer Staples V.E.(BV) Telecommunication Services 0.00 -1.00 Consumer Discretionary V.E. 0.20 M.E. 95 % C.I. Abs(M.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.5189 0.0041 -0.5270 -0.5108 0.5862 0.0029 0.5805 0.5919 Table 7: Average valuation error and absolute valuation error in book value with standard error and a 95 percent confidence interval (C.I.). Aggregated for all industry sectors, the average valuation error in book value is -51.89 (52.70;-51.08) percent. The average absolute valuation error is 58.62 percent and ranges between 58.05 and 59.19 percent within a 95 percent confidence interval. 5.3. The Terminal Value Constrained Residual Income Valuation Model RIV(TVC) is calculated by using company reported information and available consensus estimates at t=0. As stipulated in section 2, the valuation error provided in RIV(TVC) with conservative accounting is a function of the conservative bias of owners’ equity at horizon point of time. A negative (positive) valuation error would consequently imply that RIV(TVC) on average underestimates (overestimates) the correct value of owners’ equity: 0.80 1.20 0.60 1.00 0.40 0.80 V.E. 0.00 -0.20 0.60 0.40 -0.40 0.20 -0.60 Abs(V.E.(RIV(TVC))) Chart 3: Average valuation error and absolute valuation error in RIV(TVC) per sector. 2007 Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Chart 4: Average absolute valuation error in RIV(TVC) measured per sector and historically. Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary -0.4334 0.0119 -0.4568 -0.4101 0.5544 0.0073 0.5402 0.5686 6 Consumer Staples -0.5808 0.0066 -0.5938 -0.5678 0.5808 0.0066 0.5678 0.5938 7 Energy -0.1020 0.0431 -0.1874 -0.0165 0.4141 0.0191 0.3761 0.4520 3 Financials -0.3629 0.0080 -0.3786 -0.3471 0.4105 0.0058 0.3991 0.4219 2 Health Care -0.6358 0.0169 -0.6690 -0.6027 0.7095 0.0086 0.6927 0.7264 9 Industrials -0.4113 0.0064 -0.4238 -0.3988 0.4873 0.0042 0.4791 0.4955 5 Information Technology -0.5046 0.0132 -0.5304 -0.4788 0.6052 0.0093 0.5869 0.6235 8 Materials -0.1928 0.0110 -0.2144 -0.1711 0.2834 0.0072 0.2692 0.2976 1 Telecommunication Services -0.3764 0.0238 -0.4233 -0.3294 0.4148 0.0204 0.3745 0.4551 4 Table 8: Average valuation error and absolute valuation error in RIV(TVC) with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. The average valuation error shows that the RIV(TVC) underestimates the fair value of owners’ equity across all industry sectors. The average valuation error in RIV(TVC) is the smallest for Energy and Materials companies. The industry sectors with the largest valuation error 27 2006 2005 2004 2003 2002 2001 2000 1999 1998 Materials Information Technology Industrials Health Care Financials Energy Consumer Staples V.E.(RIV(TVC)) Telecommunication Services 0.00 -0.80 Consumer Discretionary V.E. 0.20 are Health Care and Consumer Staples. Evaluating the absolute valuation error shows that Materials and Financials together with Energy have the smallest valuation error. Health Care, Information Technology, and Consumer Staples have the largest average absolute valuation error. Putting a 95 percent confidence interval on all mean values would imply an absolute deviation from the fair value between 26.92 percent and 72.64 percent. Comparing the results from RIV(TVC) with the results from book value of owners’ equity shows that RIV(TVC) seems to provide a smaller absolute valuation error across all the sectors. This supports the theoretical reasoning in previous sections and is suggested in hypothesis 1. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.4202 0.0041 -0.4283 -0.4121 0.5033 0.0028 0.4977 0.5088 Table 9: Average valuation error and absolute valuation error in RIV(TVC) with standard error and a 95 percent confidence interval (C.I.). Aggregated for all industry sectors, the average valuation error in RIV(TVC) is -42.02 (42.83;-41.21) percent. The average absolute valuation error is 50.33 percent and ranges between 49.77 and 50.88 percent within a 95 percent confidence interval. 5.4. The Permanent Measurement Bias Extended Version of RIV(TVC) RIV(PMB) is calculated by using company reported information and available consensus estimates at t=0 together with PMB values from Runsten (1998). As stipulated in section 2, the valuation error provided in RIV(PMB) with conservative accounting is a function of the difference between the applied PMB value and the q-value that would imply zero valuation error. A negative (positive) valuation error would consequently imply that RIV(PMB) on average underestimates (overestimates) the correct value of owners’ equity: 0.80 2.50 0.60 2.00 0.40 V.E. 1.00 0.00 0.50 -0.20 Abs(V.E.(RIV(PMB))) Chart 5: Average valuation error and absolute valuation error in RIV(PMB) per sector. 28 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 Materials Information Technology Industrials Health Care Financials Energy Consumer Staples V.E.(RIV(PMB)) Telecommunication Services 0.00 -0.40 Consumer Discretionary V.E. 1.50 0.20 Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Chart 6: Average absolute valuation error in RIV(PMB) measured per sector and historically. Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary -0.0946 0.0183 -0.1304 -0.0587 0.5383 0.0112 0.5163 0.5603 8 Consumer Staples -0.3466 0.0116 -0.3695 -0.3237 0.3498 0.0113 0.3275 0.3721 3 Energy 0.5070 0.0787 0.3510 0.6631 0.6480 0.0685 0.5122 0.7838 9 Financials -0.0406 0.0114 -0.0629 -0.0182 0.2820 0.0080 0.2662 0.2977 1 Health Care -0.1164 0.0275 -0.1704 -0.0624 0.4266 0.0199 0.3874 0.4657 6 Industrials -0.2473 0.0079 -0.2628 -0.2318 0.4083 0.0052 0.3982 0.4185 5 Information Technology -0.2419 0.0192 -0.2797 -0.2042 0.5322 0.0140 0.5047 0.5596 7 Materials 0.1147 0.0151 0.0850 0.1444 0.3202 0.0092 0.3020 0.3383 2 Telecommunication Services -0.0734 0.0328 -0.1381 -0.0087 0.3967 0.0181 0.3610 0.4325 4 Table 10: Average absolute valuation error in RIV(PMB) with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. The average valuation error shows that the RIV(PMB) underestimates the fair value of owners’ equity for all industry sectors with the exception for Energy and Materials. The average valuation error in RIV(PMB) is the smallest for Financials and Telecommunication Services. The industry sectors with the largest valuation error are Energy and Consumer Staples. Evaluating the absolute valuation error shows that Financials and Materials, together with Consumer Staples have the smallest valuation error. Energy, Consumer Discretionary, and Information Technology, have the largest average absolute valuation error. Putting a 95 percent confidence interval on all mean values would imply an absolute deviation from the fair value between 26.62 percent and 78.38 percent. Comparing the results from RIV(PMB) with the results from RIV(TVC) shows that RIV(PMB) seem to provide a smaller absolute valuation error across all the sectors with exception for Energy and Materials. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.1495 0.0059 -0.1611 -0.1380 0.425 0.004 0.4172 0.4328 Table 11: Average valuation error and absolute valuation error in RIV(PMB) with standard error and a 95 percent confidence interval (C.I.). Aggregated for all industry sectors, the average valuation error in RIV(PMB) is -14.95 (16.11;-13.80) percent. The average absolute valuation error is 42.50 percent and ranges between 41.72 and 43.28 percent within a 95 percent confidence interval. As shown, the adjustment of RIV(TVC) with Runsten’s (1998) PMB values does not eliminate valuation errors. This could be explained by the fluctuation over time in the factors that influence the level of business goodwill/badwill at time t=T*. Ideally, the PMB should therefore be calculated specifically for each company and year. (Runsten, 1998) An alternative approach could be to make an extension to the RIV(TVC) model with estimated q values (Q) that capture not only the conservative bias (i.e. the assumption of steady state is released). This could potentially improve the accuracy of the parsimonious RIV(TVC) model: 29 GICS Sector 1998 1999 2000 2001 2002 2003 Consumer Discretionary 2.9925 5.0637 2.9190 2.7656 1.7971 1.0825 Consumer Staples 1.8209 1.2385 1.7823 2.2079 1.5433 Energy -0.2589 -0.2224 -0.3752 -0.4610 -0.3425 -0.1156 Financials 0.9593 1.1643 1.6864 0.8864 0.8998 0.6246 Health Care -0.9127 1.0154 1.4695 1.2846 2.3460 2.2909 Industrials 1.5278 1.6377 1.4173 1.0635 0.6796 0.4801 Information Technology 3.4601 4.2168 9.5600 1.7779 1.7180 1.0137 Materials 0.4895 0.5333 0.2473 0.1940 0.3412 0.2221 Telecommunication Services 5.3307 6.1903 7.1655 2.5016 0.7805 0.2745 Table 12: Q estimated per industry sector and year. 2004 1.8457 1.8594 0.3508 0.8847 3.1286 0.9753 2.5582 0.3333 0.3417 2005 2.2272 2.3799 0.7540 0.8610 3.8374 1.2712 2.0303 0.3718 0.1172 2006 2.4948 3.7260 0.9783 1.0079 4.2589 1.7798 2.1712 0.8015 1.0612 2007 3.1321 4.6575 0.8008 1.1461 4.0137 2.4021 2.4691 0.7353 1.8053 Over time, the average Q values have varied, and since 2002 the estimated values have generally increased across all sectors. Notably, Telecommunication Services, Information Technology and Consumer Discretionary show extremely high Q values during year 1998-2000. The average levels of the calculated Q values are higher than the PMB values obtained from Runsten (1998). Runsten’s (1998) PMB values are calculated with a horizon point of time beyond FY3. With a shorter horizon it is more likely that the companies have not reached steady state and is therefore still earning abnormal profits, which would explain the higher Q values and make direct comparisons between the estimated values difficult. The average overestimation in RIV(PMB) for Energy and Materials, could be explained by flawed assumption about the industry sector categorisation. Hence, the applicability of Runsten’s (1998) PMB values could lead to inaccurate adjustment of the RIV(TVC) model. Rank Rank PMB Q GICS Sector Runsten (1998) Classification PMB Q Consumer Discretionary Consumer Goods 0.72 7 2.50 6 Consumer Staples Consumer Goods 0.72 7 2.67 7 Energy Shipping 0.65 6 0.44 1 Financials Real Estate 0.56 3 1.03 3 Health Care Pharmaceuticals 1.74 9 3.05 8 Industrials Engineering 0.33 1 1.43 4 Information Technology Consultants and Computer 0.59 4 3.08 9 Materials Chemicals 0.44 2 0.46 2 Telecommunication Services Consultants and Computer 0.59 4 1.69 5 Table 13: Comparison between Runsten’s (1998) PMB values and estimated Q, both ranked in ascending order. The industry sectors with the lowest Q values are Energy and Materials together with Financials. Information Technology, Health Care, and Consumer Staples provide the highest Q values on average. Analogously with RIV(PMB), the valuation error in RIV(Q) is a function of the error in the estimation (Q) of q and the book value of owners’ equity at T: V0 − P0 = − ( Q − q ) ⋅ Bv T R ET With positive PMB values, RIV(Q) will consequently provide a smaller valuation error than RIV(PMB) if ( Q − q ) < ( PMB − q ) . 30 The RIV(Q) model [on average] provides a smaller valuation Sub-Hypothesis: error than RIV(PMB). RIV(Q) is calculated by using company reported information and available consensus estimates at t=0. As stipulated in section 2, the valuation error provided in RIV(Q) is a function of the difference between the applied Q value and the q-value that would imply zero valuation error. A negative (positive) valuation error would consequently imply that RIV(Q) on average 3.00 1.00 2.50 0.80 2.00 Abs(V.E.(RIV(Q))) Chart 7: Average valuation error and absolute valuation error in RIV(Q) per sector. 2007 Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Chart 8: Average absolute valuation error in RIV(Q) measured per sector and historically. Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary 0.7448 0.0349 0.6763 0.8134 0.9979 0.0299 0.9393 1.0565 8 Consumer Staples 0.2868 0.0268 0.2341 0.3395 0.4654 0.0174 0.4312 0.4997 3 Energy 0.3117 0.0671 0.1786 0.4448 0.5239 0.0535 0.4178 0.6300 6 Financials 0.2282 0.0145 0.1997 0.2568 0.3934 0.0112 0.3714 0.4153 2 Health Care 0.2748 0.0368 0.2024 0.3471 0.5015 0.0313 0.4400 0.5631 4 Industrials 0.2990 0.0135 0.2726 0.3255 0.5109 0.0111 0.4891 0.5327 5 Information Technology 0.8676 0.0456 0.7782 0.9570 1.0643 0.0422 0.9815 1.1470 9 Materials 0.1313 0.0153 0.1011 0.1614 0.3282 0.0095 0.3095 0.3469 1 Telecommunication Services 0.4906 0.0508 0.3905 0.5908 0.7571 0.0307 0.6965 0.8177 7 Table 14: Average valuation error and absolute valuation error in RIV(Q) with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. The average valuation error shows that the RIV(Q) on average overestimates the fair value of owners’ equity for all industry sectors. The average valuation error in RIV(Q) is the smallest for Materials and Financials. The industry sectors with the largest valuation error are Information Technology and Consumer Discretionary. Evaluating the absolute valuation error shows that Materials and Financials together with Consumer Staples have the smallest valuation error. Information Technology, Consumer Discretionary, and Telecommunications Services, have the largest average absolute valuation error. Putting a 95 percent confidence interval on all mean values would imply an absolute deviation from the fair value between 30.95 percent and 114.70 percent. 31 2006 2005 2004 2003 2002 1998 Materials Telecommunication Services V.E.(RIV(Q)) Information Technology 0.00 Industrials 0.00 Health Care 0.50 Financials 0.20 Energy 1.00 Consumer Staples 0.40 2001 1.50 2000 0.60 1999 V.E. 1.20 Consumer Discretionary V.E. underestimates (overestimates) the correct value of owners’ equity: Comparing the results from RIV(Q) with the results from RIV(PMB) shows that RIV(Q) seems to provide a larger absolute valuation error across all the sectors, with exception for Energy companies. This contradicts the sub-hypothesis. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.4363 0.0110 0.4148 0.4578 0.6456 0.0097 0.6266 0.6646 Table 15: Average valuation error and absolute valuation error in RIV(Q) with standard error and a 95 percent confidence interval (C.I.). Aggregated for all industry sectors, the average valuation error in RIV(Q) is 43.63 (41.48;45.78) percent. The average absolute valuation error is 64.56 percent and ranges between 62.66 and 66.46 percent within a 95 percent confidence interval. 5.5. The Capitalised Earnings Model (Required Rate of Return on Equity) PVEE(rE) is calculated by using consensus estimates for next year’s earnings at t=0 and the estimated company required rate of return on equity. As stipulated in section 2, the valuation error provided in PVEE(rE) with conservative accounting is the difference between capitalised earnings and capitalised unbiased earnings at t=0. A negative (positive) valuation error would consequently imply that PVEE(rE) on average underestimates (overestimates) the correct value of owners’ equity: 3.50 0.60 3.00 0.40 2.50 0.20 2.00 Abs(V.E.(PVEE(rE))) Chart 9: Average valuation error and absolute valuation error in PVEE(rE) per sector. 32 2007 2006 2005 2004 2003 2002 2001 2000 1998 Telecommunication Services V.E.(PVEE(rE)) Materials 0.00 Information Technology -0.60 Industrials 0.50 Health Care -0.40 Financials 1.00 Energy -0.20 Consumer Staples 1.50 Consumer Discretionary 0.00 1999 V.E. V.E. 0.80 Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Chart 10: Absolute average valuation error in PVEE(rE) measured per sector and historically. V.E. 95 % C.I. GICS Sector Mean Std. Error Lower Upper Consumer Discretionary 0.0109 0.0170 -0.0224 0.0443 Consumer Staples 0.2039 0.0188 0.1669 0.2410 Energy 0.2217 0.0972 0.0292 0.4143 Financials -0.1045 0.0091 -0.1223 -0.0867 Health Care -0.3514 0.0167 -0.3843 -0.3185 Industrials -0.0343 0.0093 -0.0525 -0.0161 Information Technology -0.4500 0.0114 -0.4723 -0.4278 Materials 0.2990 0.0291 0.2418 0.3561 Telecommunication Services -0.3902 0.0230 -0.4356 -0.3449 Table 16: Average valuation error and absolute valuation error in PVEE(rE) interval (C.I.) per sector and ranked in ascending order. Abs(V.E.) Mean Std. Error 0.4399 0.0120 0.2971 0.0145 0.6696 0.0758 0.2581 0.0059 0.4536 0.0102 0.3334 0.0070 0.5237 0.0086 0.4829 0.0248 0.4191 0.0203 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.4163 0.4635 5 0.2685 0.3257 2 0.5194 0.8198 9 0.2464 0.2697 1 0.4336 0.4737 6 0.3197 0.3470 3 0.5069 0.5405 8 0.4341 0.5316 7 0.3790 0.4592 4 and a 95 percent confidence The average valuation error shows that the PVEE(rE) underestimates or overestimates the fair value of owners’ equity depending on industry sector. On average, the valuation error is relatively small and negative in Industrials and Financials, whereas for Consumer Discretionary companies the model shows small but positive average errors. Information Technology, Telecommunication Services, and Health Care all show large negative valuation errors. The lowest average absolute valuation error is provided in Financials, Consumer Staples and Industrials. Energy, Information Technology and Materials, however, have the largest average absolute valuation error. Putting a 95 percent confidence interval on all mean values would imply an absolute deviation from the fair value between 24.64 percent and 81.98 percent. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.0892 0.0059 -0.1008 -0.0776 0.3911 0.0042 0.3828 0.3994 Table 17: Average valuation error and absolute valuation error in PVEE(rE) with standard error and a 95 percent confidence interval (C.I.). Aggregated for all industry sectors, the average valuation error in PVEE(rE) is -8.92 (-10.08;7.76) percent. The average absolute valuation error is 39.11 percent and ranges between 38.28 and 39.94 percent within a 95 percent confidence interval. 5.6. The Capitalised Earnings Model (The Risk-free Interest Rate) PVEE(rf) is calculated by using consensus estimates for next year’s earnings at t=0 and the risk-free interest rate at t=0. The valuation error provided in PVEE(rf) with conservative accounting is analogue with the V.E. in PVEE(rE) and equals the difference between capitalised earnings and capitalised unbiased earnings at t=0. A negative (positive) valuation error would consequently imply that PVEE(rf) on average underestimates (overestimates) the correct value of owners’ equity: 33 1.40 7.00 1.20 6.00 1.00 5.00 V.E.(PVEE(rf)) Abs(V.E.(PVEE(rf))) Chart 11: Average valuation error and absolute valuation error in PVEE(rf) per sector. 2007 Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Chart 12: Absolute average valuation error in PVEE(rf) measured per sector and historically. Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary 0.7884 0.0291 0.7313 0.8454 0.9235 0.0259 0.8726 0.9744 7 Consumer Staples 0.6116 0.0210 0.5703 0.6528 0.6225 0.0199 0.5832 0.6617 2 Energy 1.2600 0.1609 0.9410 1.5790 1.4204 0.1480 1.1270 1.7139 9 Financials 0.6572 0.0170 0.6237 0.6906 0.7346 0.0141 0.7069 0.7624 5 Health Care 0.0313 0.0249 -0.0177 0.0803 0.4127 0.0162 0.3809 0.4445 1 Industrials 0.7506 0.0140 0.7232 0.7779 0.8263 0.0124 0.8019 0.8506 6 Information Technology 0.3955 0.0284 0.3398 0.4512 0.7018 0.0233 0.6560 0.7476 4 Materials 1.1402 0.0417 1.0582 1.2222 1.1860 0.0397 1.1081 1.2638 8 Telecommunication Services 0.2360 0.0489 0.1395 0.3324 0.6274 0.0269 0.5743 0.6805 3 Table 18: Average valuation error and absolute valuation error in PVEE(rf) with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. The average valuation error shows that the PVEE(rf) overestimates the fair value of owners’ equity across all industry sectors. The average valuation error in PVEE(rf) is the smallest for Health Care, Telecommunication Services together with Information Technology. The industry sectors with the largest valuation error are Energy, Materials and Consumer Discretionary. Evaluating the absolute valuation error shows that Health Care, Consumer Staples and Telecommunication Services have the smallest valuation error. Energy, Materials and Consumer Discretionary have the largest average absolute valuation error. Putting a 95 percent confidence interval on all mean values would imply an absolute deviation from the fair value between 38.03 percent and 171.39 percent. Comparing the results from PVEE(rf) with the results of PVEE(rE) shows that PVEE(rf) seem to provide a smaller absolute valuation error only for the Health Care sector. The difference in valuation errors between PVEE(rf) and PVEE(rE) is tested in hypothesis 3. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.6673 0.0097 0.6483 0.6863 0.8085 0.0083 0.7922 0.8248 Table 19: Average valuation error and absolute valuation error in PVEE(rf) with standard error and a 95 percent confidence interval (C.I.). 34 2006 2005 2004 2003 2002 1998 Telecommunication Services 0.00 Materials 0.00 Information Technology 1.00 Industrials 0.20 Health Care 2.00 Financials 0.40 Energy 3.00 Consumer Staples 0.60 2001 4.00 2000 0.80 1999 V.E. 8.00 Consumer Discretionary V.E. 1.60 Aggregated for all industry sectors, the average valuation error in PVEE(rf) is 66.73 (64.83;68.63) percent. The average absolute valuation error is 60.65 percent and ranges between 79.22 and 82.48 percent within a 95 percent confidence interval. 5.7. The Terminal Value Constrained Abnormal Earnings Growth Valuation Model AEG(TVC) is calculated by using company reported information and available consensus estimates at t=0. As stipulated in section 2, the valuation error provided in AEG(TVC) with conservative accounting is a function of the conservative bias of owners’ equity at horizon point of time. A negative (positive) valuation error would consequently imply that AEG(TVC) on 2.00 0.60 1.80 0.50 1.60 0.40 1.40 0.30 1.20 Chart 13: Average valuation error and absolute measurement in AEG(TVC) measured per sector. V.E. GICS Sector Mean Std. Error Consumer Discretionary 0.2316 0.0177 Consumer Staples 0.3983 0.0231 Energy 0.2674 0.0749 Financials -0.0652 0.0090 Health Care -0.0721 0.0174 Industrials 0.1675 0.0104 Information Technology -0.1816 0.0169 Materials 0.3226 0.0229 Telecommunication Services -0.1809 0.0218 Table 20: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 2007 Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services Chart 14: Absolute average valuation error in AEG(TVC) measured per sector and historically. 95 % C.I. Lower Upper 0.1969 0.2662 0.3529 0.4437 0.1189 0.4159 -0.0829 -0.0476 -0.1064 -0.0378 0.1472 0.1879 -0.2147 -0.1485 0.2776 0.3675 -0.2239 -0.1379 error in AEG(TVC) Abs(V.E.) Mean Std. Error 0.4580 0.0140 0.4314 0.0212 0.5817 0.0560 0.2505 0.0056 0.3118 0.0104 0.3424 0.0088 0.4304 0.0129 0.4028 0.0207 0.2793 0.0159 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.4306 0.4854 8 0.3898 0.4731 7 0.4706 0.6928 9 0.2394 0.2616 1 0.2913 0.3323 3 0.3251 0.3597 4 0.4051 0.4557 6 0.3621 0.4436 5 0.2480 0.3106 2 and a 95 percent confidence The average valuation error shows that the AEG(TVC) underestimates the fair value of owners’ equity for Telecommunications Services, Information Technology, Health Care, and Financials and overestimates the fair value of owners’ equity for Consumer Staples, Materials, Consumer Discretionary, Industrials, and Energy. The AEG(TVC) provides the smallest valuation error on average for Financials and Health Care. The industry sectors with the largest valuation error are Consumer Staples and Materials. Evaluating the absolute valuation error shows 35 2006 2005 2004 2003 2002 1998 Materials Abs(V.E.(AEG(TVC))) Telecommunication Services V.E.(AEG(TVC)) Information Technology 0.00 Industrials -0.30 Health Care 0.20 Financials 0.40 -0.20 Energy 0.60 -0.10 Consumer Staples 0.80 0.00 2001 1.00 0.10 2000 0.20 1999 V.E. 0.70 Consumer Discretionary V.E. average underestimates (overestimates) the correct value of owners’ equity: that Financials, Telecommunication Services, and Health Care have the smallest valuation error. Putting a 95 percent confidence interval on all mean values would imply an absolute deviation from the fair value between 23.94 percent and 69.28 percent. Energy, Consumer Discretionary, and Consumer Staples have the largest average absolute valuation error. Comparing the results from AEG(TVC) with the results from PVEE(rE) shows that AEG(TVC) seem to provide a smaller absolute valuation error across all the sectors with exception for Industrials, Consumer Discretionary, and Consumer Staples. Comparing the results with those from RIV(TVC), the AEG(TVC) seems to provide a smaller valuation error of the fair value of owners’ equity with exception for Energy and Materials. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.0920 0.0062 0.0799 0.1042 0.3688 0.0048 0.3594 0.3783 Table 21: Average valuation error and absolute valuation error in AEG(TVC) with standard error and a 95 percent confidence interval (C.I.). Aggregated for all industry sectors, the average valuation error in AEG(TVC) is 9.20 (7.99;10.42) percent. The average absolute valuation error is 36.88 percent and ranges between 35.94 and 37.83 percent within a 95 percent confidence interval. 36 5.8. Testing of Hypothesis 1 Hypothesis 1 suggests that the absolute valuation error in RIV(TVC) [on average] is smaller than the absolute error provided in the book value of owners’ equity. To test hypothesis 1 the difference between the absolute valuation error in RIV(TVC) and book value of owners’ equity is calculated for each observation: DiffRIV(TVC)-Bv = Abs(V.E.)RIV(TVC) - Abs(V.E.)Bv (DiffRIV(TVC)-Bv) The mean difference is tested with a paired t-test where significant negative (positive) mean values would imply that the absolute valuation error in RIV(TVC) [on average] is smaller (greater) than in book value of owners’ equity: 0.90 1 0.80 0.8 0.70 0.6 0.60 Diff 0.40 0.2 2007-05-14 2006-05-19 2005-05-24 2004-05-29 2003-06-04 2002-06-09 2001-06-14 2000-06-19 1998-06-30 Materials Information Technology Abs(V.E.(BV)) Telecommunication Services Abs(V.E.(RIV(TVC))) Industrials -0.6 Health Care -0.4 0.00 Financials 0.10 Energy -0.2 Consumer Staples 0.20 1999-06-25 0 0.30 Consumer Discretionary V.E. 0.4 0.50 Abs(V.E.(RIV(TVC)))-Abs(V.E.(BV)) Chart 15: Comparison of the absolute average valuation error in RIV(TVC) and BV per sector. Chart 16: The difference between the absolute valuation errors in the models, calculated for each observation. Number of H0: RIV(TVC)-BV = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0806*** -24.1501 0.0000 0.0000 1.0000 1343 Consumer Staples -0.1559*** -48.1293 0.0000 0.0000 1.0000 326 Energy -0.0271** -2.3290 0.0109 0.0217 0.9891 109 Financials -0.0640*** -28.3670 0.0000 0.0000 1.0000 1190 Health Care -0.0955*** -35.9340 0.0000 0.0000 1.0000 471 Industrials -0.0984*** -55.9340 0.0000 0.0000 1.0000 2947 Information Technology -0.0587*** -24.8607 0.0000 0.0000 1.0000 1289 Materials -0.0787*** -19.0168 0.0000 0.0000 1.0000 625 Telecommunication Services -0.0376*** -9.8045 0.0000 0.0000 1.0000 204 Table 22: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(TVC)-BV = 0 Observations Mean t p (<0) p (≠0) p(>0) Total -0.0830*** -79.1652 0.0000 0.0000 1.0000 8504 Table 23: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Testing of hypothesis 1 show that the mean absolute valuation error in RIV(TVC) is smaller than in book value. The largest absolute differences can be observed in Consumer Staples and 37 Health Care. For Energy and Telecommunication, the mean absolute differences are found to be the smallest. All results are significant at the 1 percent level, except for Energy companies where the difference is significantly less than zero at the 5 percent level. Over time, the volatility in DiffRIV(TVC)-Bv has decreased and the differences in the sample have converged. The RIV(TVC) model [on average] provides a smaller absolute Result 1: valuation error than book value of owners’ equity for 9 out of 9 industry sectors. 5.9. Testing of Hypothesis 2 and Sub-Hypothesis Hypothesis 2 suggests that the absolute valuation error in RIV(PMB) [on average] is smaller than the absolute error provided in RIV(TVC). To test hypothesis 2 the difference between the absolute valuation error in RIV(PMB) and RIV(TVC) is calculated for each observation: DiffRIV(PMB)-RIV(TVC) = Abs(V.E.)RIV(PMB) - Abs(V.E.)RIV(TVC) (DiffRIV(PMB)RIV(TVC)) The mean difference is subsequently tested with a paired t-test where significant negative (positive) mean values would imply that the absolute valuation error in RIV(PMB) [on average] is 3 0.70 2.5 0.60 2 0.50 1.5 Diff 0.80 0.40 1 0.30 0.5 0.20 0 0.10 -0.5 2007-05-14 2006-05-19 2005-05-24 2004-05-29 2003-06-04 2002-06-09 2001-06-14 2000-06-19 1999-06-25 1998-06-30 Materials Information Technology Abs(V.E.(RIV(TVC))) -1 Telecommunication Services Abs(V.E.(RIV(PMB))) Industrials Health Care Financials Energy Consumer Staples 0.00 Consumer Discretionary V.E. smaller (greater) than in RIV(TVC): Abs(V.E.(RIV(PMB)))-Abs(V.E.(RIV(TVC))) Chart 17: Comparison of the absolute average valuation error in RIV(PMB) and RIV(TVC) per sector. 38 Chart 18: The difference between the absolute valuation errors in the models, calculated for each observation. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0161* -1.5582 0.0597 0.1194 0.9403 1343 Consumer Staples -0.2311*** -41.0754 0.0000 0.0000 1.0000 326 Energy 0.2339*** 3.8472 0.9999 0.0002 0.0001 109 Financials -0.1286*** -15.7197 0.0000 0.0000 1.0000 1190 Health Care -0.2830*** -15.7283 0.0000 0.0000 1.0000 471 Industrials -0.0790*** -26.4430 0.0000 0.0000 1.0000 2947 Information Technology -0.0730*** -8.0700 0.0000 0.0000 1.0000 1289 Materials 0.0368*** 3.3154 0.9995 0.0010 0.0005 625 Telecommunication Services -0.0181 -0.9548 0.1704 0.3408 0.8296 204 Table 24: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total -0.0782*** -24.5064 0.0000 0.0000 1.0000 8504 Table 25: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Testing of hypothesis 2 shows that the mean absolute valuation error in RIV(PMB) is smaller than in RIV(TVC) for all sectors except Materials and Energy. The largest absolute differences can be observed in Health Care and Energy and the smallest absolute difference is found in Consumer Discretionary and Telecommunication Services. The results for Telecommunication Services are not significant at the 10 percent level. The remaining sectors have significant results at the 1 percent or 10 percent (Consumer Discretionary) level. Over time, the volatility in the differences has decreased. The RIV(PMB) model [on average] provides a smaller absolute Result 2: valuation error than RIV(TVC) for 5 out of 9 industry sectors. RIV(TVC) [on average] provides a smaller absolute valuation error than RIV(PMB) for 2 out of 9 industry sectors. In RIV(Q) the RIV(TVC) model is extended using PMB values estimated for the sample over the whole period (Q). To test the sub-hypothesis that RIV(Q) [on average] provides a smaller valuation error than RIV(PMB), the difference between the absolute valuation error in RIV(Q) and RIV(PMB) is calculated for each observation: DiffRIV(Q)-RIV(PMB) = Abs(V.E.)RIV(Q) - Abs(V.E.)RIV(PMB) (DiffRIV(Q)RIV(PMB)) The mean difference is tested with a paired t-test where significant negative (positive) mean values would imply that the absolute valuation error in RIV(Q) [on average] is smaller (greater) than in RIV(PMB): 39 14 1.20 12 1.00 10 0.80 Diff 6 4 0.40 2 0.20 0 2007-05-14 Chart 20: The difference between the absolute valuation errors in the models, calculated for each observation. H0: RIV(Q )-RIV(PMB) = 0 t p (<0) p (≠0) 19.0887 1.0000 0.0000 4.4038 1.0000 0.0000 -6.7938 0.0000 0.0000 15.8932 1.0000 0.0000 4.0221 1.0000 0.0001 10.1091 1.0000 0.0000 15.4071 1.0000 0.0000 12.8344 1.0000 0.0000 11.0948 1.0000 0.0000 Significant at the 1 percent level, ** Number of Observations p(>0) 0.0000 1343 0.0000 326 1.0000 109 0.0000 1190 0.0000 471 0.0000 2947 0.0000 1289 0.0000 625 0.0000 204 Significant at the 5 percent Number of H0: RIV(Q )-RIV(PMB) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.2206*** 27.9585 1.0000 0.0000 0.0000 8504 Table 27: Paired t-test of DiffRIV(Q)-RIV(PMB). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Testing of the sub-hypothesis to hypothesis 2 shows that the mean absolute valuation error in RIV(Q) is smaller than in RIV(PMB) only for Energy companies. For all other industry sectors, the RIV(PMB) model provides the smallest average absolute valuation error. All results are significant at the 1 percent level. The largest absolute differences can be observed in Information Technology, Consumer Discretionary and Telecommunication Services. The smallest absolute difference is found in Materials and Health Care. Over time, the volatility in the difference has been relatively constant with more extreme values concentrated around year 2000-2001. With exception for Energy, the results contradict the sub-hypothesis for all sectors: Sub-Result: 2006-05-19 2005-05-24 2004-05-29 2003-06-04 2002-06-09 2001-06-14 2000-06-19 Abs(V.E.(RIV(Q)))-Abs(V.E.(RIV(PMB))) Chart 19: Comparison of the absolute average valuation error in RIV(Q) and RIV(PMB) per sector. GICS Sector Mean Consumer Discretionary 0.4596*** Consumer Staples 0.1157*** Energy -0.1241*** Financials 0.1114*** Health Care 0.0749*** Industrials 0.1025*** Information Technology 0.5321*** Materials 0.0080*** Telecommunication Services 0.3603*** Table 26: Paired t-test of DiffRIV(Q)-RIV(PMB). *** level, * Significant at the 10 percent level. 1999-06-25 1998-06-30 Materials Information Technology Abs(V.E.(RIV(PMB))) -2 Telecommunication Services Abs(V.E.(RIV(Q))) Industrials Health Care Financials Energy Consumer Staples 0.00 Consumer Discretionary V.E. 8 0.60 The RIV(Q) model [on average] provides a smaller absolute valuation error than RIV(PMB) for 1 out of 9 industry sectors. RIV(PMB) [on average] provides a smaller absolute valuation error than RIV(Q) for 8 out of 9 industry sectors. 40 5.10. Testing of Hypothesis 3 Hypothesis 3 suggests that the absolute valuation error in PVEE(rf) [on average] is smaller than the absolute error provided in PVEE(rE). To test hypothesis 3 the difference between the absolute valuation error in PVEE(rf) and PVEE(rE) is calculated for each observation: DiffPVEE(rf)-PVEE(rE) = Abs(V.E.)PVEE(rf) - Abs(V.E.)PVEE(rE) (DiffPVEE(rf)PVEE(rE)) The mean difference is tested with a paired t-test where significant negative (positive) mean values would imply that the absolute valuation error in PVEE(rf) [on average] is smaller (greater) than in PVEE(rE): 1.40 9 8 1.20 7 6 1.00 5 0.80 Diff V.E. 4 0.60 3 2 0.40 1 0 0.20 -1 2007-05-14 2006-05-19 2005-05-24 2004-05-29 2003-06-04 2002-06-09 2001-06-14 2000-06-19 1999-06-25 1998-06-30 Materials Information Technology Abs(V.E.(PVEE(rE))) -2 Telecommunication Services Abs(V.E.(PVEE(rf))) Industrials Health Care Financials Energy Consumer Staples Consumer Discretionary 0.00 Abs(V.E.(PVEE(rf)))-Abs(V.E.(PVEE(rE))) Chart 21: Comparison of the absolute average valuation error in PVEE(rf) and PVEE(rE) per sector. Chart 22: The difference between the absolute valuation errors in the models, calculated for each observation. H0: PVEE(rf)-PVEE(rE) = 0 GICS Sector Mean t p (<0) p (≠0) Consumer Discretionary 0.4836*** 25.5524 1.0000 0.0000 Consumer Staples 0.3254*** 23.7195 1.0000 0.0000 Energy 0.7508*** 7.8110 1.0000 0.0000 Financials 0.4765*** 29.6847 1.0000 0.0000 Health Care -0.0410** -2.2602 0.0121 0.0243 Industrials 0.4929*** 47.5434 1.0000 0.0000 Information Technology 0.1781*** 7.5452 1.0000 0.0000 Materials 0.7031*** 30.1305 1.0000 0.0000 Telecommunication Services 0.2083*** 5.1504 1.0000 0.0000 Table 28: Paired t-test of DiffPVEE(rE)-PVEE(rf). *** Significant at the 1 percent level, ** level, * Significant at the 10 percent level. Number of Observations p(>0) 0.0000 1343 0.0000 326 0.0000 109 0.0000 1190 0.9879 471 0.0000 2947 0.0000 1289 0.0000 625 0.0000 204 Significant at the 5 percent Number of H0: PVEE(rf)-PVEE(rE) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.4174*** 58.9518 1.0000 0.0000 0.0000 8504 Table 29: Paired t-test of DiffPVEE(rE)-PVEE(rf). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. 41 Testing of hypothesis 3 shows that the mean absolute valuation error in PVEE(rf) is smaller than in PVEE(rE) only for Health Care companies. This is significant at the 5 percent level. For all other industry sectors, the PVEE(rE) model provides the smallest average absolute valuation error, and the results are significant at the 1 percent level. The largest absolute differences can be observed in Energy, Materials and Industrials. The smallest absolute difference is found in Health Care, Information Technology and Telecommunication Services. Over time, the volatility in the difference has been relatively constant with more extreme values concentrated around year 20002001. With exception for Health Care, the results contradict hypothesis 3 for all sectors The PVEE(rf) model [on average] provides a smaller absolute Result 3: valuation error than PVEE(rE) for 1 out of 9 industry sectors. PVEE(rE) [on average] provides a smaller absolute valuation error than PVEE(rf) for 8 out of 9 industry sectors. 5.11. Testing of Hypothesis 4 Hypothesis 4 suggests that the absolute valuation error in AEG(TVC) [on average] is smaller than the absolute error provided in PVEE(rE). To test hypothesis 4 the difference between the absolute valuation error in AEG(TVC) and PVEE(rE) is calculated for each observation: DiffAEG(TVC)-PVEE(rE) = Abs(V.E.)AEG(TVC) - Abs(V.E.)PVEE(rE) (DiffAEG(TVC)PVEE(rE)) The mean difference is tested with a paired t-test where significant negative (positive) mean values would imply that the absolute valuation error in AEG(TVC) [on average] is smaller (greater) than in PVEE(rE): 42 0.80 5 0.70 4 3 0.60 2 1 Diff 0.40 0 0.30 -1 0.20 -2 0.10 -3 2007-05-14 Abs(V.E.(AEG(TVC)))-Abs(V.E.(PVEE(rE)) Chart 23: Comparison of the absolute average valuation error in AEG(TVC) and PVEE(rE) per sector. Chart 24: The difference between the absolute valuation errors in the models, calculated for each observation. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.0181*** 2.3763 0.9912 0.0176 0.0088 1343 Consumer Staples 0.1343*** 10.8061 1.0000 0.0000 0.0000 326 Energy -0.0880 -1.0560 0.1467 0.2933 0.8533 109 Financials -0.0076** -1.7952 0.0364 0.0729 0.9636 1190 Health Care -0.1419*** -12.2921 0.0000 0.0000 1.0000 471 Industrials 0.0090** 1.8258 0.9660 0.0680 0.0340 2947 Information Technology -0.0933*** -9.5589 0.0000 0.0000 1.0000 1289 Materials -0.0800*** -4.8402 0.0000 0.0000 1.0000 625 Telecommunication Services -0.1397*** -9.0181 0.0000 0.0000 1.0000 204 Table 30: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total -0.0223*** -6.7949 0.0000 0.0000 1.0000 8504 Table 31: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Testing of hypothesis 4 shows that the mean absolute valuation error in AEG(TVC) is smaller than in PVEE(rE) for all sectors with exception for Consumer Discretionary, Consumer Staples and Industrials. The results are not significant at the 10 percent level for Energy. The largest absolute differences can be observed in Health Care, Telecommunication Services and Consumer Staples. The smallest absolute difference is found in Financials, Industrials and Consumer Discretionary. Over time, the volatility in the difference has been relatively constant. Result 4: 2006-05-19 2005-05-24 2004-05-29 2003-06-04 2002-06-09 2001-06-14 2000-06-19 1999-06-25 1998-06-30 Materials Information Technology Abs(V.E.(PVEE(rE))) -4 Telecommunication Services Abs(V.E.(AEG(TVC))) Industrials Health Care Financials Energy Consumer Staples 0.00 Consumer Discretionary V.E. 0.50 The AEG(TVC) model [on average] provides a smaller absolute valuation error than PVEE(rE) for 5 out of 9 industry sectors. PVEE(rE) [on average] provides a smaller absolute valuation error than AEG(TVC) for 3 out of 9 industry sectors. 43 5.12. Testing of Hypothesis 5 Hypothesis 5 suggests that the absolute valuation error in AEG(TVC) [on average] is smaller than the absolute error provided in RIV(TVC). To test hypothesis 5 the difference between the absolute valuation error in AEG(TVC) and RIV(TVC) is calculated for each observation: DiffAEG(TVC)-RIV(TVC) = Abs(V.E.)AEG(TVC) - Abs(V.E.)RIV(TVC) (DiffAEG(TVC)RIV(TVC)) The mean difference is tested with a paired t-test where significant negative (positive) mean values would imply that the absolute valuation error in AEG(TVC) [on average] is smaller (greater) than in RIV(TVC): 0.80 6 0.70 5 4 0.60 3 2 Diff 0.40 1 0.30 0 0.20 -1 0.10 -2 2007-05-14 2006-05-19 2005-05-24 2004-05-29 2003-06-04 2002-06-09 2001-06-14 2000-06-19 1999-06-25 1998-06-30 Materials Information Technology Abs(V.E.(RIV(TVC))) -3 Telecommunication Services Abs(V.E.(AEG(TVC))) Industrials Health Care Financials Energy Consumer Staples 0.00 Consumer Discretionary V.E. 0.50 Abs(V.E.(AEG(TVC)))-Abs(V.E.(RIV(TVC))) Chart 25: Comparison of the absolute average valuation error in AEG(TVC) and RIV(TVC) per sector. Chart 26: The difference between the absolute valuation errors in the models, calculated for each observation. Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0964*** -5.9113 0.0000 0.0000 1.0000 1343 Consumer Staples -0.1494*** -6.2728 0.0000 0.0000 1.0000 326 Energy 0.1676*** 3.2558 0.9992 0.0015 0.0008 109 Financials -0.1600*** -19.9913 0.0000 0.0000 1.0000 1190 Health Care -0.3978*** -27.0365 0.0000 0.0000 1.0000 471 Industrials -0.1449*** -15.2183 0.0000 0.0000 1.0000 2947 Information Technology -0.1748*** -19.9894 0.0000 0.0000 1.0000 1289 Materials 0.1195*** 5.2066 1.0000 0.0000 0.0000 625 Telecommunication Services -0.1355*** -7.7032 0.0000 0.0000 1.0000 204 Table 32: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total -0.1344*** -26.0213 0.0000 0.0000 1.0000 8504 Table 33: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. 44 Testing of hypothesis 5 shows that the mean absolute valuation error in AEG(TVC) is smaller than in RIV(TVC) for all sectors with exception for Energy and Materials. All results are significant at the 1 percent level. The largest absolute differences can be observed in Health Care, Information Technology and Energy. The smallest absolute difference is found in Consumer Discretionary, Materials and Telecommunication Services. Over time, the volatility in the difference has converged from initially high levels during the years 1999-2001. Result 5: The AEG(TVC) model [on average] provides a smaller absolute valuation error than RIV(TVC) for 7 out of 9 industry sectors. RIV(TVC) [on average] provides a smaller absolute valuation error than AEG(TVC) for 2 out of 9 industry sectors. 45 5.13. Summary of Empirical Results and Statistical Testing 4.00 3.20 2.40 V.E. 1.60 0.80 0.00 RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 27: Average valuation error for each GICS industry sector and model over the whole period (1998-2007). 46 Materials Information Technology Telecommunication Services BV Industrials Health Care Financials Energy Consumer Staples -1.60 Consumer Discretionary -0.80 4.00 3.20 V.E. 2.40 1.60 RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 28: Average absolute valuation error for each GICS industry sector and model over the whole period (1998-2007). 47 Materials Information Technology Telecommunication Services BV Industrials Health Care Financials Energy Consumer Staples 0.00 Consumer Discretionary 0.80 0.80 0.60 0.40 V.E. 0.20 0.00 -0.20 -0.40 -0.60 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 29: Average valuation error for each model over the whole period (1998-2007). 0.90 0.80 0.70 0.60 V.E. 0.50 0.40 0.30 0.20 0.10 0.00 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 30: Average absolute valuation error for each model over the whole period (1998-2007). 48 The empirical modelling in this section implies that: Average Valuation error Average Absolute Valuation error Valuation Model Book Value Over/underestimation Underestimates for all sectors. Largest Error Consumer Staples (-), Health Care (-) Smallest Error Energy (-), Materials (-) Largest Error Health Care, Consumer Staples Smallest Error Materials, Energy RIV(TVC) Underestimates for all sectors. Health Care (-), Consumer Staples (-) Energy (-), Materials (-) Health Care, Information Technology Materials, Financials RIV(PMB) Underestimates for 7/9 sectors. Energy (+), Consumer Staples (-) Financials (-), Telecommunication Services (-) Energy, Consumer Discretionary Financials, Materials RIV(Q) Overestimates for all sectors. Information Technology (+), Consumer Discretionary (+) Materials (+), Financials (+) Information Technology, Consumer Discretionary Materials, Financials PVEE(rE) Underestimates for 5/9 sectors. Information Technology (-), Telecommunication Services (-) Consumer Discretionary (+), Industrials (-) Energy, Information Technology Financials, Consumer Staples PVEE(rf) Overestimates for all sectors. Energy (+), Materials (+) Health Care (+), Telecommunication Services (+) Energy, Materials Health Care, Consumer Staples AEG(TVC) Overestimates for 5/9 sectors. Consumer Staples (+), Materials (+) Financials (-), Health Care (-) Energy, Financials, Consumer Telecommunication Discretionary Services Table 34: Overview of results from empirical modelling. (+) Positive average valuation error, (-) Negative average valuation error. Summarised results from the statistical testing of hypotheses: H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 GICS Sector Consumer Discretionary *** * (***) (***) (***) *** Consumer Staples *** *** (***) (***) *** *** Energy ** (***) *** (***) (***) Financials *** *** (***) (***) ** *** Health Care *** *** (***) ** *** *** Industrials *** *** (***) (***) (**) *** Information Technology *** *** (***) (***) *** *** Materials *** (***) (***) (***) *** (***) Telecommunication Services *** (***) (***) *** *** Table 35: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 Total *** *** (***) (***) *** *** Table 36: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. In the next section, the results will be discussed and critically evaluated. 49 6. Discussion of Empirical Results and Concluding Comments 6.1. Discussion of Empirical Results Empirical testing of benchmark equity valuation models has been performed for seven different valuation models on a data sample of 190 Swedish companies between 1998 and 2007 (Table 1-3). The models have differing approaches to obtain the fair value of owners’ equity, but could [with some reservation for book value of owners’ equity] all be derived from the theory that the value of a company’s equity capital equals the present value of expected future dividends. The calculated differences between the fair (market) value of owners’ equity and the estimated value in each model is referred to as the valuation error. In the empirical analysis, the valuation error is assumed to be attributable to conservative accounting principles and the business goodwill/badwill at t=T and the models’ failure to withstand these biases (cf. the definition of valuation error in section 5.1.). The results show that the models’ ability to reflect the market value of owners’ equity varies between industry sectors and over time. Book value of owners’ equity constantly underestimates the market value of owners’ equity for all sectors and over time, i.e. the valuation bias in book value of owners’ equity is non-positive for all sectors. These implications fits well with the theoretical reasoning that the biased book value at t=0 fails to capture the value of for example future earnings and that the market value of owners’ equity should equal book value with a premium. Inferences about different levels of conservative bias and business goodwill/badwill among the industry sectors could consequently be made from the results. Materials and Energy sectors seem to be the sectors with the lowest level of valuation bias. The Materials and Energy sectors comprise companies that manufacture materials, paper, forest products and related products along with companies constructing or providing oil rigs, drilling equipment and other energy related services and equipment. These companies could be expected to have capital intensive business models with relatively large proportions of the assets marked to market on the balance sheet. On the opposite side, Health Care, Consumer Staples and Information Technology show the highest levels of conservative accounting. These industry sectors could also be expected to have a relatively higher amount of hidden assets that are not recorded on the balance sheet. The industries encompass companies that are engaged in research, development and production of pharmaceuticals, development of software application or provision of technology consulting services as well as manufacturers and distributors of food and beverages. Examples of hidden assets on the companies’ balance sheets could be operating assets that are recorded according to the principal of prudency and thus lead to underestimation of the fair value of owners’ equity. 50 The RIV(TVC) model anchors the value of owners’ equity to book value, and links future residual income to the value of equity capital to arrive at the estimated intrinsic value. RIV(TVC) on average provides estimation below the market value for all sectors. In comparison with the results for book value of owners’ equity the RIV(TVC) model on average results in smaller absolute valuation errors for each sector and over time. Consequently, the anchoring of residual income to the book value of owners’ equity seems to withstand valuation biases to a greater extent than book value alone. The differences in valuation error across industry sectors are comparable with the results discussed for book value of owners’ equity. Hypothesis 1: The RIV(TVC) model [on average] provides a smaller absolute valuation error than the book value of owners’ equity. Result 1: The RIV(TVC) model [on average] provides a smaller absolute valuation error than book value of owners’ equity for 9 out of 9 industry sectors. Testing hypothesis 1 shows that the extension of book value in RIV(TVC) with future residual income on average arrives at a more accurate estimation of the fair value of owners’ equity for companies in all industry sectors. This implies that RIV(TVC) is a more robust model with a greater ability to withstand valuation bias than book value of owners’ equity (cf. the reasoning in section 3.4.). The valuation error in RIV(TVC) is a function of the business goodwill/badwill at the chosen horizon point of time. To adjust for the average underestimation of the fair value in the model, an extension of RIV(TVC) that aims to approximate the level of business goodwill/badwill at T could be made. The extension is referred to as RIV(PMB) and uses an estimated value per sector (the PMB value) to adjust for the conservative bias. Applying the PMB values from Runsten (1998) (Table 5) in an extension of the RIV(TVC) model results in a varying degree of adjustment in valuation errors. The extended residual income valuation does not underestimate the value for all sectors; for Energy and Materials companies RIV(PMB) provide a positive valuation error on average, i.e. the model overestimates the value of owners’ equity. For all other sectors, however, RIV(PMB) shows lower absolute levels of valuation error and the extension seem to have provided a better estimate of the fair value. Hypothesis 2: The RIV(PMB) model [on average] provides a smaller absolute valuation error than the RIV(TVC) model. Result 2: The RIV(PMB) model [on average] provides a smaller absolute valuation error than RIV(TVC) for 5 out of 9 industry sectors. 51 RIV(TVC) [on average] provides a smaller absolute valuation error than RIV(PMB) for 2 out of 9 industry sectors. Testing hypothesis 2 shows that the extension of RIV(TVC) provides better estimates than RIV(TVC) for 5 out of 9 sectors, with exception for Materials and Energy. The two sectors exhibited the lowest absolute (negative) levels of valuation error in RIV(TVC) modelling, and thus it could be concluded that the applied PMB values from Runsten (1998) was a poor estimate which overestimated the level of business goodwill at T for these sectors. The positive error in the estimated level of business goodwill could possibly be explained by the different sector categorisation used by Runsten (1998). Runsten (1998) also concludes that the factors that influence the level of measurement bias varies over time and per company and thus the PMB values should ideally be calculated per company and year rather than subjectively taken from a static table. By reverse-engineering the residual value in the RIV(TVC) estimation, an estimate of the q value that potentially would capture the valuation bias from a company that has not reached steady state has been computed for each observation. To avoid “data mining” and explicit fitting of parameters to the historical data sample, however, the estimated values (Q), have not been computed on a yearly basis but as an average over the whole period. The extension of the RIV(TVC) with the Q values results in a consequent overestimation of the market value for all sectors. The results imply a weaker ability in RIV(Q) compared to RIV(PMB) to capture valuation biases. The results also indicate that the level of business goodwill/badwill at T varies considerably over time in the sample. Sub-Hypothesis: The RIV(Q) model [on average] provides a smaller valuation error than RIV(PMB). Sub-Result: The RIV(Q) model [on average] provides a smaller absolute valuation error than RIV(PMB) for 1 out of 9 industry sectors. RIV(PMB) [on average] provides a smaller absolute valuation error than RIV(Q) for 8 out of 9 industry sectors. Testing the sub-hypothesis that the average estimations of Q values would more accurately adjust the RIV(TVC) model than the adjustment of conservative bias with PMB values, shows that this holds only for Energy companies. The poorly applied PMB value from Runsten (1998) for this sector is more accurately estimated by an average Q value over the whole period (cf. the comparison between PMB and Q in Table 10). The estimated Q values in general, however, seem to be influenced by very high levels of business goodwill during some years in the beginning of the period, and the effect from these extreme values could explain the poor adjustment of RIV(TVC) and that the estimated values do not result in smaller valuation errors than in 52 RIV(PMB). The rejection of the sub-hypothesis for 8 out of 9 sectors harmonizes with the comments in Runsten (1998) about varying levels of factors influencing the level of goodwill at T over time as well as the difficulties in estimating the PMB values. Estimating a company’s equity capital from an earnings-based valuation approach is most easily achieved by capitalising the next year’s expected earnings with the company required rate of return on equity. This model is referred to as the present value of expected earnings (PVEE(rE)), and the valuation error from conservative accounting in PVEE(rE) equals the difference between capitalised next year’s earnings and capitalised next year’s unbiased earnings. The results for PVEE(rE), show varying levels of both under- and overestimation of the fair value of owners’ equity. The average absolute valuation error is the smallest for Financials, Consumer Staples and Industrials companies. These industry sectors could consequently be anticipated to encompass companies with relatively low levels of conservative bias in next year’s earnings. The results also show that PVEE(rE) on average underestimates the fair value the most for Information Technology, Telecommunication Services and Health Care Companies. Underlying assumptions (cf. the assumption that all earnings are paid out as dividends in section 3.6.) in the PVEE(rE) model make it difficult to attribute the valuation error in the model only to different levels of conservative accounting principles. The industries, for which PVEE(rE) on average underestimates the fair value the most, have all shown higher-than-steady-state levels of growth over the period. Releasing the assumption that T=1=T* (i.e. that the company has entered steady state and that the growth equals zero) could possibly add to the explanation that the calculated valuation errors to some extent reflect the model’s failure to include future growth in its valuation of owners’ equity. In Materials and Energy companies, on the other hand, owners’ equity is on average overestimated by PVEE(rE); the implications of this (that next year’s earnings are heavily biased by conservative accounting) could interestingly be compared with the results from the empirical testing of the asset-based book value approach (where the same sectors in contrast showed the smallest average absolute valuation error). In section 3.6, the reasoning that the unconsidered effect of growth in earnings in PVEE(rE) could possibly be adjusted for by replacing the denominator with the risk-free interest rate is presented. The estimation rests on the assumption that the growth rate equals the risk adjusted market risk premium, and would result in a more accurate estimation than PVEE(rE) for any company or sector where this holds or where the growth rate is greater than the difference between rE and rf: Hypothesis 3: The Capitalised Earnings Model where earnings are capitalised with the risk-free interest rate [on average] provides a smaller valuation error than earnings capitalised with the required rate of return on equity. 53 The PVEE(rf) model [on average] provides a smaller absolute Result 3: valuation error than PVEE(rE) for 1 out of 9 industry sectors. PVEE(rE) [on average] provides a smaller absolute valuation error than PVEE(rf) for 8 out of 9 industry sectors. Empirical testing shows that the results from PVEE(rf) on average provide an overestimation of the value of owners’ equity for all sectors. The smallest overestimation and average absolute valuation error is provided for Health Care companies, and this is also the only sector for which PVEE(rf) provides a more accurate estimate of the value of owners’ equity on average over time. The assumption of no growth in the nominator for PVEE is a strong assumption that evidently seems to result in underestimated values of owners’ equity. Adjusting the denominator under the assumption that the growth rate would equal the difference between the risk-free interest rate and the required rate of return on equity, however, does not seem to be an appropriate adjustment for all sectors26. The AEG(TVC) model anchors future abnormal earnings to capitalised earnings to arrive at an estimation of the value of owners’ equity. AEG(TVC), on average provides the largest estimations below the market value for Information Technology, Telecommunication Services and Health Care companies. The valuation error in AEG(TVC) is a function of the growth in expected level of conservative bias as T+1. Consequently, the growth in conservative bias for companies in the three sectors could be anticipated to be high at T+1. 26 Suggesting an alternative approach could be to replace the assumption of no growth with an assumption that the company growth rate in earnings equals the expected level of inflation (i.e. the company real growth rate is zero) that is included in the nominal risk-free interest rate at t=0: The relationship between inflation (i), real (r) and nominal (R) interest rates can be described (1 + r)(1 + i) = (1 + R). In this alternative approach, the next year’s earnings would consequently be capitalised using the required rate of return on equity less the expected inflation rate (rE – i). Provided an expected inflation greater than zero at t=0, this approach would result in a valuation somewhere between PVEE(rE) and PVEE(rf). Further research to empirically evaluate the reasoning presented in this alternative approach is suggested by the authors. The impact of adopting the revised discount rate (rE – i) in the parsimonious terminal value constrained version of the Abnormal Earnings Growth valuation model could possibly also be researched. 54 Hypothesis 4: The AEG(TVC) model [on average] provides a smaller absolute valuation error than PVEE(rE). Result 4: The AEG(TVC) model [on average] provides a smaller absolute valuation error than PVEE(rE) for 5 out of 9 industry sectors. PVEE(rE) [on average] provides a smaller absolute valuation error than AEG(TVC) for 3 out of 9 industry sectors. The testing of hypothesis 4 indicates that the AEG(TVC) provides better estimates than the PVEE(rE) of the fair value of owners’ equity with exception for Consumer Discretionary and Industrials. These sectors would consequently include companies with relatively low growth levels in conservatively biased future earnings. Consumer Discretionary and Industrials include companies that manufacture automotive, household durable goods and capital goods including aerospace and defence (Table 24). The results from testing hypothesis 4 suggest that AEG(TVC) on average decreases the absolute valuation error for 5 out of 9 sectors. In line with the reasoning above about anticipated levels of conservative accounting in the Health Care sector, and the discussion of permanent measurement biases in Runsten (1998), the relatively large adjustment for Health Care companies seems reasonable. Over the studied time period, the estimated Q values for the Health Care sector have steadily increased (Table 9). This historical growth in business goodwill at T could imply that the level of conservative accounting in the sector has increased. AEG(TVC) focuses on earnings and earnings growth in the short and in the long run, and thus the model could therefore be expected to provide a smaller valuation error than PVEE(rE) for the Health Care sector (cf. the underestimation of fair value of owners’ equity in PVEE(rE) for Health Care companies). Skogsvik and Juettner-Nauroth (2007) suggest that the valuation error in the terminal value constrained AEG model is typically smaller than in the corresponding RIV model if the growth of the conservative bias lies within a certain interval of “normal” values. Hypothesis 5: The AEG(TVC) model [on average] provides a smaller absolute valuation error than RIV(TVC). Result 5: The AEG(TVC) model [on average] provides a smaller absolute valuation error than RIV(TVC) for 7 out of 9 industry sectors. RIV(TVC) [on average] provides a smaller absolute valuation error than AEG(TVC) for 2 out of 9 industry sectors. The testing of hypothesis 5 shows that the AEG(TVC) model provides a smaller absolute valuation error than the RIV(TVC) model for all sectors with exception for Energy and Materials. 55 As earlier touched upon, the Energy and Materials sectors encompass companies with relatively low levels of expected exposure to conservative accounting principles. The empirical testing shows that the largest absolute differences can be observed for Health Care and Information Technology. Companies within these sectors generally possess characteristics of high Q values and could consequently be expected to have a relatively higher exposure to conservative accounting principles. Comparing the average valuation errors show different levels of bias in the results (i.e. an average valuation error close to zero). A relatively unbiased result such as the PVEE(rE) valuation for Consumer Discretionary companies (1.09 percent) could be useful in the context of portfolio valuation. Comparing the total results aggregated over all industry sectors, shows that PVEE(rE) and AEG(TVC) provide the smallest biases and average absolute valuation errors together with RIV(PMB). Evaluating the aggregated results in an attempt to rank the models would, however, imply a naïve approach to equity valuation modelling. 6.2. The Validity and Robustness of the Empirical Results The empirical results should generally be robust to different data sources or sample selection conditions. Strong assumptions and limited consistency of the data, however, motivates a discussion of the validity and robustness of the results: It should be noted that evaluation of equity valuation models revolve on a harsh treatment of accounting numbers, e.g. the assumption that CSR holds is necessary in the valuation modelling. This relation, however, could not be expected to hold in practice. The short horizon point of time, where the truncation of the parsimonious valuation models occur (FY3) could be expected to appear at a stage where T<T*, and thus the assumption of steady state could also be expected to be violated. The impact of the short horizon point of time on the valuation models is summarised in conjunction with the estimation of Q values (cf. Table 10 and the associated discussion). Cyclical market effects that appear over the time period could potentially lead to biased results. To make inferences about the impact over time from periods with relatively extreme conditions, the sample is divided into two sub-samples (1998-2002 and 2003-2007), for which the empirical analysis and statistical testing is performed in a first robustness test: The robustness test of the empirical results for the two time periods shows fairly similar results (cf. Appendix 18-19 for empirical results and statistical testing) to the main results and conclusions about historical fluctuations presented in the previous section. The use of consensus estimates as a proxy for market expectations on the specific companies’ future book value of owners’ equity, earnings and dividends requires accurate analyst forecasts. Preferably, the number of estimates should be high enough to categorically motivate 56 this assumption. To test for the implications of few estimates, a sub-sample is empirically evaluated in a second robustness test: The sub-sample consists of all observations with five or more consensus estimates for each parameter and fiscal period. When limiting he sample by adding restrictions to the sample criteria on the minimum number of consensus estimates, the number of observations decreases to 2 705. GICS Sector 1998 1999 2000 2001 2002 2003 2004 2005 Consumer Discretionary 0 36 49 30 11 36 70 49 Consumer Staples 0 8 13 1 0 7 19 13 Energy 0 0 0 0 0 0 0 0 Financials 0 37 44 42 24 46 61 41 Health Care 0 5 15 2 0 3 15 7 Industrials 0 47 118 89 36 95 156 121 Information Technology 0 7 32 22 2 8 47 23 Materials 0 19 32 28 3 24 52 49 Telecommunication Services 0 5 10 15 1 15 23 20 Total 0 164 313 229 77 234 443 323 Table 37: Total number of complete observation in robustness test sub-sample per industry sector and year. 2006 76 18 0 66 28 168 34 60 23 473 2007 79 13 1 71 28 156 30 52 19 449 Total 436 92 1 432 103 986 205 319 131 2705 The robustness test shows that the results are in line with the results for the whole sample. With fewer degrees of freedom, however, the statistical significance in the results is affected negatively (cf. Table 128-139, where the statistical results for the Energy sector are not significant). The estimated equity risk premium is used to infer the required rate of return on equity and, thus, the assumption will have impacts on [some of] the evaluated models: E( rE ) = rf + β ⋅ [E(rm ) − rf ] (CAPM) gives that [E(rm ) − rf ] ↑⇒ E( rE ) ↑ , i.e. when the equity risk premium increases, this leads to a higher required rate of return on equity and the models that comprise the required rate of return on equity will be affected analogously. The robustness of the results, with regards to the assumption of the equity risk premium, is consequently tested by repeating the empirical analysis with an assumed equity risk premium of 5.0 percent. The results (cf. Appendix) show little deviations from the results obtained with a 4.0 percent risk premium. Hence, the aggregated results could be viewed as robust for the proposed risk premium. This reasoning could be applied to a discussion regarding the impact of poorly estimated beta values; the estimation of industry sector beta values over time shows a more or less volatile pattern (Chart 32) and this volatility could potentially affect the empirical results. The direct link to the required rate of return on equity through CAPM and the 57 equity risk premium provides a possibility to estimate the impact of changes in beta on the results without performing separate robustness tests: β ↑⇒ E( rE ) ↑ . In conclusion, the results can generally [with exception for specific observations] be seen as robust over time. The observed variations in the statistical results, however, recognize the difficulties in finding appropriate rules of thumb to apply on industry sectors and over a long period of time. 58 7. References Dimson E., Marsh P., and Staunton M. (2005), “Global Investment Returns Yearbook 2005”, London, London Business School., pp. 5-75. Modigliani, F., and Miller, M. H. (1958), “The Cost of Capital, Corporation Finance, and the theory of Investment”, American Economic Review, Vol. 48, No. 3, pp. 261-297. Ohlson, J.A. (1995), “Earnings, Book Values and Dividends in Equity Valuation”, Contemporary Accounting Research, Vol. 11. Ohlson, J.A. (2005), “On Accounting-Based Valuation Formulae”, Review of Accounting Studies, Vol. 10, No. 2-3. Ohlson, J.A and Juettner-Nauroth, B. E. (2005), “Expected EPS and EPS Growth as Determinants of Value”, Review of Accounting Studies, Vol. 10. Penman, S.H. (2007), “Financial Statement Analysis and Security Valuation”, McGraw-Hill Irwin, 3rd ed., pp. 119-139, 177-224. Runsten, M. (1998), “The Association between Accounting Information and Stock Prices”, Stockholm: EFI., pp. 41-56, 140-173. Skogsvik, K., and Jennergren, P. (2007), “The Abnormal Earnings Growth Model: Applicability and Applications”, SSE/EFI Working Paper Series in Business Administration No. 2007:11, Stockholm School of Economics. Skogsvik, K., and Juettner-Nauroth, B. E. (2007), “The Impact of Conservative Accounting in Residual Income and Abnormal Earnings Growth Valuation Modelling”. 59 8. Appendix Most of the formulas and derivations in the appendices are summarised from the working paper by Skogsvik and Juettner-Nauroth (2007). Cf. Skogsvik and Juettner-Nauroth (2007) for the full theoretical reasoning and derivations. 8.1. Appendix 1: Derivation of AEG(TVC) from PVED T V0 = ∑ t =1 = E 0 ( X 1 ) E 0 ( Div 1 ) E 0 ( X 1 ) E 0 ( X 2 ) E 0 ( Div 2 ) E 0 ( X 2 ) + − + + − rE RE rE rE ⋅ R E R 2E rE ⋅ R E + ..... + = E 0 ( DIVt ) E o ( PT ) + = RE RT E 0 ( X T ) E 0 ( Div T ) E 0 ( X T ) E 0 ( PT ) + − + = rE ⋅ R ET −1 R TE rE ⋅ R ET −1 R ET E 0 ( X 1 ) T −1 E 0 ( X t +1 + rE ⋅ Div t − X t ⋅ R E ) rE E 0 ( PT + Div T − X T ⋅ R E ) rE +∑ + t =1 rE R tE R ET (Skogsvik and Juettner-Nauroth, 2007) 60 8.2. Appendix 2: GICS Industry Sectors and GICS Level 1 Sector Group Indexes GICS Sector Description GICS Level 1 Sector Group Index Consumer Discretionary The GICS Consumer Discretionary Sector encompasses those industries that tend to be the most sensitive to economic cycles. Its manufacturing segment includes automotive, household durable goods, textiles & apparel and leisure equipment. The services segment includes hotels, restaurants and other leisure facilities, media production and services, and consumer retailing and services. The Stockholmsborsen All-Share Consumer Discretionary Sector Price Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1995. The parent index is SAX. Consumer Staples The GICS Consumer Staples Sector comprises companies whose businesses are less sensitive to economic cycles. It includes manufacturers and distributors of food, beverages and tobacco and producers of nondurable household goods and personal products. It also includes food & drug retailing companies as well as hypermarkets and consumer super centres. The Stockholmsborsen All-Share Consumer Staples Sector Price Index is a capitalizationweighted index. The index was developed with a base value of 100 as of December 31, 1995. The parent index is SAX. Energy The GICS Energy Sector comprises companies whose businesses are dominated by either of the following activities: The construction or provision of oil rigs, drilling equipment and other energy related service and equipment, including seismic data collection. Companies engaged in the exploration, production, marketing, refining and/or transportation of oil and gas products, coal and other consumable fuels. The Stockholmsborsen All-Share Energy Sector Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1995. The parent index is SAX. Financials The GICS Financial Sector contains companies involved in activities such as banking, mortgage finance, consumer finance, specialized finance, investment banking and brokerage, asset management and custody, corporate lending, insurance, and financial investment, and real estate, including REITs. The Stockholmsborsen All-Share Financial Sector Price Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1995. The parent index is SAX. Health Care The GICS Health Care Sector encompasses two main industry groups. The first includes companies who manufacture health care equipment and supplies or provide health care related services, including distributors of health care products, providers of basic health-care services, and owners and operators of health care facilities and organizations. The second regroups companies primarily involved in the research, development, production and marketing of pharmaceuticals and biotechnology products. The Stockholmsborsen All-Share Health Care Sector Price Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1995. The parent index is SAX. Industrials The GICS Industrials Sector includes companies whose businesses are dominated by one of the following activities: The manufacture and distribution of capital goods, including aerospace & defence, construction, engineering & building products, electrical equipment and industrial machinery. The provision of commercial services and supplies, including printing, employment, environmental and office services. The provision of transportation services, including airlines, couriers, marine, road & rail and transportation infrastructure. The Stockholmsborsen All-Share Industrials Sector Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1995. The parent index is SAX. Information Technology The GICS Information Technology Sector covers the following general areas: firstly, Technology Software & Services, including companies that primarily develop software in various fields such as the Internet, applications, systems, databases management and/or home entertainment, and companies that provide information technology consulting and services, as well as data processing and outsourced services; secondly Technology Hardware & Equipment, including manufacturers and distributors of communications equipment, computers & peripherals, electronic equipment and related instruments; and thirdly, Semiconductors & Semiconductor Equipment Manufacturers. The Stockholmsborsen All-Share Materials Sector Price Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1995. The parent index is SAX. Materials The GICS Materials Sector encompasses a wide range of commodity-related manufacturing industries. Included in this sector are companies that manufacture chemicals, construction materials, glass, paper, forest products and related packaging products, and metals, minerals and mining companies, including producers of steel. The Stockholmsborsen All-Share Information Technology Sector Price Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1995. The parent index is SAX. Telecommunicat ion Services The GICS Telecommunications Services Sector contains companies that provide communications services primarily through a fixed-line, cellular, wireless, high bandwidth and/or fibber optic able network. The Stockholmsborsen All-Share Telecommunication Services Sector Price Index is a capitalization-weighted index. The index was developed with a base value of 100 as of December 31, 1995. The parent index is SAX. Table 38: Description of GICS Industry Sectors and corresponding GICS Level 1 Sector Group indexes. Information retrieved from BLOOMBERG. 61 8.3. Appendix 3: Data Sample Company GICS Sector 1998-2007 >=5 Estimates AARHUSKARLSHAMN Consumer Staples 17 0 ABB (OME) Industrials 83 31 ACANDO 'B' Information Technology 63 0 ADDTECH 'B' Industrials 53 0 ALFA LAVAL Industrials 56 47 ANGPANNEFORENINGEN 'B' Industrials 71 0 ANOTO GROUP Information Technology 2 0 ASPIRO Information Technology 4 0 ASSA ABLOY 'B' Industrials 100 63 ATLAS COPCO 'A' Industrials 112 87 AUDIODEV 'B' Information Technology 34 0 AUTOLIV SDB Consumer Discretionary 105 67 AVANZA Financials 16 0 AXFOOD Consumer Staples 91 19 AXIS Information Technology 31 0 B&B TOOLS 'B' Industrials 107 0 BALLINGSLOV INTL. Consumer Discretionary 61 0 BE GROUP Industrials 5 0 BEIJER ALMA 'B' Industrials 35 0 BETSSON 'B' Consumer Discretionary 7 0 BILIA 'A' Consumer Discretionary 84 2 BILLERUD Materials 55 34 BIOVITRUM Health Care 1 0 BJORN BORG Consumer Discretionary 6 0 BOLIDEN Materials 45 28 BONGS LJUNGDAHL 'B' Industrials 53 0 BOSS MEDIA Information Technology 45 0 BRINOVA FASTIGHETER Financials 20 0 BROSTROM Energy 51 1 BTS GROUP Industrials 36 0 BURE EQUITY Financials 19 0 CARDO Industrials 75 27 CARL LAMM Information Technology 9 0 CASHGUARD 'B' Information Technology 6 0 CASTELLUM Financials 67 38 CATENA Financials 1 0 CISION Industrials 65 6 CLAS OHLSON 'B' Consumer Discretionary 77 22 CLOETTA FAZER 'B' Consumer Staples 84 0 CONCORDIA MARITIME 'B' Energy 35 0 CONNECTA Information Technology 19 0 CTT SYSTEMS Industrials 3 0 D CARNEGIE & CO Financials 69 3 DIGITAL VISION Information Technology 1 0 DIOS FASTIGHETER Financials 9 0 DORO Information Technology 22 0 ELANDERS 'B' Consumer Discretionary 63 4 ELECTROLUX 'B' Consumer Discretionary 112 74 ELEKTA 'B' Health Care 89 16 ENEA Information Technology 63 0 ENIRO Consumer Discretionary 81 44 ERICSSON 'B' Information Technology 84 72 EXPANDA 'B' Industrials 15 0 FABEGE Financials 63 12 FAGERHULT Industrials 18 0 FASTIGHETS BALDER 'B' Financials 6 0 FENIX OUTDOOR Consumer Discretionary 28 0 G & L BEIJER Industrials 22 0 GANT COMPANY Consumer Discretionary 9 1 GETINGE Health Care 88 51 GUNNEBO Industrials 62 28 GUNNEBO INDUSTRIER Industrials 17 0 HAKON INVEST AB Consumer Staples 20 0 Table 39: Sample members, assigned GICS industry sector and total number of complete observations. 62 5% Risk Premium 17 83 63 53 56 71 2 4 100 112 34 105 16 91 31 107 61 5 35 7 84 55 1 6 45 53 45 20 51 36 19 75 9 6 67 1 65 77 84 35 19 3 69 1 9 22 63 112 89 62 81 84 15 63 18 3 28 22 9 88 62 17 20 Company GICS Sector 1998-2007 >=5 Estimates 5% Risk Premium HALDEX Industrials 88 48 88 HEBA 'B' Financials 26 0 25 HEMTEX Consumer Discretionary 16 1 16 HENNES & MAURITZ 'B' Consumer Discretionary 112 91 112 HEXAGON 'B' Industrials 79 22 79 HIQ INTERNATIONAL Information Technology 68 27 68 HL DISPLAY 'B' Industrials 60 0 60 HOGANAS 'B' Materials 86 44 86 HOLMEN 'B' Materials 112 68 112 HOME PROPERTIES Financials 55 0 55 HQ Financials 8 0 8 HUFVUDSTADEN 'A' Financials 54 13 54 IBS 'B' Information Technology 71 13 71 INDL.& FINL.SYS.'B' Information Technology 43 13 43 INDUSTRIVARDEN 'A' Financials 11 0 11 INDUTRADE Industrials 20 0 20 INTELLECTA 'B' Industrials 7 0 7 INTRUM JUSTITIA Industrials 56 3 56 INVESTOR 'B' Financials 57 0 57 JEEVES INFO.SYSTEMS Information Technology 9 0 9 JM Consumer Discretionary 84 26 84 KABE HUSVAGNAR 'B' Consumer Discretionary 11 0 11 KAPPAHL HOLDINGS Consumer Discretionary 11 0 11 KAROLIN MACHINE TOOL Industrials 47 0 47 KAUPTHING BANK Financials 8 0 8 KLOVERN Financials 23 0 23 KNOW IT Information Technology 44 0 44 KUNGSLEDEN Financials 53 1 53 LAGERCRANTZ 'B' Information Technology 47 0 47 LATOUR INVESTMENT 'B' Financials 4 0 4 LAWSON SOFTWARE (OME) Information Technology 2 0 2 LINDAB INTERNATIONAL Industrials 9 6 9 LINDEX Consumer Discretionary 99 26 99 LUNDBERGFORETAGEN 'B' Financials 9 0 9 LUNDIN MINING SDB Materials 19 2 19 MALMBERGS ELEKTRISKA Industrials 12 0 12 MEDA 'A' Health Care 48 8 48 MEDIVIR 'B' Health Care 2 0 2 MEKONOMEN Consumer Discretionary 42 0 42 METRO INTL.SDB 'B' Consumer Discretionary 32 0 32 MIDELFART SONESSON 'A' Consumer Staples 1 0 1 MILLICOM INTL.CELU.SDB Telecommunication Services 14 0 14 MOBYSON Information Technology 11 0 11 MODERN TIMES GP.MTG 'B' Consumer Discretionary 79 48 79 MODUL 1 DATA Information Technology 23 0 23 MUNTERS Industrials 86 17 86 NCC 'B' Industrials 74 34 74 NEFAB 'B' Industrials 46 0 46 NEONET Financials 6 0 6 NET INSIGHT 'B' Information Technology 2 0 2 NEW WAVE GROUP 'B' Consumer Discretionary 56 16 56 NIBE INDUSTRIER 'B' Industrials 73 1 73 NOBEL BIOCARE (OME) Health Care 83 7 83 NOBIA Consumer Discretionary 55 14 55 NOCOM 'B' Information Technology 2 0 2 NOKIA (OME) Information Technology 5 5 5 NOLATO 'B' Information Technology 58 9 58 NORDEA BANK Financials 104 90 104 NORDNET SECURITIES BANK Financials 17 0 17 NOTE Information Technology 6 0 6 NOVOTEK 'B' Information Technology 6 0 6 OEM INTERNATIONAL 'B' Industrials 10 0 10 OMX Financials 76 40 76 Table 39 (cont’d): Sample members, assigned GICS industry sector and total number of complete observations. 63 Company GICS Sector 1998-2007 >=5 Estimates 5% Risk Premium ORC SOFTWARE Information Technology 55 17 55 ORIFLAME COSMETICS SDB Consumer Staples 32 17 32 ORTIVUS 'B' Health Care 13 0 13 PA RESOURCES 'B' Energy 6 0 6 PARTNERTECH Information Technology 56 0 56 PEAB 'B' Industrials 68 5 68 POOLIA 'B' Industrials 63 0 63 PREVAS 'B' Information Technology 13 0 13 PROACT IT GROUP Information Technology 9 0 9 PROFFICE 'B' Industrials 52 0 52 PROFILGRUPPEN 'B' Materials 35 0 35 Q-MED Health Care 55 21 55 RATOS 'B' Financials 10 0 10 RAYSEARCH LABORATORIES Health Care 28 0 28 READSOFT 'B' Information Technology 36 0 36 REJLERKONCERNEN 'B' Industrials 1 0 1 RNB RETAIL AND BRANDS Consumer Discretionary 35 0 35 ROTTNEROS Materials 61 17 61 SAAB 'B' Industrials 78 23 78 SANDVIK Industrials 112 82 112 SAS Industrials 40 22 40 SCA 'B' Materials 112 69 112 SCANIA 'B' Industrials 87 63 87 SCRIBONA 'B' Information Technology 49 0 49 SEB 'A' Financials 112 77 112 SECO TOOLS 'B' Industrials 79 0 79 SECTRA 'B' Health Care 64 0 64 SECURITAS 'B' Industrials 108 90 108 SECURITAS SYSTEMS Industrials 8 3 8 SEMCON Information Technology 59 0 59 SENSYS TRAFFIC Information Technology 11 0 11 SIGMA B Information Technology 28 0 28 SKANSKA 'B' Industrials 108 56 108 SKF 'B' Industrials 109 95 109 SKISTAR 'B' Consumer Discretionary 20 0 20 SSAB 'A' Materials 89 57 89 STORA ENSO 'A' (OME) Materials 11 0 11 STUDSVIK Industrials 10 0 10 SWECO 'B' Industrials 49 0 49 SWEDBANK 'A' Financials 112 79 112 SVEDBERGS 'B' Industrials 35 0 35 SWEDISH MATCH Consumer Staples 81 56 81 SVENSKA HANDBKN.'A' Financials 112 78 112 SWITCHCORE Information Technology 3 0 3 TELE2 'B' Telecommunication Services 99 65 99 TELECA 'B' Information Technology 87 30 87 TELELOGIC Information Technology 53 17 53 TELIASONERA Telecommunication Services 81 66 81 TELIGENT Information Technology 11 0 11 THALAMUS NETWORKS 'B' Telecommunication Services 10 0 10 TICKET TRAVEL Consumer Discretionary 40 0 40 TIETOENATOR (OME) Information Technology 10 0 10 TRADEDOUBLER Information Technology 19 2 19 TRANSCOM WWD.SDB.B Industrials 47 0 47 TRELLEBORG 'B' Industrials 82 45 82 UNIFLEX 'B' Industrials 22 0 22 WALLENSTAM 'B' Financials 42 0 42 WEDINS SKOR&ACCESSORIES Consumer Discretionary 1 0 1 WEST SIBERIAN RES.SDB Energy 17 0 17 WIHLBORGS FASTIGHETER Financials 21 1 21 VOLVO 'B' Industrials 111 82 111 XANO INDUSTRI 'B' Industrials 23 0 23 XPONCARD Information Technology 10 0 10 ZODIAK TELEVISION 'B' Consumer Discretionary 17 0 17 Table 39 (cont’d): Sample members, assigned GICS industry sector and total number of complete observations. 64 8.4. Appendix 4: Valuation error in RIV(TVC) The valuation bias of RIV(TVC) is calculated as the difference between ( TVC ) V0RIV : , UB T* ( TVC ) = Bv (oUB ) + ∑ V0RIV , UB t =1 T* ( TVC ) = Bv o + ∑ V0RIV ,CB t =1 = ( Bv E 0 (X t − r ⋅ Bv t −1 ) = R tE E 0 (X (t UB ) − ∆( Cb t ) − r ⋅ ( Bv (t −UB1 ) − Cb t −1 ) − Cb 0 ) + ∑ = R tE t =1 T* ( UB ) o RIV ( TVC ) 0 , UB V E 0 (X (t UB ) − r ⋅ Bv (t −UB1 ) ) R tE = Bv ) E 0 (X (t UB ) − r ⋅ Bv (t UB −1 ) +∑ R tE t =1 T* ( UB ) o The valuation bias of RIV(TVC): T* ( TVC ) ( TVC ) V0RIV − V0RIV = −Cb 0 + ∑ ,CB , UB t =1 E 0 (− ∆( Cb t ) + r ⋅ Cb t −1 ) R tE It can be inferred that: ( TVC ) ( TVC ) V0RIV − V0RIV + ,CB , UB E 0 (Cb T* ) T* RE =0 And hence: ( TVC ) ( TVC ) V0RIV − V0RIV =− ,CB , UB E 0 (Cb T * ) T* RE (Skogsvik and Juettner-Nauroth, 2007) 65 ( TVC ) V0RIV and ,CB 8.5. Appendix 5: Valuation error in RIV(PMB) The valuation error in RIV(PMB) V0 − P0 is derived from T V0RIV( PMB ) = Bv 0 + ∑ t =1 E 0 ( X t − rE ⋅ Bv t −1 ) q ⋅ Bv T + = P0 R tE R ET (RIV(PMB)) Where q is the correct adjustment for business goodwill/badwill at T* (i.e. company is in steady state): q ⋅ Bv T E 0 ( PT − Bv T ) = R TE R TE And q is estimated by PMB. The valuation error is subsequently a function of the failure in PMB to estimate q correctly: V0 − P0 = − ( PMB − q ) ⋅ Bv T R ET 66 8.6. Appendix 6: Valuation error in AEG(TVC) In order for the AEG(TVC) model to have no valuation bias with unbiased accounting principles, the horizon point in time is here set to T=(T*+1). With this value of T, the valuation of AEG(TVC): ( TVC ) V0AEG = , UB E 0 (X (1UB ) ) T* E 0 (X (t +UB1 ) + r ⋅ Div t − X (t UB ) ⋅ R E )/ rE +∑ rE R tE t =1 ( TVC ) V0AEG = ,CB E 0 (X 1 ) T* E 0 (X t +1 + r ⋅ Div t − X t ⋅ R E )/ rE +∑ = rE R tE t =1 = [ ] ) ( UB ) E 0 (X (1UB ) − ∆( Cb 1 )) T* E 0 (X (t UB − ∆( Cb t ))⋅ R E ) / rE +1 − ∆( Cb t +1 )) + r ⋅ Div t − (X t +∑ = t rE RE t =1 ( TVC ) ( TVC ) The difference between V0AEG and V0AEG : ,CB , UB ( TVC ) ( TVC ) V0AEG − V0AEG = ,CB , UB E 0 (− ∆( Cb1 )) T* E 0 [(− ∆( Cb t +1 )) + (Cb t ) ⋅ R E )]/ rE +∑ rE R tE t =1 Expressed together with the assumption of zero valuation error in the unconstraint AEG valuation model: ( TVC ) ( TVC ) V0AEG − V0AEG = ,CB , UB =− E 0 [(− ∆( Cb T* +1 )) + (Cb T* ) ⋅ R E )]/ rE T* RE E 0 [∆(Cb T* +1 )]/ rE T* RE (Skogsvik and Juettner-Nauroth, 2007) 67 − E 0 [(∆Cb T * ) ⋅ R E ]/ rE T* RE = 8.7. Appendix 7: Comparison Between the Valuation Error in AEG(TVC) and RIV(TVC) ( TVC ) ( TVC ) The valuation error in RIV(TVC) is V0RIV − V0RIV =− ,CB , UB E 0 (Cb T * ) T* RE , and given that the valuation bias is non-positive due to conservative biased accounting regime, the sign of the valuation error of the AEG(TVC) is indeterminate: ( TVC ) ( TVC ) V0AEG − V0AEG = ,CB , UB =− E 0 [(− ∆( Cb T* +1 )) + (Cb T* ) ⋅ R E )]/ rE T* RE E 0 [∆(Cb T* +1 )]/ rE − E 0 [(∆Cb T * ) ⋅ R E ]/ rE T* RE T* RE The following two conditions must both be fulfilled for the AEG(TVC) to dominate RIV(TVC): ( TVC ) ( TVC ) V0AEG − V0AEG >− ,CB , UB E 0 (Cb T* ) T* RE ( TVC ) ( TVC ) and V0AEG − V0AEG < ,CB , UB E 0 (Cb T* ) T* RE Solving for the two equations above: − E 0 [∆(Cb T * +1 )] rE ⋅ R E T* > E 0 (Cb T * ) T* RE ⇔ E 0 [Cb T * ⋅ rE − ∆(Cb T* +1 )] > 0 and − E 0 [∆(Cb T * +1 )] rE ⋅ R E T* <− E 0 (Cb T * ) T* RE ⇔ E 0 [Cb T * ⋅ rE − ∆(Cb T* +1 )] > 0 This implies that the valuation error of AEG(TVC) is smaller than the valuation error of RIV(TVC) if the expected growth of the conservative bias in period (T*+1) is smaller than E 0 (Cb T* ) ⋅ rE , but larger than − E0 (Cb T * ) ⋅ rE . (Skogsvik and Juettner-Nauroth, 2007) 68 = 8.8. Appendix 8: Beta Calculations 2.50 1.80 1.60 2.00 1.40 1.20 Beta 0.80 1.00 0.60 0.40 0.50 0.20 Chart 31: Average (1998-2007) beta values per industry sector. 69 Consumer Staples Energy Financials Health Care Industrials Information Technology Materials Telecommunication Services 2002 0.8589 0.0996 0.7542 0.8779 0.4046 0.6816 1.9807 0.5130 1.2016 2003 0.8786 0.2045 0.8645 1.0167 0.6593 0.8705 2.0107 0.6295 1.2447 2004 0.7507 0.2786 0.9503 0.9267 0.7169 0.9573 2.0587 0.6749 1.0413 2005 0.7104 0.3777 0.9954 0.8103 0.5603 0.9764 2.0658 0.6275 1.0100 2006 0.8150 0.5132 1.1527 0.9969 0.6733 1.1285 1.2986 0.9587 0.9124 2007 0.8852 0.5723 1.1704 1.0552 0.6488 1.1684 1.0151 1.1475 0.8280 2007-10-31 2007-04-30 Consumer Discretionary Chart 32: Estimated beta values per industry sector historically. GICS Sector 1998 1999 2000 2001 Consumer Discretionary 0.9272 0.9313 0.7403 0.6383 Consumer Staples 0.3979 0.2182 0.1134 Energy 0.8651 0.8464 0.3718 0.3845 Financials 0.8789 0.9144 0.6868 0.6221 Health Care 0.8365 0.7170 0.3538 0.1109 Industrials 0.8687 0.8064 0.4254 0.3752 Information Technology 1.5740 1.6932 1.8373 1.9835 Materials 0.8042 0.7479 0.4068 0.3038 Telecommunication Services 1.0981 1.1438 1.2231 1.1501 Table 40: Average estimated beta values per industry sector and year. 2006-10-31 2006-04-30 2005-10-31 2005-04-30 2004-10-31 2004-04-30 2003-10-31 2003-04-30 2002-10-31 2002-04-30 2001-10-31 2001-04-30 2000-10-31 2000-04-30 1999-10-31 1999-04-30 1998-10-31 1998-04-30 Telecommunication Services Materials Information Technology Industrials Health Care Financials Energy Consumer Staples Avg(Beta) 1997-10-31 0.00 0.00 Consumer Discretionary Beta 1.50 1.00 8.9. Appendix 9: Average Absolute Valuation errors per Sector and Year GICS Sector 1998 1999 2000 2001 2002 2003 2004 2005 2006 Consumer Discretionary 0.5944 0.6266 0.5807 0.6177 0.6585 0.4969 0.5581 0.6626 0.6873 Consumer Staples 0.7468 0.7045 0.7868 0.8107 0.7101 0.7104 0.7593 0.7153 Energy 0.5339 0.6000 0.7171 0.5253 0.3751 0.3522 0.3397 0.5072 0.4579 Financials 0.5699 0.5407 0.5352 0.5436 0.5003 0.3655 0.4425 0.5027 0.4372 Health Care 1.1787 0.7521 0.7150 0.4923 0.8222 0.7728 0.7691 0.8281 0.8515 Industrials 0.5458 0.5945 0.5549 0.5985 0.6376 0.4153 0.4948 0.5872 0.6549 Information Technology 0.8041 0.7401 0.7781 0.9021 0.4186 0.4636 0.5941 0.6295 0.6799 Materials 0.3512 0.3151 0.3130 0.2818 0.3317 0.2613 0.2914 0.3296 0.5090 Telecommunication Services 0.8927 0.8976 0.8775 0.6986 0.4388 0.2619 0.2729 0.1933 0.3788 Table 41: Average absolute valuation error in book value of owners’ equity measured per industry sector and year. 2007 0.7364 0.7629 0.4353 0.4699 0.8483 0.7021 0.6777 0.4807 0.5695 GICS Sector 1998 1999 2000 2001 2002 2003 2004 Consumer Discretionary 0.6647 0.5916 0.5755 0.5881 0.6493 0.4457 0.4591 Consumer Staples 0.5934 0.5176 0.6038 0.6578 0.5078 0.5436 Energy 0.6033 0.5815 0.6785 0.7009 0.5377 0.2825 0.2465 Financials 0.5162 0.5025 0.4752 0.4661 0.4142 0.3061 0.3611 Health Care 1.1142 0.6260 0.5841 0.4548 0.7228 0.6439 0.6788 Industrials 0.4571 0.5250 0.4728 0.5062 0.5290 0.3343 0.3862 Information Technology 0.7517 0.6632 0.7618 0.9209 0.4319 0.4315 0.5529 Materials 0.3394 0.2538 0.2327 0.2184 0.2219 0.2163 0.2317 Telecommunication Services 0.8458 0.8456 0.8411 0.7033 0.4622 0.2611 0.2068 Table 42: Average absolute valuation error in RIV(TVC) measured per industry sector and year. 2005 0.5383 0.5964 0.3883 0.4229 0.7434 0.4717 0.5797 0.2556 0.1504 2006 0.5691 0.5877 0.4211 0.3800 0.7651 0.5494 0.5868 0.3812 0.3153 2007 0.6199 0.6455 0.3942 0.4160 0.7655 0.5946 0.5700 0.3843 0.5038 GICS Sector 1998 1999 2000 2001 2002 2003 2004 Consumer Discretionary 0.9816 0.6755 0.7341 0.8418 0.7949 0.6435 0.4550 Consumer Staples 0.3192 0.2049 0.3424 0.4120 0.2415 0.3022 Energy 2.1066 2.2956 1.8859 1.7264 1.5616 1.0536 0.2227 Financials 0.2275 0.3428 0.3875 0.2471 0.2087 0.3203 0.2239 Health Care 1.2833 0.5199 0.6919 0.3077 0.3698 0.3401 0.3410 Industrials 0.4087 0.4468 0.4538 0.4889 0.4691 0.3181 0.2837 Information Technology 0.5758 0.5965 0.7328 1.1617 0.4570 0.5082 0.4644 Materials 0.5642 0.2892 0.4053 0.2840 0.1409 0.4049 0.3205 Telecommunication Services 0.7514 0.7609 0.7541 0.5275 0.3770 0.2940 0.1871 Table 43: Average absolute valuation error in RIV(PMB) measured per industry sector and year. 2005 0.3971 0.3856 0.0752 0.2393 0.4060 0.3459 0.4703 0.3081 0.3547 2006 0.4075 0.3904 0.2510 0.2442 0.4010 0.4379 0.4505 0.2525 0.3895 2007 0.4271 0.4758 0.1799 0.3104 0.3938 0.4894 0.4035 0.2890 0.2806 GICS Sector 1998 1999 2000 2001 2002 2003 2004 Consumer Discretionary 2.0530 1.3389 1.6136 1.6198 1.5863 1.5477 1.0316 Consumer Staples 0.4510 0.6705 0.3705 0.3433 0.4969 0.3911 Energy 1.6244 1.7458 1.4986 1.3975 1.2331 0.7823 0.1163 Financials 0.1696 0.3505 0.4580 0.3334 0.2959 0.5679 0.3892 Health Care 1.7915 1.0652 1.0899 0.7795 0.7549 0.5927 0.4271 Industrials 0.6877 0.6145 0.8072 0.7382 0.6982 0.8161 0.4347 Information Technology 0.4593 0.8066 0.9584 2.7940 1.2041 1.8901 0.8969 Materials 0.5806 0.3003 0.4208 0.2959 0.1515 0.4179 0.3329 Telecommunication Services 0.5757 0.6033 0.5922 0.2115 0.7392 0.8841 0.8749 Table 44: Average absolute valuation error in RIV(Q) equity measured per industry sector and year. 2005 0.6723 0.3060 0.1551 0.3348 0.2902 0.3269 0.8977 0.3181 1.1468 2006 0.5483 0.4902 0.2219 0.3707 0.2455 0.2988 0.8313 0.2486 0.9027 2007 0.4566 0.5255 0.1976 0.4021 0.2296 0.3188 0.8181 0.2879 0.3995 GICS Sector 1998 1999 2000 2001 2002 2003 2004 Consumer Discretionary 0.9971 0.6472 0.6937 0.6632 0.5083 0.5569 0.4766 Consumer Staples 0.2269 0.3944 0.3415 0.2466 0.6297 0.3238 Energy 2.8301 3.3191 0.2991 1.8405 0.7797 0.4694 0.2254 Financials 0.2666 0.3131 0.2768 0.2251 0.1030 0.2281 0.2251 Health Care 0.3598 0.4036 0.6387 0.7114 0.3241 0.3415 0.4124 Industrials 0.3196 0.3717 0.5727 0.6098 0.2827 0.3230 0.2348 Information Technology 0.6893 0.5800 0.7474 0.7363 0.5613 0.6363 0.5895 Materials 0.4251 0.2805 1.0107 0.9390 0.2511 0.3794 0.3818 Telecommunication Services 0.8142 0.7812 0.7851 0.7327 0.6989 0.3705 0.1003 Table 45: Average absolute valuation error in PVEE(rE) measured per industry sector and year. 2005 0.3166 0.3752 0.1938 0.2757 0.4493 0.2461 0.5169 0.6690 0.1605 2006 0.2527 0.1189 0.5746 0.2698 0.4868 0.2546 0.3781 0.3590 0.3133 2007 0.2908 0.1838 0.3992 0.3021 0.5031 0.2909 0.3111 0.2445 0.3888 70 GICS Sector 1998 1999 2000 2001 2002 2003 2004 Consumer Discretionary 1.7187 0.9684 1.1777 0.9913 0.9640 1.3306 1.0003 Consumer Staples 0.5219 0.5991 0.4571 0.3383 0.9164 0.6596 Energy 5.7250 6.8951 0.2459 2.6168 1.8482 1.5989 1.3064 Financials 0.6520 0.5516 0.5131 0.6751 0.6580 0.8002 0.7769 Health Care 0.5286 0.6396 0.7587 0.6959 0.3889 0.5578 0.4287 Industrials 0.9529 0.6946 0.9172 0.9459 0.5977 0.8932 0.7846 Information Technology 0.3535 0.5319 0.8290 1.6039 0.8587 0.6320 0.5356 Materials 1.2797 0.5099 1.5096 1.4056 0.7363 0.9842 1.1472 Telecommunication Services 0.6375 0.5718 0.5824 0.4851 0.4735 0.3535 0.8080 Table 46: Average absolute valuation error in PVEE(rf) measured per industry sector and year. 2005 0.9935 1.0110 1.5975 1.0742 0.3324 1.1340 0.7990 1.6861 1.1745 2006 0.7334 0.5762 0.9707 0.7772 0.2426 0.7922 0.6276 1.1832 0.5727 2007 0.4745 0.3184 0.6108 0.6724 0.2431 0.5671 0.6445 1.0940 0.4261 GICS Sector 1998 1999 2000 2001 2002 2003 2004 Consumer Discretionary 1.0991 0.5812 0.7840 0.7610 0.5625 0.6278 0.4988 Consumer Staples 0.2845 0.7054 0.7026 0.3380 0.7326 0.4969 Energy 1.0538 0.2981 1.7813 1.4198 1.8145 0.5941 0.5867 Financials 0.2343 0.2319 0.2296 0.2461 0.1541 0.2564 0.2395 Health Care 0.1539 0.3611 0.5552 0.3186 0.2490 0.3177 0.3292 Industrials 0.3884 0.3600 0.7538 0.7590 0.4600 0.3817 0.2182 Information Technology 0.4371 0.4831 0.6682 1.0891 0.3755 0.4339 0.4245 Materials 0.5601 0.3577 1.0200 0.6544 0.3514 0.4891 0.2526 Telecommunication Services 0.5396 0.5597 0.6806 0.6359 0.3530 0.1974 0.1481 Table 47: Average absolute valuation error in AEG(TVC) measured per industry sector and year. 2005 0.4213 0.5722 0.4698 0.3016 0.3069 0.2069 0.3867 0.3643 0.2143 2006 0.2156 0.1875 0.3537 0.2449 0.2837 0.1754 0.2796 0.2155 0.1384 2007 0.2104 0.1584 0.2500 0.2812 0.2387 0.2011 0.2580 0.1487 0.1220 71 8.10. Appendix 10: Empirical Results 1998-2002 Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary -0.4254 0.0300 -0.4844 -0.3664 0.6165 0.0183 0.5804 0.6526 5 Consumer Staples -0.7439 0.0114 -0.7666 -0.7212 0.7439 0.0114 0.7212 0.7666 7 Energy 0.5352 0.0358 0.4605 0.6100 0.5352 0.0358 0.4605 0.6100 3 Financials -0.4911 0.0148 -0.5202 -0.4620 0.5345 0.0102 0.5145 0.5544 2 Health Care -0.4173 0.0707 -0.5577 -0.2770 0.7681 0.0283 0.7118 0.8243 8 Industrials -0.4599 0.0142 -0.4877 -0.4320 0.5823 0.0082 0.5662 0.5983 4 Information Technology -0.5806 0.0413 -0.6618 -0.4995 0.7889 0.0283 0.7332 0.8446 9 Materials -0.2807 0.0182 -0.3165 -0.2448 0.3154 0.0151 0.2856 0.3452 1 Telecommunication Services -0.6739 0.0396 -0.7532 -0.5947 0.7034 0.0304 0.6426 0.7643 6 Table 48: Average valuation error and absolute valuation error in book value of owners’ equity, with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.4665 0.0099 -0.4860 -0.4470 0.6003 0.0064 0.5877 0.6129 Table 49: Average valuation error and absolute valuation error in book value of owners’ equity, with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.3012 0.0335 Consumer Staples -0.5696 0.0120 Energy 0.6232 0.0337 Financials -0.4297 0.0144 Health Care -0.3178 0.0671 Industrials -0.3250 0.0153 Information Technology -0.5098 0.0437 Materials -0.1327 0.0197 Telecommunication Services -0.6793 0.0324 Table 50: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.3670 -0.2354 -0.5934 -0.5459 0.5528 0.6935 -0.4580 -0.4014 -0.4510 -0.1846 -0.3550 -0.2951 -0.5958 -0.4239 -0.1716 -0.0938 -0.7441 -0.6144 error in RIV(TVC), Abs(V.E.) Mean Std. Error 0.6046 0.0185 0.5696 0.0120 0.6232 0.0337 0.4721 0.0104 0.6650 0.0326 0.4974 0.0091 0.7627 0.0299 0.2475 0.0133 0.6916 0.0280 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.5683 0.6410 5 0.5459 0.5934 4 0.5528 0.6935 6 0.4517 0.4925 2 0.6004 0.7297 7 0.4794 0.5153 3 0.7039 0.8215 9 0.2213 0.2737 1 0.6356 0.7476 8 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.3556 0.0106 -0.3763 -0.3349 0.5374 0.0068 0.5241 0.5508 Table 51: Average valuation error and absolute valuation error in RIV(TVC), with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary 0.1311 0.0500 Consumer Staples -0.2822 0.0168 Energy 1.8623 0.0724 Financials -0.0984 0.0215 Health Care 0.4471 0.0924 Industrials -0.1322 0.0186 Information Technology -0.2563 0.0616 Materials 0.2045 0.0266 Telecommunication Services -0.4718 0.0511 Table 52: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper 0.0328 0.2295 -0.3156 -0.2489 1.7113 2.0133 -0.1407 -0.0561 0.2637 0.6304 -0.1687 -0.0957 -0.3774 -0.1352 0.1521 0.2570 -0.5739 -0.3697 error in RIV(PMB), Abs(V.E.) Mean Std. Error 0.7713 0.0294 0.2852 0.0162 1.8623 0.0724 0.3086 0.0155 0.6081 0.0826 0.4564 0.0120 0.7724 0.0460 0.3447 0.0181 0.5842 0.0269 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.7135 0.8292 7 0.2530 0.3175 1 1.7113 2.0133 9 0.2780 0.3391 2 0.4442 0.7719 6 0.4328 0.4800 4 0.6819 0.8628 8 0.3090 0.3805 3 0.5304 0.6380 5 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.0521 0.0148 -0.0811 -0.0230 0.5241 0.0105 0.5034 0.5447 Table 53: Average valuation error and absolute valuation error in RIV(PMB), with standard error and a 95 percent confidence interval (C.I.). 72 Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary 1.2021 0.0944 1.0165 1.3878 1.5753 0.0773 1.4233 1.7273 9 Consumer Staples 0.4949 0.0369 0.4217 0.5681 0.5097 0.0346 0.4410 0.5784 3 Energy 1.4648 0.0551 1.3499 1.5797 1.4648 0.0551 1.3499 1.5797 8 Financials 0.1778 0.0284 0.1219 0.2337 0.3624 0.0235 0.3162 0.4085 2 Health Care 1.0232 0.1164 0.7922 1.2542 1.0642 0.1126 0.8407 1.2877 6 Industrials 0.5104 0.0310 0.4496 0.5712 0.7207 0.0262 0.6692 0.7722 5 Information Technology 0.8146 0.1377 0.5436 1.0856 1.2816 0.1260 1.0336 1.5295 7 Materials 0.2227 0.0270 0.1695 0.2759 0.3581 0.0185 0.3217 0.3945 1 Telecommunication Services -0.0855 0.0870 -0.2594 0.0885 0.5497 0.0538 0.4422 0.6573 4 Table 54: Average valuation error and absolute valuation error in RIV(Q), with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.5848 0.0270 0.5319 0.6378 0.8359 0.0242 0.7884 0.8833 Table 55: Average valuation error and absolute valuation error in RIV(Q), with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary 0.0831 0.0474 Consumer Staples 0.2885 0.0322 Energy 1.5222 0.3278 Financials -0.0752 0.0167 Health Care -0.2118 0.0521 Industrials 0.1691 0.0233 Information Technology -0.4812 0.0356 Materials 0.5062 0.0669 Telecommunication Services -0.7474 0.0162 Table 56: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.0102 0.1764 0.2245 0.3525 0.8384 2.2060 -0.1080 -0.0424 -0.3152 -0.1084 0.1235 0.2148 -0.5512 -0.4113 0.3744 0.6380 -0.7797 -0.7151 error in PVEE(rE), Abs(V.E.) Mean Std. Error 0.6609 0.0321 0.3234 0.0284 1.6708 0.2894 0.2452 0.0117 0.5000 0.0254 0.4708 0.0184 0.6941 0.0218 0.6536 0.0603 0.7474 0.0162 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.5977 0.7241 6 0.2670 0.3798 2 1.0671 2.2744 9 0.2221 0.2683 1 0.4497 0.5504 4 0.4346 0.5069 3 0.6512 0.7370 7 0.5348 0.7724 5 0.7151 0.7797 8 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.0409 0.0153 0.0109 0.0710 0.5191 0.0113 0.497 0.5413 Table 57: Average valuation error and absolute valuation error in PVEE(rE), with standard error and a 95 percent confidence interval (C.I.). V.E. 95 % C.I. GICS Sector Mean Std. Error Lower Upper Consumer Discretionary 0.7766 0.0789 0.6215 0.9318 Consumer Staples 0.5196 0.0365 0.4471 0.5922 Energy 3.0551 0.5808 1.8436 4.2666 Financials 0.4778 0.0262 0.4263 0.5293 Health Care 0.1112 0.0738 -0.0352 0.2577 Industrials 0.6783 0.0318 0.6159 0.7408 Information Technology 0.2772 0.0909 0.0985 0.4560 Materials 1.0745 0.0804 0.9160 1.2331 Telecommunication Services -0.5092 0.0323 -0.5738 -0.4446 Table 58: Average valuation error and absolute valuation error in PVEE(rf), interval (C.I.) per sector and ranked in ascending order. Abs(V.E.) Mean Std. Error 1.0894 0.0676 0.5265 0.0355 3.1297 0.5606 0.5880 0.0195 0.6260 0.0402 0.8345 0.0276 0.8853 0.0776 1.1207 0.0773 0.5279 0.0272 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.9565 1.2223 7 0.4561 0.5969 1 1.9603 4.2991 9 0.5497 0.6264 3 0.5462 0.7057 4 0.7802 0.8887 5 0.7325 1.0380 6 0.9684 1.2730 8 0.4736 0.5821 2 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.6035 0.0235 0.5574 0.6496 0.854 0.0202 0.8145 0.8936 Table 59: Average valuation error and absolute valuation error in PVEE(rf), with standard error and a 95 percent confidence interval (C.I.). 73 V.E. GICS Sector Mean Std. Error Consumer Discretionary 0.2696 0.0499 Consumer Staples 0.5531 0.0502 Energy 1.3887 0.1634 Financials -0.0178 0.0151 Health Care 0.0848 0.0476 Industrials 0.4205 0.0267 Information Technology -0.1478 0.0582 Materials 0.6365 0.0543 Telecommunication Services -0.5260 0.0258 Table 60: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Abs(V.E.) Lower Upper Mean Std. Error 0.1713 0.3678 0.7069 0.0358 0.4534 0.6527 0.5621 0.0490 1.0478 1.7295 1.3887 0.1634 -0.0475 0.0120 0.2211 0.0102 -0.0096 0.1793 0.3703 0.0309 0.3682 0.4728 0.5861 0.0231 -0.2623 -0.0334 0.6879 0.0443 0.5294 0.7436 0.6588 0.0530 -0.5776 -0.4745 0.5341 0.0230 error in AEG(TVC), with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.6364 0.7773 8 0.4647 0.6595 4 1.0478 1.7295 9 0.2011 0.2411 1 0.3091 0.4315 2 0.5406 0.6315 5 0.6007 0.7750 7 0.5543 0.7632 6 0.4881 0.5800 3 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.2518 0.0167 0.2191 0.2844 0.5614 0.0133 0.5354 0.5875 Table 61: Average valuation error and absolute valuation error in AEG(TVC), with standard error and a 95 percent confidence interval (C.I.). 74 8.11. Appendix 11: Empirical Results 2003-2007 Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary -0.6136 0.0097 -0.6326 -0.5946 0.6417 0.0076 0.6267 0.6567 7 Consumer Staples -0.7338 0.0098 -0.7530 -0.7145 0.7338 0.0098 0.7145 0.7530 8 Energy -0.3141 0.0377 -0.3890 -0.2391 0.4187 0.0233 0.3725 0.4650 3 Financials -0.3830 0.0113 -0.4052 -0.3607 0.4457 0.0080 0.4300 0.4613 4 Health Care -0.8150 0.0059 -0.8266 -0.8033 0.8150 0.0059 0.8033 0.8266 9 Industrials -0.5625 0.0060 -0.5743 -0.5507 0.5874 0.0047 0.5782 0.5965 5 Information Technology -0.5536 0.0118 -0.5767 -0.5304 0.6229 0.0074 0.6084 0.6375 6 Materials -0.3204 0.0150 -0.3499 -0.2908 0.3848 0.0108 0.3635 0.4061 2 Telecommunication Services -0.2842 0.0260 -0.3355 -0.2329 0.3376 0.0209 0.2964 0.3789 1 Table 62: Average valuation error and absolute valuation error in book value of owners’ equity, with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.5407 0.0041 -0.5488 -0.5325 0.5804 0.0031 0.5743 0.5865 Table 63: Average valuation error and absolute valuation error in book value of owners’ equity, with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.4808 0.0105 Consumer Staples -0.5853 0.0079 Energy -0.2750 0.0317 Financials -0.3306 0.0095 Health Care -0.7215 0.0064 Industrials -0.4525 0.0058 Information Technology -0.5029 0.0101 Materials -0.2221 0.0131 Telecommunication Services -0.2379 0.0234 Table 64: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.5013 -0.4602 -0.6008 -0.5697 -0.3381 -0.2119 -0.3493 -0.3120 -0.7341 -0.7090 -0.4637 -0.4412 -0.5227 -0.4831 -0.2477 -0.1964 -0.2842 -0.1916 error in RIV(TVC), Abs(V.E.) Mean Std. Error 0.5364 0.0072 0.5853 0.0079 0.3642 0.0188 0.3809 0.0068 0.7215 0.0064 0.4825 0.0044 0.5536 0.0068 0.3009 0.0085 0.2883 0.0189 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.5222 0.5506 6 0.5697 0.6008 8 0.3268 0.4015 3 0.3676 0.3941 4 0.7090 0.7341 9 0.4739 0.4910 5 0.5403 0.5670 7 0.2842 0.3176 2 0.2509 0.3257 1 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.4471 0.0038 -0.4545 -0.4396 0.4891 0.0028 0.4835 0.4946 Table 65: Average valuation error and absolute valuation error in RIV(TVC), with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.1754 0.0165 Consumer Staples -0.3722 0.0145 Energy 0.1836 0.0548 Financials -0.0127 0.0132 Health Care -0.2683 0.0176 Industrials -0.3023 0.0073 Information Technology -0.2372 0.0157 Materials 0.0709 0.0180 Telecommunication Services 0.1087 0.0315 Table 66: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.2077 -0.1430 -0.4008 -0.3436 0.0747 0.2926 -0.0386 0.0133 -0.3029 -0.2338 -0.3166 -0.2880 -0.2681 -0.2064 0.0355 0.1063 0.0464 0.1710 error in RIV(PMB), Abs(V.E.) Mean Std. Error 0.4549 0.0097 0.3755 0.0141 0.3582 0.0438 0.2691 0.0092 0.3777 0.0109 0.3854 0.0050 0.4535 0.0096 0.3082 0.0105 0.3110 0.0195 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.4359 0.4739 9 0.3477 0.4034 5 0.2712 0.4453 4 0.2510 0.2872 1 0.3563 0.3990 6 0.3756 0.3951 7 0.4346 0.4724 8 0.2876 0.3288 2 0.2724 0.3496 3 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.1900 0.0055 -0.2008 -0.1792 0.3839 0.0034 0.3772 0.3906 Table 67: Average valuation error and absolute valuation error in RIV(PMB), with standard error and a 95 percent confidence interval (C.I.). 75 Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary 0.5811 0.0318 0.5188 0.6435 0.7912 0.0268 0.7387 0.8438 7 Consumer Staples 0.2038 0.0329 0.1388 0.2687 0.4478 0.0200 0.4084 0.4872 6 Energy 0.0365 0.0474 -0.0577 0.1307 0.2994 0.0351 0.2296 0.3691 1 Financials 0.2525 0.0166 0.2200 0.2851 0.4083 0.0121 0.3845 0.4321 4 Health Care 0.0730 0.0263 0.0214 0.1247 0.3499 0.0193 0.3119 0.3879 3 Industrials 0.1980 0.0127 0.1730 0.2230 0.4106 0.0099 0.3912 0.4300 5 Information Technology 0.8849 0.0403 0.8058 0.9641 0.9931 0.0377 0.9192 1.0670 9 Materials 0.0867 0.0183 0.0507 0.1226 0.3136 0.0109 0.2922 0.3350 2 Telecommunication Services 0.7540 0.0483 0.6585 0.8495 0.8519 0.0347 0.7833 0.9204 8 Table 68: Average valuation error and absolute valuation error in RIV(Q), with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.3747 0.0106 0.3538 0.3955 0.5666 0.0091 0.5487 0.5845 Table 69: Average valuation error and absolute valuation error in RIV(Q), with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.0149 0.0155 Consumer Staples 0.1702 0.0226 Energy -0.0886 0.0536 Financials -0.1186 0.0107 Health Care -0.3890 0.0154 Industrials -0.1316 0.0070 Information Technology -0.4398 0.0096 Materials 0.1978 0.0272 Telecommunication Services -0.2269 0.0214 Table 70: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.0454 0.0156 0.1256 0.2148 -0.1951 0.0179 -0.1397 -0.0975 -0.4193 -0.3588 -0.1453 -0.1178 -0.4586 -0.4210 0.1444 0.2513 -0.2693 -0.1845 error in PVEE(rE), Abs(V.E.) Mean Std. Error 0.3608 0.0105 0.2866 0.0168 0.4307 0.0288 0.2643 0.0068 0.4411 0.0110 0.2677 0.0047 0.4679 0.0081 0.3995 0.0213 0.2689 0.0176 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.3402 0.3814 5 0.2534 0.3198 4 0.3734 0.4880 7 0.2510 0.2775 1 0.4196 0.4627 8 0.2585 0.2769 2 0.4521 0.4837 9 0.3577 0.4414 6 0.2341 0.3037 3 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.1432 0.0053 -0.1536 -0.1328 0.338 0.0035 0.3311 0.3449 Table 71: Average valuation error and absolute valuation error in PVEE(rE), with standard error and a 95 percent confidence interval (C.I.). V.E. 95 % C.I. GICS Sector Mean Std. Error Lower Upper Consumer Discretionary 0.7926 0.0276 0.7384 0.8468 Consumer Staples 0.6482 0.0251 0.5988 0.6977 Energy 0.8316 0.1018 0.6292 1.0340 Financials 0.7436 0.0212 0.7020 0.7853 Health Care 0.0097 0.0246 -0.0386 0.0581 Industrials 0.7851 0.0139 0.7579 0.8123 Information Technology 0.4342 0.0230 0.3891 0.4794 Materials 1.1722 0.0482 1.0776 1.2669 Telecommunication Services 0.5766 0.0470 0.4837 0.6695 Table 72: Average valuation error and absolute valuation error in PVEE(rf), interval (C.I.) per sector and ranked in ascending order. Abs(V.E.) Mean Std. Error 0.8641 0.0254 0.6608 0.0236 1.0125 0.0808 0.8053 0.0182 0.3552 0.0162 0.8224 0.0127 0.6417 0.0173 1.2178 0.0454 0.6729 0.0367 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.8143 0.9139 7 0.6142 0.7073 3 0.8519 1.1732 8 0.7695 0.8410 5 0.3233 0.3871 1 0.7974 0.8473 6 0.6078 0.6757 2 1.1286 1.3070 9 0.6004 0.7454 4 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.6938 0.0096 0.6750 0.7126 0.7896 0.0083 0.7734 0.8058 Table 73: Average valuation error and absolute valuation error in PVEE(rf), with standard error and a 95 percent confidence interval (C.I.). 76 V.E. GICS Sector Mean Std. Error Consumer Discretionary 0.2180 0.0160 Consumer Staples 0.3365 0.0243 Energy -0.0002 0.0538 Financials -0.0881 0.0111 Health Care -0.1144 0.0175 Industrials 0.0466 0.0071 Information Technology -0.1927 0.0118 Materials 0.1694 0.0170 Telecommunication Services -0.0231 0.0174 Table 74: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Abs(V.E.) Lower Upper Mean Std. Error 0.1866 0.2493 0.3689 0.0129 0.2887 0.3843 0.3792 0.0214 -0.1071 0.1067 0.3891 0.0339 -0.1099 -0.0663 0.2647 0.0067 -0.1487 -0.0800 0.2960 0.0102 0.0327 0.0605 0.2259 0.0051 -0.2158 -0.1695 0.3461 0.0073 0.1359 0.2028 0.2779 0.0132 -0.0575 0.0113 0.1629 0.0108 error in AEG(TVC), with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.3437 0.3942 7 0.3371 0.4214 8 0.3216 0.4565 9 0.2514 0.2779 3 0.2760 0.3160 5 0.2160 0.2359 2 0.3316 0.3605 6 0.2520 0.3038 4 0.1416 0.1841 1 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.0257 0.0051 0.0157 0.0357 0.2889 0.0035 0.282 0.2958 Table 75: Average valuation error and absolute valuation error in AEG(TVC), with standard error and a 95 percent confidence interval (C.I.). 77 8.12. Appendix 12: Empirical Results Five or More Consensus Estimates (1998-2007) Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary -0.5787 0.0181 -0.6142 -0.5432 0.6238 0.0142 0.5959 0.6517 6 Consumer Staples -0.8253 0.0090 -0.8432 -0.8073 0.8253 0.0090 0.8073 0.8432 9 Energy -0.3747 . . . 0.3747 . . . 1 Financials -0.4599 0.0087 -0.4769 -0.4429 0.4684 0.0075 0.4536 0.4832 4 Health Care -0.7968 0.0068 -0.8104 -0.7833 0.7968 0.0068 0.7833 0.8104 8 Industrials -0.5144 0.0096 -0.5333 -0.4956 0.5585 0.0067 0.5454 0.5716 5 Information Technology -0.6713 0.0220 -0.7146 -0.6280 0.7100 0.0148 0.6808 0.7393 7 Materials -0.3494 0.0144 -0.3779 -0.3210 0.3752 0.0122 0.3511 0.3993 2 Telecommunication Services -0.3802 0.0250 -0.4297 -0.3306 0.3993 0.0226 0.3545 0.4441 3 Table 76: Average valuation error and absolute valuation error in book value of owners’ equity, with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.5233 0.0059 -0.5349 -0.5117 0.5549 0.0047 0.5456 0.5641 Table 77: Average valuation error and absolute valuation error in book value of owners’ equity, with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.4576 0.0197 Consumer Staples -0.6439 0.0114 Energy -0.2837 . Financials -0.3699 0.0075 Health Care -0.6858 0.0122 Industrials -0.4023 0.0094 Information Technology -0.6303 0.0193 Materials -0.2351 0.0139 Telecommunication Services -0.3413 0.0249 Table 78: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.4964 -0.4188 -0.6667 -0.6212 . . -0.3846 -0.3551 -0.7100 -0.6615 -0.4206 -0.3839 -0.6684 -0.5922 -0.2625 -0.2076 -0.3906 -0.2920 error in RIV(TVC), Abs(V.E.) Mean Std. Error 0.5583 0.0124 0.6439 0.0114 0.2837 . 0.3764 0.0067 0.6858 0.0122 0.4543 0.0065 0.6513 0.0156 0.2931 0.0099 0.3573 0.0231 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.5338 0.5827 6 0.6212 0.6667 7 . . 1 0.3632 0.3895 4 0.6615 0.7100 9 0.4415 0.4671 5 0.6206 0.6819 8 0.2736 0.3126 2 0.3116 0.4031 3 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.4196 0.0059 -0.4311 -0.4081 0.465 0.0044 0.4563 0.4737 Table 79: Average valuation error and absolute valuation error in RIV(TVC), with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.1274 0.0327 Consumer Staples -0.4693 0.0198 Energy 0.1185 . Financials -0.0626 0.0112 Health Care -0.2075 0.0291 Industrials -0.2421 0.0117 Information Technology -0.4228 0.0301 Materials 0.0528 0.0188 Telecommunication Services -0.0298 0.0354 Table 80: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.1916 -0.0632 -0.5087 -0.4300 . . -0.0846 -0.0407 -0.2653 -0.1497 -0.2649 -0.2192 -0.4821 -0.3635 0.0158 0.0899 -0.1000 0.0403 error in RIV(PMB), Abs(V.E.) Mean Std. Error 0.5930 0.0172 0.4710 0.0194 0.1185 . 0.1734 0.0080 0.3200 0.0163 0.3760 0.0072 0.5636 0.0149 0.2748 0.0112 0.3289 0.0208 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.5592 0.6269 9 0.4324 0.5095 7 . . 1 0.1577 0.1891 2 0.2877 0.3524 4 0.3619 0.3902 6 0.5342 0.5931 8 0.2528 0.2969 3 0.2878 0.3700 5 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.1699 0.0084 -0.1863 -0.1534 0.3796 0.0053 0.3693 0.39 Table 81: Average valuation error and absolute valuation error in RIV(PMB), with standard error and a 95 percent confidence interval (C.I). 78 Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary 0.6905 0.0652 0.5623 0.8186 1.0376 0.0536 0.9322 1.1429 9 Consumer Staples 0.0027 0.0450 -0.0866 0.0920 0.3428 0.0270 0.2892 0.3965 5 Energy -0.0105 . . . 0.0105 . . . 1 Financials 0.1936 0.0144 0.1653 0.2218 0.2727 0.0110 0.2511 0.2943 2 Health Care 0.1527 0.0420 0.0695 0.2360 0.3091 0.0325 0.2447 0.3736 4 Industrials 0.2919 0.0204 0.2519 0.3318 0.4607 0.0169 0.4275 0.4938 6 Information Technology 0.4535 0.0765 0.3027 0.6044 0.6855 0.0675 0.5524 0.8186 7 Materials 0.0683 0.0191 0.0307 0.1059 0.2800 0.0115 0.2573 0.3027 3 Telecommunication Services 0.5500 0.0560 0.4392 0.6609 0.7342 0.0363 0.6623 0.8060 8 Table 82: Average valuation error and absolute valuation error in RIV(Q), with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.3236 0.0154 0.2934 0.3537 0.5227 0.0132 0.4968 0.5485 Table 83: Average valuation error and absolute valuation error in RIV(Q), with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.0220 0.0306 Consumer Staples 0.2414 0.0284 Energy 0.3429 . Financials -0.0085 0.0117 Health Care -0.2450 0.0422 Industrials -0.0457 0.0117 Information Technology -0.5320 0.0183 Materials 0.3054 0.0458 Telecommunication Services -0.3243 0.0285 Table 84: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.0821 0.0382 0.1851 0.2978 . . -0.0314 0.0144 -0.3288 -0.1613 -0.0686 -0.0228 -0.5680 -0.4960 0.2154 0.3955 -0.3807 -0.2678 error in PVEE(rE), Abs(V.E.) Mean Std. Error 0.4703 0.0207 0.2984 0.0216 0.3429 . 0.1847 0.0075 0.4300 0.0237 0.2904 0.0073 0.5425 0.0167 0.5086 0.0397 0.3539 0.0257 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.4295 0.5110 7 0.2555 0.3413 3 . . 4 0.1699 0.1996 1 0.3831 0.4769 6 0.2762 0.3046 2 0.5096 0.5754 9 0.4305 0.5866 8 0.3031 0.4048 5 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.0425 0.0099 -0.0619 -0.0232 0.356 0.0071 0.342 0.3701 Table 85: Average valuation error and absolute valuation error in PVEE(rE), with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary 0.7042 0.0510 Consumer Staples 0.6669 0.0275 Energy 1.8383 . Financials 0.8235 0.0245 Health Care 0.1583 0.0549 Industrials 0.7368 0.0198 Information Technology 0.1938 0.0428 Materials 1.1601 0.0643 Telecommunication Services 0.3624 0.0606 Table 86: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper 0.6039 0.8044 0.6122 0.7216 . . 0.7754 0.8716 0.0495 0.2672 0.6980 0.7756 0.1095 0.2781 1.0336 1.2865 0.2425 0.4823 error in PVEE(rf), Abs(V.E.) Mean Std. Error 0.8675 0.0448 0.6669 0.0275 1.8383 . 0.8478 0.0225 0.4672 0.0334 0.8073 0.0168 0.5218 0.0260 1.2075 0.0615 0.6864 0.0326 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.7794 0.9556 7 0.6122 0.7216 3 . . 9 0.8037 0.8920 6 0.4009 0.5335 1 0.7745 0.8402 5 0.4705 0.5732 2 1.0866 1.3284 8 0.6220 0.7508 4 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.7120 0.0155 0.6817 0.7424 0.8259 0.0132 0.7999 0.8518 Table 87: Average valuation error and absolute valuation error in PVEE(rf), with standard error and a 95 percent confidence interval (C.I.). 79 V.E. 95 % C.I. Abs(V.E.) GICS Sector Mean Std. Error Lower Upper Mean Std. Error Consumer Discretionary 0.1693 0.0321 0.1061 0.2324 0.4700 0.0243 Consumer Staples 0.4682 0.0370 0.3946 0.5417 0.4714 0.0366 Energy -0.1474 . . . 0.1474 . Financials 0.0336 0.0115 0.0111 0.0562 0.1877 0.0072 Health Care -0.0605 0.0397 -0.1392 0.0182 0.3212 0.0245 Industrials 0.1088 0.0120 0.0854 0.1323 0.2813 0.0086 Information Technology -0.3772 0.0213 -0.4191 -0.3352 0.4186 0.0171 Materials 0.2428 0.0320 0.1798 0.3057 0.3334 0.0293 Telecommunication Services -0.1455 0.0287 -0.2023 -0.0887 0.2657 0.0211 Table 88: Average valuation error and absolute valuation error in AEG(TVC), with standard error interval (C.I.) per sector and ranked in ascending order. Rank 95 % C.I. Lower Upper Abs(V.E.) 0.4222 0.5178 8 0.3988 0.5441 9 . . 1 0.1735 0.2020 2 0.2726 0.3697 5 0.2644 0.2983 4 0.3849 0.4522 7 0.2757 0.3911 6 0.2241 0.3074 3 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.0789 0.0091 0.0611 0.0967 0.3205 0.0068 0.3071 0.3339 Table 89: Average valuation error and absolute valuation error in AEG(TVC), with standard error and a 95 percent confidence interval (C.I.). 80 8.13. Appendix 13: Empirical Results 5% Equity Risk Premium (1998-2007) Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary -0.5640 0.0109 -0.5854 -0.5426 0.6350 0.0074 0.6205 0.6496 6 Consumer Staples -0.7367 0.0077 -0.7518 -0.7215 0.7367 0.0077 0.7215 0.7518 8 Energy -0.1504 0.0448 -0.2393 -0.0616 0.4412 0.0204 0.4007 0.4817 2 Financials -0.4163 0.0091 -0.4342 -0.3984 0.4729 0.0064 0.4604 0.4854 4 Health Care -0.7305 0.0174 -0.7647 -0.6964 0.8050 0.0077 0.7900 0.8200 9 Industrials -0.5293 0.0062 -0.5415 -0.5172 0.5857 0.0041 0.5776 0.5938 5 Information Technology -0.5599 0.0135 -0.5864 -0.5334 0.6636 0.0092 0.6456 0.6816 7 Materials -0.3073 0.0117 -0.3304 -0.2843 0.3620 0.0089 0.3446 0.3795 1 Telecommunication Services -0.4065 0.0251 -0.4560 -0.3569 0.4524 0.0209 0.4112 0.4936 3 Table 90: Average valuation error and absolute valuation error in book value of owners’ equity, with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.5186 0.0041 -0.5268 -0.5105 0.586 0.0029 0.5803 0.5917 Table 91: Average valuation error and absolute valuation error in book value of owners’ equity, with standard error and a 95 percent confidence interval (C.I). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.4461 0.0117 Consumer Staples -0.5848 0.0065 Energy -0.1276 0.0422 Financials -0.3774 0.0079 Health Care -0.6416 0.0168 Industrials -0.4249 0.0063 Information Technology -0.5280 0.0126 Materials -0.2083 0.0109 Telecommunication Services -0.3933 0.0233 Table 92: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.4690 -0.4232 -0.5977 -0.5719 -0.2113 -0.0439 -0.3928 -0.3620 -0.6746 -0.6086 -0.4373 -0.4126 -0.5526 -0.5033 -0.2297 -0.1869 -0.4393 -0.3473 error in RIV(TVC), Abs(V.E.) Mean Std. Error 0.5594 0.0072 0.5848 0.0065 0.4165 0.0181 0.4201 0.0057 0.7145 0.0085 0.4968 0.0041 0.6150 0.0090 0.2892 0.0074 0.4248 0.0204 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.5453 0.5735 6 0.5719 0.5977 7 0.3805 0.4524 2 0.4088 0.4313 3 0.6979 0.7312 9 0.4887 0.5050 5 0.5974 0.6326 8 0.2747 0.3036 1 0.3845 0.4651 4 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.4349 0.0040 -0.4428 -0.4270 0.5113 0.0028 0.5058 0.5168 Table 93: Average valuation error and absolute valuation error in RIV(TVC), with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.1135 0.0179 Consumer Staples -0.3525 0.0115 Energy 0.4692 0.0773 Financials -0.0624 0.0112 Health Care -0.1295 0.0272 Industrials -0.2642 0.0078 Information Technology -0.2751 0.0184 Materials 0.0942 0.0149 Telecommunication Services -0.0977 0.0321 Table 94: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.1487 -0.0784 -0.3752 -0.3298 0.3159 0.6225 -0.0843 -0.0405 -0.1830 -0.0760 -0.2795 -0.2489 -0.3111 -0.2390 0.0648 0.1235 -0.1610 -0.0345 error in RIV(PMB), Abs(V.E.) Mean Std. Error 0.5346 0.0109 0.3550 0.0113 0.6234 0.0665 0.2815 0.0078 0.4297 0.0196 0.4160 0.0051 0.5355 0.0132 0.3132 0.0090 0.3881 0.0183 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.5133 0.5560 7 0.3328 0.3772 3 0.4916 0.7552 9 0.2662 0.2969 1 0.3912 0.4682 6 0.4060 0.4260 5 0.5097 0.5614 8 0.2956 0.3308 2 0.3520 0.4241 4 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.1700 0.0057 -0.1813 -0.1588 0.427 0.0039 0.4194 0.4345 Table 95: Average valuation error and absolute valuation error in RIV(PMB), with standard error and a 95 percent confidence interval (C.I.). 81 Rank V.E. 95 % C.I. Abs(V.E.) 95 % C.I. GICS Sector Mean Std. Error Lower Upper Mean Std. Error Lower Upper Abs(V.E.) Consumer Discretionary 0.7101 0.0343 0.6429 0.7773 0.9714 0.0291 0.9144 1.0285 8 Consumer Staples 0.2757 0.0266 0.2234 0.3279 0.4591 0.0171 0.4255 0.4926 3 Energy 0.2777 0.0659 0.1471 0.4084 0.5124 0.0512 0.4109 0.6140 6 Financials 0.2003 0.0143 0.1723 0.2283 0.3749 0.0109 0.3535 0.3963 2 Health Care 0.2562 0.0364 0.1846 0.3278 0.4932 0.0308 0.4327 0.5537 4 Industrials 0.2715 0.0133 0.2454 0.2976 0.4981 0.0108 0.4769 0.5194 5 Information Technology 0.7931 0.0436 0.7075 0.8786 1.0061 0.0401 0.9275 1.0846 9 Materials 0.1105 0.0152 0.0807 0.1402 0.3206 0.0092 0.3025 0.3387 1 Telecommunication Services 0.4527 0.0496 0.3549 0.5504 0.7279 0.0293 0.6701 0.7856 7 Table 96: Average valuation error and absolute valuation error in RIV(Q), with standard error and a 95 percent confidence interval (C.I.) per sector and ranked in ascending order. V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.4018 0.0107 0.3809 0.4227 0.6236 0.0093 0.6053 0.6418 Table 97: Average valuation error and absolute valuation error in RIV(Q), with standard error and a 95 percent confidence interval (C.I.). V.E. GICS Sector Mean Std. Error Consumer Discretionary -0.0873 0.0154 Consumer Staples 0.1366 0.0187 Energy 0.0998 0.0889 Financials -0.1949 0.0082 Health Care -0.4052 0.0156 Industrials -0.1262 0.0087 Information Technology -0.5204 0.0099 Materials 0.1893 0.0275 Telecommunication Services -0.4583 0.0204 Table 98: Average valuation error and absolute valuation interval (C.I.) per sector and ranked in ascending order. 95 % C.I. Lower Upper -0.1176 -0.0571 0.0999 0.1733 -0.0764 0.2759 -0.2111 -0.1788 -0.4358 -0.3746 -0.1433 -0.1090 -0.5399 -0.5009 0.1352 0.2433 -0.4984 -0.4182 error in PVEE(rE), Abs(V.E.) Mean Std. Error 0.4248 0.0105 0.2743 0.0132 0.5992 0.0683 0.2722 0.0061 0.4770 0.0104 0.3486 0.0064 0.5644 0.0079 0.4353 0.0226 0.4659 0.0195 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.4043 0.4453 4 0.2483 0.3003 2 0.4638 0.7346 9 0.2602 0.2842 1 0.4566 0.4974 7 0.3361 0.3611 3 0.5490 0.5798 8 0.3909 0.4797 5 0.4275 0.5044 6 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.1766 0.0055 -0.1874 -0.1659 0.3994 0.0039 0.3917 0.407 Table 99: Average valuation error and absolute valuation error in PVEE(rE), with standard error and a 95 percent confidence interval (C.I.). V.E. 95 % C.I. GICS Sector Mean Std. Error Lower Upper Consumer Discretionary 0.7884 0.0291 0.7313 0.8454 Consumer Staples 0.6116 0.0210 0.5703 0.6528 Energy 1.2600 0.1609 0.9410 1.5790 Financials 0.6570 0.0171 0.6235 0.6906 Health Care 0.0313 0.0249 -0.0177 0.0803 Industrials 0.7506 0.0140 0.7232 0.7779 Information Technology 0.3964 0.0284 0.3407 0.4521 Materials 1.1402 0.0417 1.0582 1.2222 Telecommunication Services 0.2360 0.0489 0.1395 0.3324 Table 100: Average valuation error and absolute valuation error in PVEE(rf), interval (C.I.) per sector and ranked in ascending order. Abs(V.E.) Mean Std. Error 0.9235 0.0259 0.6225 0.0199 1.4204 0.1480 0.7347 0.0142 0.4127 0.0162 0.8263 0.0124 0.7018 0.0233 1.1860 0.0397 0.6274 0.0269 with standard error Rank 95 % C.I. Lower Upper Abs(V.E.) 0.8726 0.9744 7 0.5832 0.6617 2 1.1270 1.7139 9 0.7069 0.7625 5 0.3809 0.4445 1 0.8019 0.8506 6 0.6560 0.7476 4 1.1081 1.2638 8 0.5743 0.6805 3 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total 0.6675 0.0097 0.6485 0.6864 0.8086 0.0083 0.7922 0.8249 Table 101: Average valuation error and absolute valuation error in PVEE(rf), with standard error and a 95 percent confidence interval (C.I.). 82 V.E. 95 % C.I. Abs(V.E.) GICS Sector Mean Std. Error Lower Upper Mean Std. Error Consumer Discretionary 0.1018 0.0159 0.0706 0.1330 0.4080 0.0117 Consumer Staples 0.3163 0.0229 0.2712 0.3613 0.3772 0.0199 Energy 0.1314 0.0696 -0.0065 0.2692 0.5489 0.0470 Financials -0.1654 0.0081 -0.1813 -0.1495 0.2550 0.0058 Health Care -0.1560 0.0160 -0.1875 -0.1245 0.3235 0.0093 Industrials 0.0471 0.0098 0.0279 0.0663 0.3228 0.0078 Information Technology -0.3007 0.0144 -0.3291 -0.2724 0.4589 0.0107 Materials 0.2024 0.0219 0.1594 0.2454 0.3419 0.0189 Telecommunication Services -0.2801 0.0191 -0.3178 -0.2423 0.3169 0.0161 Table 102: Average valuation error and absolute valuation error in AEG(TVC), with standard error interval (C.I.) per sector and ranked in ascending order. Rank 95 % C.I. Lower Upper Abs(V.E.) 0.3850 0.4309 7 0.3381 0.4163 6 0.4557 0.6420 9 0.2436 0.2664 1 0.3052 0.3418 4 0.3075 0.3382 3 0.4379 0.4800 8 0.3048 0.3791 5 0.2852 0.3486 2 and a 95 percent confidence V.E. 95 % C.I. Abs(V.E.) 95 % C.I. Mean Std. Error Lower Upper Mean Std. Error Lower Upper Total -0.0229 0.0057 -0.0341 -0.0117 0.3537 0.0042 0.3454 0.362 Table 103: Average valuation error and absolute valuation error in AEG(TVC), with standard error and a 95 percent confidence interval (C.I.). 83 8.14. Appendix 14: Statistical Testing 1998-2002 Number of H0: RIV(TVC)-BV = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0118* -1.4588 0.0728 0.1455 0.9272 354 Consumer Staples -0.1743*** -26.3603 0.0000 0.0000 1.0000 93 Energy 0.0879*** 2.9781 0.9963 0.0074 0.0037 21 Financials -0.0624*** -15.3718 0.0000 0.0000 1.0000 387 Health Care -0.1030*** -11.3111 0.0000 0.0000 1.0000 100 Industrials -0.0849*** -17.9565 0.0000 0.0000 1.0000 953 Information Technology -0.0262*** -4.6006 0.0000 0.0000 1.0000 318 Materials -0.0679*** -8.5542 0.0000 0.0000 1.0000 205 Telecommunication Services -0.0118* -1.5106 0.0679 0.1359 0.9321 64 Table 104: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(TVC)-BV = 0 Observations Mean t p (<0) p (≠0) p(>0) Total -0.0629*** -24.0723 0.0000 0.0000 1.0000 2495 Table 105: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.1667*** 6.3100 1.0000 0.0000 0.0000 354 Consumer Staples -0.2844*** -34.9853 0.0000 0.0000 1.0000 93 Energy 1.2391*** 19.3690 1.0000 0.0000 0.0000 21 Financials -0.1635*** -10.4949 0.0000 0.0000 1.0000 387 Health Care -0.0570 -0.8232 0.2062 0.4124 0.7938 100 Industrials -0.0410*** -5.8426 0.0000 0.0000 1.0000 953 Information Technology 0.0097 0.4281 0.6656 0.6689 0.3344 318 Materials 0.0972*** 5.0412 1.0000 0.0000 0.0000 205 Telecommunication Services -0.1074*** -4.0282 0.0001 0.0002 0.9999 64 Table 106: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations t p (<0) p (≠0) p(>0) Total -1.7759 0.0379 0.0759 0.9621 2495 Table 107: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean -0.0134** Number of H0: RIV(Q )-RIV(PMB) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.8040*** 13.8909 1.0000 0.0000 0.0000 354 Consumer Staples 0.2245*** 4.5192 1.0000 0.0000 0.0000 93 Energy -0.3975*** -19.3690 0.0000 0.0000 1.0000 21 Financials 0.0538*** 3.8458 0.9999 0.0001 0.0001 387 Health Care 0.4561*** 10.4741 1.0000 0.0000 0.0000 100 Industrials 0.2643*** 12.5275 1.0000 0.0000 0.0000 953 Information Technology 0.5092*** 5.6726 1.0000 0.0000 0.0000 318 Materials 0.0134*** 14.2218 1.0000 0.0000 0.0000 205 Telecommunication Services -0.0345 -0.6666 0.2537 0.5075 0.7463 64 Table 108: Paired t-test of DiffRIV(Q)-RIV(PMB). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(Q )-RIV(PMB) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.3118*** 17.9369 1.0000 0.0000 0.0000 2495 Table 109: Paired t-test of DiffRIV(Q)-RIV(PMB). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. 84 Number of H0: PVEE(rf)-PVEE(rE) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.4285*** 10.2376 1.0000 0.0000 0.0000 354 Consumer Staples 0.2031*** 12.4607 1.0000 0.0000 0.0000 93 Energy 1.4589*** 5.0410 1.0000 0.0001 0.0000 21 Financials 0.3428*** 17.0863 1.0000 0.0000 0.0000 387 Health Care 0.1259*** 3.2223 0.9991 0.0017 0.0009 100 Industrials 0.3637*** 24.5224 1.0000 0.0000 0.0000 953 Information Technology 0.1912*** 2.8896 0.9979 0.0041 0.0021 318 Materials 0.4671*** 16.8000 1.0000 0.0000 0.0000 205 Telecommunication Services -0.2196*** -16.2623 0.0000 0.0000 1.0000 64 Table 110: Paired t-test of DiffPVEE(rf)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: PVEE(rf)-PVEE(rE) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.3349*** 25.5190 1.0000 0.0000 0.0000 2495 Table 111: Paired t-test of DiffPVEE(rf)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.0459*** 3.1609 0.9991 0.0017 0.0009 354 Consumer Staples 0.2388*** 7.6771 1.0000 0.0000 0.0000 93 Energy -0.2821 -0.7102 0.2429 0.4858 0.7571 21 Financials -0.0241*** -3.0587 0.0012 0.0024 0.9988 387 Health Care -0.1297*** -4.3879 0.0000 0.0000 1.0000 100 Industrials 0.1153*** 10.6101 1.0000 0.0000 0.0000 953 Information Technology -0.0062 -0.2026 0.4198 0.8396 0.5802 318 Materials 0.0052 0.2091 0.5827 0.8346 0.4173 205 Telecommunication Services -0.2134*** -8.9115 0.0000 0.0000 1.0000 64 Table 112: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations t p (<0) p (≠0) p(>0) Total 5.4876 1.0000 0.0000 0.0000 2495 Table 113: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean 0.0423*** Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.1022*** 2.6139 0.9953 0.0093 0.0047 354 Consumer Staples -0.0075 -0.1331 0.4472 0.8944 0.5528 93 Energy 0.7655*** 4.8934 1.0000 0.0001 0.0000 21 Financials -0.2510*** -20.4998 0.0000 0.0000 1.0000 387 Health Care -0.2948*** -5.6034 0.0000 0.0000 1.0000 100 Industrials 0.0887*** 3.7825 0.9999 0.0002 0.0001 953 Information Technology -0.0748*** -3.0502 0.0012 0.0025 0.9988 318 Materials 0.4113*** 7.5619 1.0000 0.0000 0.0000 205 Telecommunication Services -0.1575*** -7.9474 0.0000 0.0000 1.0000 64 Table 114: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations t p (<0) p (≠0) p(>0) Total 1.8431 0.9673 0.0654 0.0327 2495 Table 115: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean 0.0240** 85 8.15. Appendix 15: Statistical Testing 2003-2007 Number of H0: RIV(TVC)-BV = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.1053*** -33.6117 0.0000 0.0000 1.0000 989 Consumer Staples -0.1485*** -41.4799 0.0000 0.0000 1.0000 233 Energy -0.0546*** -5.0747 0.0000 0.0000 1.0000 88 Financials -0.0648*** -23.8763 0.0000 0.0000 1.0000 803 Health Care -0.0934*** -40.4030 0.0000 0.0000 1.0000 371 Industrials -0.1049*** -83.0224 0.0000 0.0000 1.0000 1994 Information Technology -0.0693*** -28.6097 0.0000 0.0000 1.0000 971 Materials -0.0839*** -17.5938 0.0000 0.0000 1.0000 420 Telecommunication Services -0.0494*** -12.5867 0.0000 0.0000 1.0000 140 Table 116: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(TVC)-BV = 0 Observations Mean t p (<0) p (≠0) p(>0) Total -0.0913*** -92.0224 0.0000 0.0000 1.0000 6009 Table 117: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0815*** -8.5473 0.0000 0.0000 1.0000 989 Consumer Staples -0.2097*** -31.3732 0.0000 0.0000 1.0000 233 Energy -0.0059 -0.1321 0.4476 0.8952 0.5524 88 Financials -0.1117*** -11.8051 0.0000 0.0000 1.0000 803 Health Care -0.3439*** -30.2345 0.0000 0.0000 1.0000 371 Industrials -0.0971*** -34.9252 0.0000 0.0000 1.0000 1994 Information Technology -0.1001*** -10.7677 0.0000 0.0000 1.0000 971 Materials 0.0073 0.5465 0.7075 0.5850 0.2925 420 Telecommunication Services 0.0228 0.9492 0.8279 0.3442 0.1721 140 Table 118: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations t p (<0) p (≠0) p(>0) Total -32.8537 0.0000 0.0000 1.0000 6009 Table 119: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean -0.1052*** Number of H0: RIV(Q )-RIV(PMB) = 0 Observations GICS Sector Mean p (<0) p (≠0) p(>0) Consumer Discretionary 0.3363*** 13.9354 1.0000 0.0000 0.0000 989 Consumer Staples 0.0722*** 2.3649 0.9906 0.0189 0.0094 233 Energy -0.0589*** -3.8313 0.0001 0.0002 0.9999 88 Financials 0.1392*** 18.0246 1.0000 0.0000 0.0000 803 Health Care -0.0278* -1.6352 0.0514 0.1029 0.9486 371 Industrials 0.0252*** 2.3626 0.9909 0.0182 0.0091 1994 Information Technology 0.5396*** 15.3249 1.0000 0.0000 0.0000 971 Materials 0.0054*** 6.9477 1.0000 0.0000 0.0000 420 Telecommunication Services 0.5408*** 17.6213 1.0000 0.0000 0.0000 140 Table 120: Paired t-test of DiffRIV(Q)-RIV(PMB). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(Q )-RIV(PMB) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.1827*** 21.5655 1.0000 0.0000 0.0000 6009 Table 121: Paired t-test of DiffRIV(Q)-RIV(PMB). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. 86 Number of H0: PVEE(rf)-PVEE(rE) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.5033*** 24.1288 1.0000 0.0000 0.0000 989 Consumer Staples 0.3742*** 21.9433 1.0000 0.0000 0.0000 233 Energy 0.5818*** 6.5427 1.0000 0.0000 0.0000 88 Financials 0.5410*** 25.3087 1.0000 0.0000 0.0000 803 Health Care -0.0860*** -4.3314 0.0000 0.0000 1.0000 371 Industrials 0.5547*** 41.4940 1.0000 0.0000 0.0000 1994 Information Technology 0.1738*** 7.6697 1.0000 0.0000 0.0000 971 Materials 0.8183*** 26.8837 1.0000 0.0000 0.0000 420 Telecommunication Services 0.4040*** 7.9734 1.0000 0.0000 0.0000 140 Table 122: Paired t-test of DiffPVEE(rf)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: PVEE(rf)-PVEE(rE) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.4516*** 53.9609 1.0000 0.0000 0.0000 6009 Table 123: Paired t-test of DiffPVEE(rf)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.0082 0.9134 0.8194 0.3613 0.1806 989 Consumer Staples 0.0926*** 8.3359 1.0000 0.0000 0.0000 233 Energy -0.0416 -0.9590 0.1701 0.3402 0.8299 88 Financials 0.0004 0.0780 0.5311 0.9379 0.4689 803 Health Care -0.1451*** -11.7870 0.0000 0.0000 1.0000 371 Industrials -0.0417*** -8.7734 0.0000 0.0000 1.0000 1994 Information Technology -0.1218*** -15.2599 0.0000 0.0000 1.0000 971 Materials -0.1216*** -5.7525 0.0000 0.0000 1.0000 420 Telecommunication Services -0.1061*** -5.5433 0.0000 0.0000 1.0000 140 Table 124: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations t p (<0) p (≠0) p(>0) Total -14.8844 0.0000 0.0000 1.0000 6009 Table 125: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean -0.0491*** Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.1674*** -10.0932 0.0000 0.0000 1.0000 989 Consumer Staples -0.2060*** -8.7016 0.0000 0.0000 1.0000 233 Energy 0.0249 0.6393 0.7378 0.5243 0.2622 88 Financials -0.1162*** -11.6987 0.0000 0.0000 1.0000 803 Health Care -0.4255*** -36.0078 0.0000 0.0000 1.0000 371 Industrials -0.2565*** -35.1587 0.0000 0.0000 1.0000 1994 Information Technology -0.2076*** -25.5550 0.0000 0.0000 1.0000 971 Materials -0.0230* -1.2920 0.0985 0.1971 0.9015 420 Telecommunication Services -0.1254*** -5.2318 0.0000 0.0000 1.0000 140 Table 126: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations t p (<0) p (≠0) p(>0) Total -42.9440 0.0000 0.0000 1.0000 6009 Table 127: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean -0.2002*** 87 8.16. Appendix 16: Statistical Testing Five or More Consensus Estimates (1998-2007) Number of H0: RIV(TVC)-BV = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0655*** -10.6284 0.0000 0.0000 1.0000 436 Consumer Staples -0.1814*** -53.2327 0.0000 0.0000 1.0000 92 Energy -0.0911 . . . . 1 Financials -0.0920*** -35.7616 0.0000 0.0000 1.0000 432 Health Care -0.1111*** -17.7197 0.0000 0.0000 1.0000 103 Industrials -0.1042*** -48.0825 0.0000 0.0000 1.0000 986 Information Technology -0.0587*** -15.5313 0.0000 0.0000 1.0000 205 Materials -0.0821*** -14.8398 0.0000 0.0000 1.0000 319 Telecommunication Services -0.0419*** -11.2411 0.0000 0.0000 1.0000 131 Table 128: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(TVC)-BV = 0 Observations Mean t p (<0) p (≠0) p(>0) Total -0.0898*** -55.3749 0.0000 0.0000 1.0000 2705 Table 129: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.0347** 1.8294 0.9660 0.0680 0.0340 436 Consumer Staples -0.1730*** -18.6286 0.0000 0.0000 1.0000 92 Energy -0.1652 . . . . 1 Financials -0.2029*** -23.9396 0.0000 0.0000 1.0000 432 Health Care -0.3657*** -18.9748 0.0000 0.0000 1.0000 103 Industrials -0.0783*** -16.0006 0.0000 0.0000 1.0000 986 Information Technology -0.0876*** -5.2725 0.0000 0.0000 1.0000 205 Materials -0.0183* -1.2972 0.0977 0.1955 0.9023 319 Telecommunication Services -0.0285 -1.2845 0.1006 0.2013 0.8994 131 Table 130: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations t p (<0) p (≠0) p(>0) Total -17.5771 0.0000 0.0000 1.0000 2705 Table 131: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean -0.0854*** Number of H0: RIV(Q )-RIV(PMB) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.4445*** 9.9525 1.0000 0.0000 0.0000 436 Consumer Staples -0.1281*** -3.4446 0.0004 0.0009 0.9996 92 Energy -0.1080 . . . . 1 Financials 0.0993*** 10.1124 1.0000 0.0000 0.0000 432 Health Care -0.0109 -0.3579 0.3606 0.7211 0.6394 103 Industrials 0.0846*** 5.0515 1.0000 0.0000 0.0000 986 Information Technology 0.1219** 1.7741 0.9612 0.0775 0.0388 205 Materials 0.0052*** 6.0103 1.0000 0.0000 0.0000 319 Telecommunication Services 0.4053*** 10.5109 1.0000 0.0000 0.0000 131 Table 132: Paired t-test of DiffRIV(Q)-RIV(PMB). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(Q )-RIV(PMB) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.1430*** 12.3474 1.0000 0.0000 0.0000 2705 Table 133: Paired t-test of DiffRIV(Q)-RIV(PMB). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. 88 Number of H0: PVEE(rf)-PVEE(rE) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.3973*** 12.0542 1.0000 0.0000 0.0000 436 Consumer Staples 0.3685*** 15.8863 1.0000 0.0000 0.0000 92 Energy 1.4954 . . . . 1 Financials 0.6631*** 27.5438 1.0000 0.0000 0.0000 432 Health Care 0.0372 1.0209 0.8451 0.3097 0.1549 103 Industrials 0.5169*** 29.0727 1.0000 0.0000 0.0000 986 Information Technology -0.0207 -0.5749 0.2830 0.5660 0.7170 205 Materials 0.6989*** 20.1642 1.0000 0.0000 0.0000 319 Telecommunication Services 0.3325*** 6.4349 1.0000 0.0000 0.0000 131 Table 134: Paired t-test of DiffPVEE(rf)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: PVEE(rf)-PVEE(rE) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.4698*** 40.7689 1.0000 0.0000 0.0000 2705 Table 135: Paired t-test of DiffPVEE(rf)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0003 -0.0244 0.4903 0.9806 0.5097 436 Consumer Staples 0.1731*** 7.9423 1.0000 0.0000 0.0000 92 Energy -0.1955 . . . . 1 Financials 0.0030 0.6336 0.7367 0.5266 0.2633 432 Health Care -0.1088*** -6.8941 0.0000 0.0000 1.0000 103 Industrials -0.0091* -1.4954 0.0676 0.1351 0.9324 986 Information Technology -0.1240*** -10.3940 0.0000 0.0000 1.0000 205 Materials -0.1752*** -7.6363 0.0000 0.0000 1.0000 319 Telecommunication Services -0.0882*** -5.3698 0.0000 0.0000 1.0000 131 Table 136: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations t p (<0) p (≠0) p(>0) Total -7.8592 0.0000 0.0000 1.0000 2705 Table 137: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level Mean -0.0355*** Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0883*** -3.0447 0.0012 0.0025 0.9988 436 Consumer Staples -0.1725*** -3.7207 0.0002 0.0003 0.9998 92 Energy -0.1363 . . . . 1 Financials -0.1886*** -18.3399 0.0000 0.0000 1.0000 432 Health Care -0.3646*** -11.3731 0.0000 0.0000 1.0000 103 Industrials -0.1730*** -14.6954 0.0000 0.0000 1.0000 986 Information Technology -0.2327*** -17.2042 0.0000 0.0000 1.0000 205 Materials 0.0403* 1.2878 0.9006 0.1987 0.0994 319 Telecommunication Services -0.0916*** -5.6474 0.0000 0.0000 1.0000 131 Table 138: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations t p (<0) p (≠0) p(>0) Total -17.9375 0.0000 0.0000 1.0000 2705 Table 139: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean -0.1445*** 89 8.17. Appendix 17: Statistical Testing 5% Equity Risk Premium (1998-2007) Number of H0: RIV(TVC)-BV = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0757*** -24.8458 0.0000 0.0000 1.0000 1343 Consumer Staples -0.1519*** -45.8245 0.0000 0.0000 1.0000 326 Energy -0.0247** -2.1956 0.0151 0.0303 0.9849 109 Financials -0.0528*** -22.4303 0.0000 0.0000 1.0000 1186 Health Care -0.0905*** -35.2186 0.0000 0.0000 1.0000 471 Industrials -0.0889*** -53.5515 0.0000 0.0000 1.0000 2947 Information Technology -0.0486*** -20.2802 0.0000 0.0000 1.0000 1288 Materials -0.0729*** -18.8871 0.0000 0.0000 1.0000 625 Telecommunication Services -0.0276*** -6.7700 0.0000 0.0000 1.0000 204 Table 140: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(TVC)-BV = 0 Observations Mean t p (<0) p (≠0) p(>0) Total -0.0747*** -74.0984 0.0000 0.0000 1.0000 8499 Table 141: Paired t-test of DiffRIV(TVC)-Bv. *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0247*** -2.4500 0.0072 0.0144 0.9928 1343 Consumer Staples -0.2298*** -40.9211 0.0000 0.0000 1.0000 326 Energy 0.2069*** 3.4011 0.9995 0.0009 0.0005 109 Financials -0.1385*** -17.4318 0.0000 0.0000 1.0000 1186 Health Care -0.2848*** -16.1445 0.0000 0.0000 1.0000 471 Industrials -0.0808*** -27.7473 0.0000 0.0000 1.0000 2947 Information Technology -0.0794*** -9.2601 0.0000 0.0000 1.0000 1288 Materials 0.0240** 2.1915 0.9856 0.0288 0.0144 625 Telecommunication Services -0.0367** -2.0222 0.0222 0.0445 0.9778 204 Table 142: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(PMB)-RIV(TVC) = 0 Observations t p (<0) p (≠0) p(>0) Total -27.1871 0.0000 0.0000 1.0000 8499 Table 143: Paired t-test of DiffRIV(PMB)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean -0.0844*** Number of H0: RIV(Q )-RIV(PMB) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.4368*** 18.3707 1.0000 0.0000 0.0000 1343 Consumer Staples 0.1041*** 4.0339 1.0000 0.0001 0.0000 326 Energy -0.1110*** -5.9817 0.0000 0.0000 1.0000 109 Financials 0.0934*** 13.4170 1.0000 0.0000 0.0000 1186 Health Care 0.0634*** 3.4400 0.9997 0.0006 0.0003 471 Industrials 0.0821*** 8.2434 1.0000 0.0000 0.0000 2947 Information Technology 0.4705*** 14.1109 1.0000 0.0000 0.0000 1288 Materials 0.0075*** 11.9719 1.0000 0.0000 0.0000 625 Telecommunication Services 0.3398*** 10.6145 1.0000 0.0000 0.0000 204 Table 144: Paired t-test of DiffRIV(Q)-RIV(PMB). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: RIV(Q )-RIV(PMB) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.1966*** 25.6090 1.0000 0.0000 0.0000 8499 Table 145: Paired t-test of DiffRIV(Q)-RIV(PMB). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. 90 Number of H0: PVEE(rf)-PVEE(rE) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary 0.4987*** 23.2431 1.0000 0.0000 0.0000 1343 Consumer Staples 0.3482*** 21.9490 1.0000 0.0000 0.0000 326 Energy 0.8212*** 7.6262 1.0000 0.0000 0.0000 109 Financials 0.4625*** 25.9744 1.0000 0.0000 0.0000 1186 Health Care -0.0643*** -3.2311 0.0007 0.0013 0.9993 471 Industrials 0.4777*** 42.0115 1.0000 0.0000 0.0000 2947 Information Technology 0.1374*** 5.5630 1.0000 0.0000 0.0000 1288 Materials 0.7507*** 28.1609 1.0000 0.0000 0.0000 625 Telecommunication Services 0.1615*** 3.9437 0.9999 0.0001 0.0001 204 Table 146: Paired t-test of DiffPVEE(rf)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: PVEE(rf)-PVEE(rE) = 0 Observations Mean t p (<0) p (≠0) p(>0) Total 0.4092*** 52.7881 1.0000 0.0000 0.0000 8499 Table 147: Paired t-test of DiffPVEE(rf)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.0169*** -2.5673 0.0052 0.0104 0.9948 1343 Consumer Staples 0.1030*** 8.2610 1.0000 0.0000 0.0000 326 Energy -0.0503 -0.6684 0.2527 0.5053 0.7473 109 Financials -0.0172*** -4.6781 0.0000 0.0000 1.0000 1186 Health Care -0.1535*** -15.1898 0.0000 0.0000 1.0000 471 Industrials -0.0258*** -5.7477 0.0000 0.0000 1.0000 2947 Information Technology -0.1054*** -13.3586 0.0000 0.0000 1.0000 1288 Materials -0.0933*** -6.4581 0.0000 0.0000 1.0000 625 Telecommunication Services -0.1491*** -11.3010 0.0000 0.0000 1.0000 204 Table 148: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-PVEE(rE) = 0 Observations t p (<0) p (≠0) p(>0) Total -15.9211 0.0000 0.0000 1.0000 8499 Table 149: Paired t-test of DiffAEG(TVC)-PVEE(rE). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean -0.0456*** Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations GICS Sector Mean t p (<0) p (≠0) p(>0) Consumer Discretionary -0.1514*** -11.0280 0.0000 0.0000 1.0000 1343 Consumer Staples -0.2076*** -9.1720 0.0000 0.0000 1.0000 326 Energy 0.1324*** 3.0894 0.9987 0.0026 0.0013 109 Financials -0.1651*** -21.7453 0.0000 0.0000 1.0000 1186 Health Care -0.3910*** -30.3629 0.0000 0.0000 1.0000 471 Industrials -0.1740*** -21.1329 0.0000 0.0000 1.0000 2947 Information Technology -0.1561*** -22.7121 0.0000 0.0000 1.0000 1288 Materials 0.0528*** 2.5071 0.9938 0.0124 0.0062 625 Telecommunication Services -0.1079*** -6.8739 0.0000 0.0000 1.0000 204 Table 150: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Number of H0: AEG(TVC)-RIV(TVC) = 0 Observations t p (<0) p (≠0) p(>0) Total -35.1956 0.0000 0.0000 1.0000 8499 Table 151: Paired t-test of DiffAEG(TVC)-RIV(TVC). *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. Mean -0.1576*** 91 8.18. Appendix 18: Summary of Empirical Results and Statistical Testing: 1998-2002 4.00 3.20 2.40 V.E. 1.60 0.80 0.00 RIV(PMB) RIV(Q) PVEE(rf) AEG(TVC) Chart 33: Average valuation error for each GICS industry sector and model over the period 1998-2002. 92 Materials Industrials Health Care PVEE(rE) Telecommunication Services RIV(TVC) Information Technology BV Financials Energy Consumer Staples -1.60 Consumer Discretionary -0.80 4.00 3.20 V.E. 2.40 1.60 RIV(PMB) RIV(Q) PVEE(rf) AEG(TVC) Chart 34: Average absolute valuation error for each GICS industry sector and model over the period 1998-2002. 93 Materials Industrials Health Care PVEE(rE) Telecommunication Services RIV(TVC) Information Technology BV Financials Energy Consumer Staples 0.00 Consumer Discretionary 0.80 0.80 0.60 0.40 V.E. 0.20 0.00 -0.20 -0.40 -0.60 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) PVEE(rf) AEG(TVC) Chart 35: Average valuation error for each model over the period (1998-2002). 0.90 0.80 0.70 0.60 V.E. 0.50 0.40 0.30 0.20 0.10 0.00 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) Chart 36: Average absolute valuation error for each model over the period (1998-2002). 94 The empirical modelling in this section implies that: Average Valuation error Valuation Model Book Value Over/underestimation Underestimates for 8/9 sectors. RIV(TVC) Average Absolute Valuation error Largest Error Consumer Staples (-), Telecommunication Services (-) Smallest Error Materials (-), Health Care (-) Largest Error Information Technology, Health Care Smallest Error Materials, Financials Underestimates for 8/9 sectors. Telecommunication Services (-), Energy (+) Industrials (-), Consumer Discretionary (-) Information Technology, Telecommunication Services Materials, Financials RIV(PMB) Underestimates for 5/9 sectors. Energy (+), Telecommunication Services (-) Financials (-), Consumer Discretionary (+) Energy, Information Technology Consumer Staples, Financials RIV(Q) Overestimates 8/9 sectors. for Energy (+), Consumer Discretionary (+) Telecommunication Services (-), Financials (+) Consumer Discretionary, Energy Materials, Financials PVEE(rE) Overestimates 5/9 sectors. for Energy (+), Telecommunication Services (-) Financials (-), Consumer Discretionary (+) Energy, Telecommunication Services Financials, Consumer Staples PVEE(rf) Overestimates 8/9 sectors. for Energy (+), Material (+) Health Care (+), Information Technology (+) Energy, Materials Consumer Staples, Telecommunication Services AEG(TVC) Overestimates 6/9 sectors. for Energy (+), Material (+) Financials (-), Health Care (+) Energy, Consumer Discretionary Financials, Health Care Table 152: Overview of results from empirical modelling. Summarised results from the statistical testing of hypotheses: H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 GICS Sector Consumer Discretionary * (***) (***) (***) (***) (***) Consumer Staples *** *** (***) (***) (***) Energy (***) (***) *** (***) (***) Financials *** *** (***) (***) *** *** Health Care *** (***) (***) *** *** Industrials *** *** (***) (***) (***) (***) Information Technology *** (***) (***) *** Materials *** (***) (***) (***) (***) Telecommunication Services * *** *** *** *** Table 153: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 Total *** *** (***) (***) (***) (**) Table 154: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. 95 8.19. Appendix 19: Summary of Empirical Results and Statistical Testing: 2003-2007 1.60 1.20 0.80 V.E. 0.40 0.00 -0.40 RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 37: Average valuation error for each GICS industry sector and model over the period 2003-2007. 96 Materials Information Technology Telecommunication Services BV Industrials Health Care Financials Energy Consumer Staples -1.20 Consumer Discretionary -0.80 1.60 0.80 RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 38: Average absolute valuation error for each GICS industry sector and model over the period 2003-2007. 97 Materials Telecommunication Services RIV(TVC) Information Technology BV Industrials Health Care Financials Energy 0.00 Consumer Staples 0.40 Consumer Discretionary V.E. 1.20 0.80 0.60 0.40 V.E. 0.20 0.00 -0.20 -0.40 -0.60 -0.80 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 39: Average valuation error for each model over the period (2003-2007). 0.90 0.80 0.70 0.60 V.E. 0.50 0.40 0.30 0.20 0.10 0.00 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) Chart 40: Average absolute valuation error for each model over the period (2003-2007). 98 AEG(TVC) The empirical modelling in this section implies that: Average Valuation error Valuation Model Book Value Over/underestimation Underestimates for all sectors. RIV(TVC) Average Absolute Valuation error Largest Error Health Care (-), Consumer Staples (-) Smallest Error Telecommunication Services (-), Energy (-) Largest Error Health Care, Consumer Staples Smallest Error Telecommunication Services, Materials Underestimates for all sectors. Health Care (-), Consumer Staples (-) Materials (-), Telecommunication Services (-), Health Care, Consumer Staples Telecommunication Services, Materials RIV(PMB) Underestimates for 6/9 sectors. Consumer Staples (-), Industrials (-) Financials (-), Materials (+) Consumer Discretionary, Information Technology Financials, Materials RIV(Q) Overestimates alls sectors. for Information Technology (+), Telecommunication Services (+) Energy (+), Health Care (+) Information Technology, Telecommunication Services Energy, Materials PVEE(rE) Overestimates 7/9 sectors. for Information Technology (-), Health Care (-) Consumer Discretionary (-), Energy (-) Information Technology, Health Care Financials, Industrials PVEE(rf) Overestimates all sectors. for Materials (+), Energy (+) Health Care (+), Information Technology (+) Materials, Energy Health Care, Information Technology AEG(TVC) Underestimates for 5/9 sectors. Energy (-), Telecommunication Services (-) Energy, Consumer Staples Telecommunication Services, Industrials Consumer Staples (+), Consumer Discretionary (+) Table 155: Overview of results from empirical modelling. Summarised results from the statistical testing of hypotheses: H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 GICS Sector Consumer Discretionary *** *** (***) (***) *** Consumer Staples *** *** (***) (***) (***) *** Energy ** *** (***) Financials *** *** (***) (***) *** Health Care *** *** * *** *** *** Industrials *** *** (***) (***) *** *** Information Technology *** *** (***) (***) *** *** Materials *** (***) (***) *** * Telecommunication Services *** (***) (***) *** *** Table 156: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 Total *** *** (***) (***) *** *** Table 157: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. 99 8.20. Appendix 20: Summary of Empirical Results and Statistical Testing: 5 or More Consensus Estimates (1998-2007) 2.00 1.60 1.20 0.40 0.00 -0.40 RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 41: Average valuation error for each GICS industry sector and model over the whole period (1998-2007). 100 Materials Information Technology Telecommunication Services BV Industrials Health Care Financials Energy -1.20 Consumer Staples -0.80 Consumer Discretionary V.E. 0.80 2.00 1.80 1.60 1.40 1.00 0.80 0.60 0.40 RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 42: Average absolute valuation error for each GICS industry sector and model over the whole period (1998-2007). 101 Materials Information Technology Telecommunication Services BV Industrials Health Care Financials Energy 0.00 Consumer Staples 0.20 Consumer Discretionary V.E. 1.20 0.80 0.60 0.40 V.E. 0.20 0.00 -0.20 -0.40 -0.60 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 43: Average valuation error for each model over the whole period (1998-2007). 0.90 0.80 0.70 0.60 V.E. 0.50 0.40 0.30 0.20 0.10 0.00 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 44: Average absolute valuation error for each model over the whole period (1998-2007). 102 The empirical modelling in this section implies that: Average Valuation error Average Absolute Valuation error Valuation Model Book Value Over/underestimation Underestimates for all sectors. Largest Error Consumer Staples (-), Health Care (-) Smallest Error Materials (-), Energy (-) Largest Error Consumer Staples, Health Care Smallest Error Energy, Materials RIV(TVC) Underestimates for all sectors. Health Care (-), Consumer Staples (-) Energy (-), Materials (-) Health Care, Information Technology Energy, Materials RIV(PMB) Underestimates for 7/9 sectors. Consumer Staples (-), Information Technology (-) Telecommunication Services (-), Material (+) Consumer Discretionary, Information Technology Energy, Financials RIV(Q) Overestimates for 8/9 sectors. Consumer Discretionary (+), Telecommunication Services (+) Consumer Staples (+), Energy (-) Consumer Discretionary, Telecommunication Services Energy, Financials PVEE(rE) Underestimates for 6/9 sectors. Information Technology (-), Energy (+) Financials (-), Consumer Discretionary (-) Information Technology, Materials Financials, Industrials PVEE(rf) Overestimates for 7/9 sectors. Energy (+), Materials (+) Health Care (+), Information Technology (+) Energy, Materials Health Care, Information Technology AEG(TVC) Overestimates for 5/9 sectors. Financials (+), Health Care (-) Consumer Staples, Consumer Discretionary Energy, Financials Consumer Staples (+), Information Technology (-) Table 158: Overview of results from empirical modelling. Summarised results from the statistical testing of hypotheses: H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 GICS Sector Consumer Discretionary *** (**) (***) (***) *** Consumer Staples *** *** *** (***) (***) *** Energy Financials *** *** (***) (***) *** Health Care *** *** *** *** Industrials *** *** (***) (***) * *** Information Technology *** *** (**) *** *** Materials *** * (***) (***) *** (*) Telecommunication Services *** (***) (***) *** *** Table 159: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 Total *** *** (***) (***) *** *** Table 160: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. 103 8.21. Appendix 21: Summary of Empirical Results and Statistical Testing: 5% Equity Risk Premium (1998-2007) 1.60 1.20 0.80 V.E. 0.40 0.00 -0.40 RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 45: Average valuation error for each GICS industry sector and model over the whole period (1998-2007). 104 Materials Information Technology Telecommunication Services BV Industrials Health Care Financials Energy Consumer Staples -1.20 Consumer Discretionary -0.80 1.60 1.40 1.20 0.80 0.60 0.40 RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 46: Average absolute valuation error for each GICS industry sector and model over the whole period (1998-2007). 105 Materials Information Technology Telecommunication Services BV Industrials Health Care Financials Energy 0.00 Consumer Staples 0.20 Consumer Discretionary V.E. 1.00 0.80 0.60 0.40 V.E. 0.20 0.00 -0.20 -0.40 -0.60 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 47: Average valuation error for each model over the whole period (1998-2007). 0.90 0.80 0.70 0.60 V.E. 0.50 0.40 0.30 0.20 0.10 0.00 BV RIV(TVC) RIV(PMB) RIV(Q) PVEE(rE) PVEE(rf) AEG(TVC) Chart 48: Average absolute valuation error for each model over the whole period (1998-2007). 106 The empirical modelling in this section implies that: Average Valuation error Average Absolute Valuation error Valuation Model Book Value Over/underestimation Underestimates for all sectors. Largest Error Consumer Staples (-), Health Care (-) Smallest Error Energy (-), Materials (-) Largest Error Health Care, Consumer Staples Smallest Error Materials, Energy RIV(TVC) Underestimates for all sectors. Health Care (-), Consumer Staples (-) Energy (-), Materials (-) Health Care, Information Technology Materials, Energy RIV(PMB) Underestimates for 7/9 sectors. Energy (+), Consumer Staples (-) Materials (+), Telecommunication Services (-) Energy, Information Technology Financials, Materials RIV(Q) Overestimates for all sectors. Information Technology (+), Consumer Discretionary (+) Materials (+), Financials (+) Information Technology, Consumer Discretionary Materials, Financials PVEE(rE) Underestimates for 6/9 sectors. Information Technology (-), Telecommunication Services (-) Consumer Discretionary (-), Energy (+) Energy, Information Technology Health Care, Consumer Staples PVEE(rf) Overestimates for all sectors. Energy (+), Materials (+) Energy, Materials Health Care, Consumer Staples AEG(TVC) Overestimates for 5/9 sectors. Health Care (+), Telecommunication Services (+) Industrials (+), Consumer Discretionary (+) Energy, Information Technology Financials, Telecommunication Services Consumer Staples (+), Information Technology (-) Table 161: Overview of results from empirical modelling. Summarised results from the statistical testing of hypotheses: H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 GICS Sector Consumer Discretionary *** * (***) (***) *** *** Consumer Staples *** *** (***) (***) (***) *** Energy ** (***) *** (***) (***) Financials *** *** (***) (***) *** *** Health Care *** *** (***) *** *** *** Industrials *** *** (***) (***) *** *** Information Technology *** *** (***) (***) *** *** Materials *** (**) (***) (***) *** (***) Telecommunication Services *** ** (***) (***) *** *** Table 162: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. H0: RIV(TVC)- H0: RIV(PMB)- H0: RIV(Q )- H0: PVEE(rf)- H0: AEG(TVC)- H0: AEG(TVC)BV = 0 RIV(TVC) = 0 RIV(PMB) = 0 PVEE(rE) = 0 PVEE(rE) = 0 RIV(TVC) = 0 Total *** *** (***) (***) *** *** Table 163: Summary of performed t-tests of hypotheses 1-5 and sub-hypothesis. p (<0): *** Significant at the 1 percent level, ** Significant at the 5 percent level, * Significant at the 10 percent level. p (>0): (***) Significant at the 1 percent level, (**) Significant at the 5 percent level, (*) Significant at the 10 percent level. 107