Paper

zz

Explore Categories

Log in

Create new account

No category

Risk Aversion and Optimal Reserve Prices in First

Download

Report

Slides - Polimi

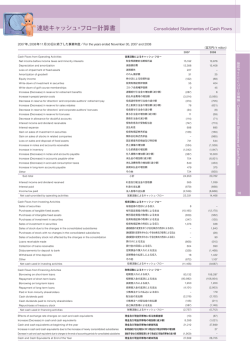

連結キャッシュ・フロー計算書

Regret Minimization for Reserve Prices in Second-Price

The Balance Sheets of Younger Americans: Is the American Dream

Price Inference in Small Markets - University of Wisconsin–Madison

Selling with Evidence - American Economic Association

On the Economic Meaning of Machina`s Fr echet

Slides - Polimi

Prices and the Winner`s Curse

Hashgraph Market Competitive Intelligence and Tracking Report Till 2026

Bidding and Searching for the Best Deal: Strategic Behavior in

© Copyright 2026 Paperzz

About Paperzz

DMCA / GDPR

Report